Yageo Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

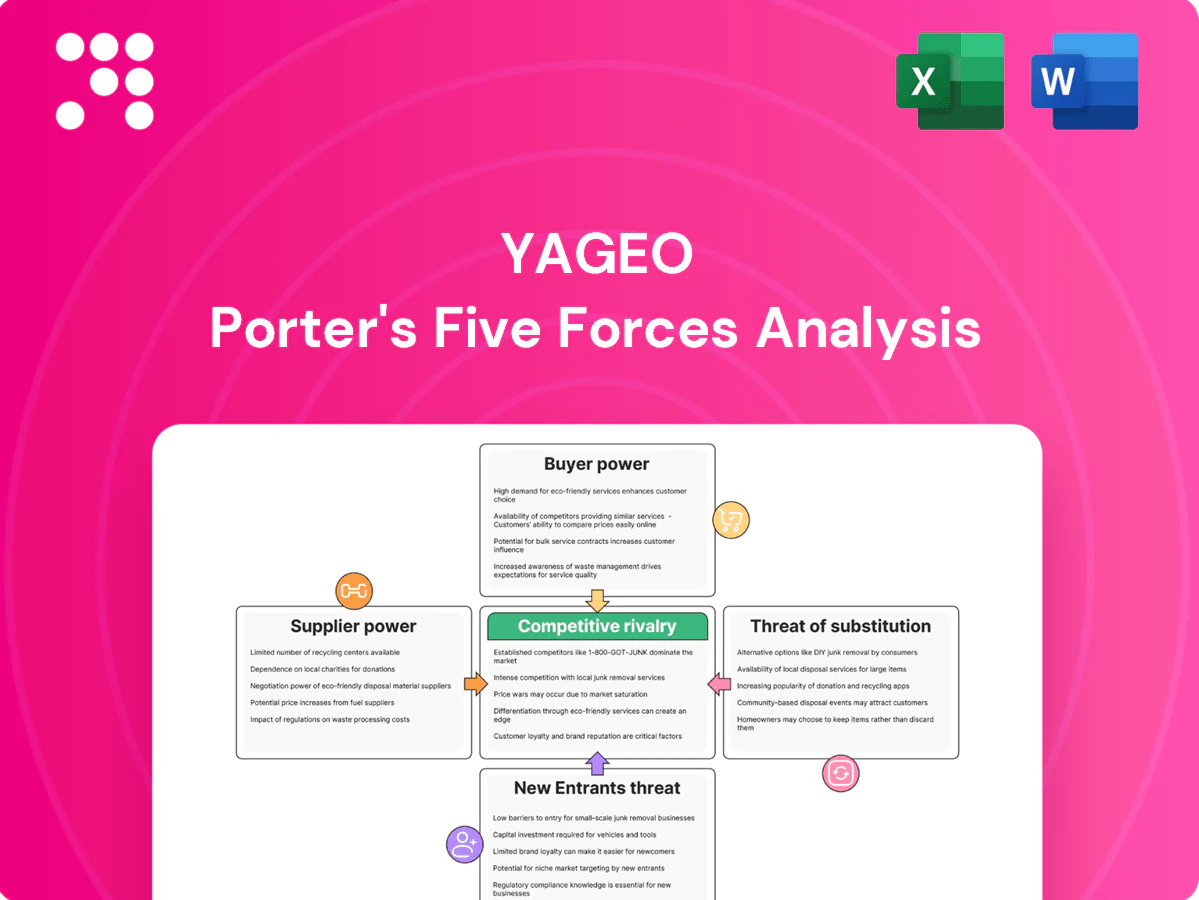

Yageo’s Porter's Five Forces snapshot highlights supplier leverage, buyer pressure, competitive rivalry, substitutes, and entry barriers shaping its market position. The complete report reveals force-by-force ratings, visuals, and strategic implications to guide investment or strategic moves. Ready for the full consultant-grade analysis? Unlock the complete Porter's Five Forces report for Yageo now.

Suppliers Bargaining Power

Critical raw materials concentration

Yageo relies on specialized inputs—nickel, copper, palladium and ceramic powders—for MLCCs, and supply is highly concentrated: Chile supplied about 27% of global mined copper in 2023, Indonesia roughly 40% of nickel, while Russia accounted for an estimated 30–40% of palladium output, amplifying concentration risk. Supplier consolidation or geopolitical disruptions can rapidly tighten availability and compress margins. Yageo reduces risk via multi-sourcing and inventory buffers, but supplier leverage remains significant.

Commodity price volatility

Metals and energy price swings (LME copper +12% in 2024) directly raised Yageo input costs and compressed gross margin volatility by roughly 300–600 basis points year-on-year; pass-through to customers is possible but typically lags, creating earnings volatility in downcycles. Hedging and long-term supply contracts (covering about 60% of expected needs in 2024) reduce but do not eliminate exposure. Prolonged commodity spikes can erode pricing competitiveness versus rivals with stronger hedging or vertical integration.

Specialty powder and equipment know-how

High-purity ceramic powders and specialized deposition equipment are technically complex and supplied by a narrow vendor base; qualification cycles for new suppliers typically run 6–12 months and lead times often extend 12–24 weeks, raising tangible switching costs. This supply tightness gives suppliers leverage on specifications, pricing and delivery cadence. Co-development programs (joint R&D and tooling investments) align incentives but deepen supplier lock-in and dependency.

Geopolitical and logistics risk

Global sourcing exposes Yageo to trade restrictions and chokepoints—export controls, port congestion and 2023–24 Red Sea/Strait of Hormuz tensions have repeatedly disrupted routes. Suppliers may favor larger, long‑term customers, reducing Yageo’s allocations; diversification of origin and partial nearshoring mitigate but do not eliminate risk.

- Trade restrictions

- Port congestion

- Supplier prioritization

- Diversification/nearshoring

ESG and compliance constraints

Responsible sourcing for conflict minerals and environmental compliance narrows viable supplier pools, forcing longer lead times and higher selection barriers. Audits and certifications add onboarding cost and time, increasing supplier bargaining leverage during remediation. Non-compliance risk elevates supplier leverage while buyers wait for corrective actions, and Yageo’s scale improves enforcement but cannot fully offset scarcity effects.

- Responsible sourcing narrows suppliers

- Audits raise onboarding cost/time

- Non-compliance increases supplier leverage

- Yageo scale helps but scarcity remains

Supplier power squeezes margins: Chile 27% Cu, Indonesia ~40% Ni, hedges 60%

Supplier power is high: raw-material concentration (Chile 27% copper 2023; Indonesia ~40% nickel; Russia 30–40% palladium) and narrow ceramic/equipment supply raise switching costs and lead times (qualification 6–12 months; lead times 12–24 weeks). Commodity swings (LME copper +12% in 2024) compress margins; hedges/long‑term contracts (~60% covered in 2024) mitigate but not eliminate risk.

| Metric | Value |

|---|---|

| Chile share (Cu 2023) | 27% |

| Indonesia share (Ni) | ~40% |

| Russia share (Pd) | 30–40% |

| LME copper 2024 | +12% |

| Hedge coverage 2024 | ~60% |

| Supplier lead times | 12–24 wks |

What is included in the product

Tailored Porter's Five Forces analysis for Yageo that uncovers key drivers of competition, supplier and buyer power, and market entry risks, identifying substitutes and disruptive threats to its component business. Includes strategic commentary on pricing influence, barriers protecting incumbents, and implications for Yageo's profitability and market positioning.

A clear, one-sheet summary of Yageo's Five Forces—visualize supplier/customer power, industry rivalry, and threats of substitutes/entrants to speed strategic decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Large OEMs and EMS leverage

Tier-1 OEMs and EMS aggregate massive volumes, creating strong price pressure on suppliers during annual sourcing cycles and scorecard-driven cost-downs.

Buyers routinely shift share among qualified vendors to extract concessions, using volume concentration and long-term program leverage.

Yageo mitigates this through broad product breadth, high reliability and integrated global logistics and consignment support, preserving margin and share.

Design-in and qualification stickiness

Once Yageo components are qualified, switching costs rise as revalidation commonly requires 6–12 months and carries added failure-risk and warranty exposure, tempering buyer power mid-cycle. Buyers typically reopen competition at new design cycles (commonly 2–5 years) to reset pricing. Automotive and industrial approvals such as AEC-Q extend part lifetimes and traceability requirements, prompting periodic rebids often every 3–7 years.

Dual-sourcing and approved vendor lists

Most buyers mandate multi-sourcing, so being one of two or three approved suppliers caps pricing upside and forces volume-based or tiered margins; approved-vendor lists commonly name 2–3 providers. Share allocations can shift quickly with lead-time or quality delta, and customers reallocate volumes based on delivery and PPAP/AEC pass rates. Maintaining top-tier on-time delivery and PPAP/AEC credentials is essential to defend share.

High price sensitivity in commoditized SKUs

Standard resistors and MLCCs are highly substitutable, pushing negotiations to penny-level discounts on components often priced in the $0.01–$0.10 range; buyers evaluate total cost of ownership including packaging, reel sizes and logistics, and in downturns excess inventory magnifies buyer leverage, forcing suppliers to offer tighter terms unless specialty specs or value-add services justify premiums.

- High substitutability → penny-level pricing pressure

- Buyers focus on TCO: packaging, reel sizes, logistics

- Premiums require specialty specs or services

- Downturn inventory increases buyer leverage

Demand cyclicality and inventory swings

Electronics cycles drive abrupt order cuts and pushouts that force price concessions, while automotive and industrial segments—which represented roughly 40% of passive components demand in 2024—offer steadier but still corrective inventory behavior.

Buyers increasingly demand vendor-managed inventory and consignment to shift holding costs to suppliers; Yageo must balance high fab utilization with disciplined pricing to avoid margin erosion amid these swings.

Passive components market $64.3B, auto/industrial 40%; suppliers face yearly sourcing cost pressure

Tier-1 OEMs and EMS concentrate volumes and force aggressive cost-downs during annual sourcing cycles. Buyers shift share among qualified vendors and reopen competition at 2–5 year design cycles, tempering supplier pricing. Yageo defends margins via breadth, reliability, VMI/consignment and AEC-Q qualifications. 2024 passive market ~64.3B with automotive/industrial ~40%.

| Metric | 2024 |

|---|---|

| Passive market | $64.3B |

| Auto/Industrial share | ~40% |

| Typical pricing | $0.01–$0.10 |

Preview Before You Purchase

Yageo Porter's Five Forces Analysis

This preview shows the exact Yageo Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed is the full, professionally formatted file, ready for download and immediate use. What you see here is exactly what will be available to you after payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Yageo’s Porter's Five Forces snapshot highlights supplier leverage, buyer pressure, competitive rivalry, substitutes, and entry barriers shaping its market position. The complete report reveals force-by-force ratings, visuals, and strategic implications to guide investment or strategic moves. Ready for the full consultant-grade analysis? Unlock the complete Porter's Five Forces report for Yageo now.

Suppliers Bargaining Power

Critical raw materials concentration

Yageo relies on specialized inputs—nickel, copper, palladium and ceramic powders—for MLCCs, and supply is highly concentrated: Chile supplied about 27% of global mined copper in 2023, Indonesia roughly 40% of nickel, while Russia accounted for an estimated 30–40% of palladium output, amplifying concentration risk. Supplier consolidation or geopolitical disruptions can rapidly tighten availability and compress margins. Yageo reduces risk via multi-sourcing and inventory buffers, but supplier leverage remains significant.

Commodity price volatility

Metals and energy price swings (LME copper +12% in 2024) directly raised Yageo input costs and compressed gross margin volatility by roughly 300–600 basis points year-on-year; pass-through to customers is possible but typically lags, creating earnings volatility in downcycles. Hedging and long-term supply contracts (covering about 60% of expected needs in 2024) reduce but do not eliminate exposure. Prolonged commodity spikes can erode pricing competitiveness versus rivals with stronger hedging or vertical integration.

Specialty powder and equipment know-how

High-purity ceramic powders and specialized deposition equipment are technically complex and supplied by a narrow vendor base; qualification cycles for new suppliers typically run 6–12 months and lead times often extend 12–24 weeks, raising tangible switching costs. This supply tightness gives suppliers leverage on specifications, pricing and delivery cadence. Co-development programs (joint R&D and tooling investments) align incentives but deepen supplier lock-in and dependency.

Geopolitical and logistics risk

Global sourcing exposes Yageo to trade restrictions and chokepoints—export controls, port congestion and 2023–24 Red Sea/Strait of Hormuz tensions have repeatedly disrupted routes. Suppliers may favor larger, long‑term customers, reducing Yageo’s allocations; diversification of origin and partial nearshoring mitigate but do not eliminate risk.

- Trade restrictions

- Port congestion

- Supplier prioritization

- Diversification/nearshoring

ESG and compliance constraints

Responsible sourcing for conflict minerals and environmental compliance narrows viable supplier pools, forcing longer lead times and higher selection barriers. Audits and certifications add onboarding cost and time, increasing supplier bargaining leverage during remediation. Non-compliance risk elevates supplier leverage while buyers wait for corrective actions, and Yageo’s scale improves enforcement but cannot fully offset scarcity effects.

- Responsible sourcing narrows suppliers

- Audits raise onboarding cost/time

- Non-compliance increases supplier leverage

- Yageo scale helps but scarcity remains

Supplier power squeezes margins: Chile 27% Cu, Indonesia ~40% Ni, hedges 60%

Supplier power is high: raw-material concentration (Chile 27% copper 2023; Indonesia ~40% nickel; Russia 30–40% palladium) and narrow ceramic/equipment supply raise switching costs and lead times (qualification 6–12 months; lead times 12–24 weeks). Commodity swings (LME copper +12% in 2024) compress margins; hedges/long‑term contracts (~60% covered in 2024) mitigate but not eliminate risk.

| Metric | Value |

|---|---|

| Chile share (Cu 2023) | 27% |

| Indonesia share (Ni) | ~40% |

| Russia share (Pd) | 30–40% |

| LME copper 2024 | +12% |

| Hedge coverage 2024 | ~60% |

| Supplier lead times | 12–24 wks |

What is included in the product

Tailored Porter's Five Forces analysis for Yageo that uncovers key drivers of competition, supplier and buyer power, and market entry risks, identifying substitutes and disruptive threats to its component business. Includes strategic commentary on pricing influence, barriers protecting incumbents, and implications for Yageo's profitability and market positioning.

A clear, one-sheet summary of Yageo's Five Forces—visualize supplier/customer power, industry rivalry, and threats of substitutes/entrants to speed strategic decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Large OEMs and EMS leverage

Tier-1 OEMs and EMS aggregate massive volumes, creating strong price pressure on suppliers during annual sourcing cycles and scorecard-driven cost-downs.

Buyers routinely shift share among qualified vendors to extract concessions, using volume concentration and long-term program leverage.

Yageo mitigates this through broad product breadth, high reliability and integrated global logistics and consignment support, preserving margin and share.

Design-in and qualification stickiness

Once Yageo components are qualified, switching costs rise as revalidation commonly requires 6–12 months and carries added failure-risk and warranty exposure, tempering buyer power mid-cycle. Buyers typically reopen competition at new design cycles (commonly 2–5 years) to reset pricing. Automotive and industrial approvals such as AEC-Q extend part lifetimes and traceability requirements, prompting periodic rebids often every 3–7 years.

Dual-sourcing and approved vendor lists

Most buyers mandate multi-sourcing, so being one of two or three approved suppliers caps pricing upside and forces volume-based or tiered margins; approved-vendor lists commonly name 2–3 providers. Share allocations can shift quickly with lead-time or quality delta, and customers reallocate volumes based on delivery and PPAP/AEC pass rates. Maintaining top-tier on-time delivery and PPAP/AEC credentials is essential to defend share.

High price sensitivity in commoditized SKUs

Standard resistors and MLCCs are highly substitutable, pushing negotiations to penny-level discounts on components often priced in the $0.01–$0.10 range; buyers evaluate total cost of ownership including packaging, reel sizes and logistics, and in downturns excess inventory magnifies buyer leverage, forcing suppliers to offer tighter terms unless specialty specs or value-add services justify premiums.

- High substitutability → penny-level pricing pressure

- Buyers focus on TCO: packaging, reel sizes, logistics

- Premiums require specialty specs or services

- Downturn inventory increases buyer leverage

Demand cyclicality and inventory swings

Electronics cycles drive abrupt order cuts and pushouts that force price concessions, while automotive and industrial segments—which represented roughly 40% of passive components demand in 2024—offer steadier but still corrective inventory behavior.

Buyers increasingly demand vendor-managed inventory and consignment to shift holding costs to suppliers; Yageo must balance high fab utilization with disciplined pricing to avoid margin erosion amid these swings.

Passive components market $64.3B, auto/industrial 40%; suppliers face yearly sourcing cost pressure

Tier-1 OEMs and EMS concentrate volumes and force aggressive cost-downs during annual sourcing cycles. Buyers shift share among qualified vendors and reopen competition at 2–5 year design cycles, tempering supplier pricing. Yageo defends margins via breadth, reliability, VMI/consignment and AEC-Q qualifications. 2024 passive market ~64.3B with automotive/industrial ~40%.

| Metric | 2024 |

|---|---|

| Passive market | $64.3B |

| Auto/Industrial share | ~40% |

| Typical pricing | $0.01–$0.10 |

Preview Before You Purchase

Yageo Porter's Five Forces Analysis

This preview shows the exact Yageo Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed is the full, professionally formatted file, ready for download and immediate use. What you see here is exactly what will be available to you after payment.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Yageo’s Porter's Five Forces snapshot highlights supplier leverage, buyer pressure, competitive rivalry, substitutes, and entry barriers shaping its market position. The complete report reveals force-by-force ratings, visuals, and strategic implications to guide investment or strategic moves. Ready for the full consultant-grade analysis? Unlock the complete Porter's Five Forces report for Yageo now.

Suppliers Bargaining Power

Critical raw materials concentration

Yageo relies on specialized inputs—nickel, copper, palladium and ceramic powders—for MLCCs, and supply is highly concentrated: Chile supplied about 27% of global mined copper in 2023, Indonesia roughly 40% of nickel, while Russia accounted for an estimated 30–40% of palladium output, amplifying concentration risk. Supplier consolidation or geopolitical disruptions can rapidly tighten availability and compress margins. Yageo reduces risk via multi-sourcing and inventory buffers, but supplier leverage remains significant.

Commodity price volatility

Metals and energy price swings (LME copper +12% in 2024) directly raised Yageo input costs and compressed gross margin volatility by roughly 300–600 basis points year-on-year; pass-through to customers is possible but typically lags, creating earnings volatility in downcycles. Hedging and long-term supply contracts (covering about 60% of expected needs in 2024) reduce but do not eliminate exposure. Prolonged commodity spikes can erode pricing competitiveness versus rivals with stronger hedging or vertical integration.

Specialty powder and equipment know-how

High-purity ceramic powders and specialized deposition equipment are technically complex and supplied by a narrow vendor base; qualification cycles for new suppliers typically run 6–12 months and lead times often extend 12–24 weeks, raising tangible switching costs. This supply tightness gives suppliers leverage on specifications, pricing and delivery cadence. Co-development programs (joint R&D and tooling investments) align incentives but deepen supplier lock-in and dependency.

Geopolitical and logistics risk

Global sourcing exposes Yageo to trade restrictions and chokepoints—export controls, port congestion and 2023–24 Red Sea/Strait of Hormuz tensions have repeatedly disrupted routes. Suppliers may favor larger, long‑term customers, reducing Yageo’s allocations; diversification of origin and partial nearshoring mitigate but do not eliminate risk.

- Trade restrictions

- Port congestion

- Supplier prioritization

- Diversification/nearshoring

ESG and compliance constraints

Responsible sourcing for conflict minerals and environmental compliance narrows viable supplier pools, forcing longer lead times and higher selection barriers. Audits and certifications add onboarding cost and time, increasing supplier bargaining leverage during remediation. Non-compliance risk elevates supplier leverage while buyers wait for corrective actions, and Yageo’s scale improves enforcement but cannot fully offset scarcity effects.

- Responsible sourcing narrows suppliers

- Audits raise onboarding cost/time

- Non-compliance increases supplier leverage

- Yageo scale helps but scarcity remains

Supplier power squeezes margins: Chile 27% Cu, Indonesia ~40% Ni, hedges 60%

Supplier power is high: raw-material concentration (Chile 27% copper 2023; Indonesia ~40% nickel; Russia 30–40% palladium) and narrow ceramic/equipment supply raise switching costs and lead times (qualification 6–12 months; lead times 12–24 weeks). Commodity swings (LME copper +12% in 2024) compress margins; hedges/long‑term contracts (~60% covered in 2024) mitigate but not eliminate risk.

| Metric | Value |

|---|---|

| Chile share (Cu 2023) | 27% |

| Indonesia share (Ni) | ~40% |

| Russia share (Pd) | 30–40% |

| LME copper 2024 | +12% |

| Hedge coverage 2024 | ~60% |

| Supplier lead times | 12–24 wks |

What is included in the product

Tailored Porter's Five Forces analysis for Yageo that uncovers key drivers of competition, supplier and buyer power, and market entry risks, identifying substitutes and disruptive threats to its component business. Includes strategic commentary on pricing influence, barriers protecting incumbents, and implications for Yageo's profitability and market positioning.

A clear, one-sheet summary of Yageo's Five Forces—visualize supplier/customer power, industry rivalry, and threats of substitutes/entrants to speed strategic decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Large OEMs and EMS leverage

Tier-1 OEMs and EMS aggregate massive volumes, creating strong price pressure on suppliers during annual sourcing cycles and scorecard-driven cost-downs.

Buyers routinely shift share among qualified vendors to extract concessions, using volume concentration and long-term program leverage.

Yageo mitigates this through broad product breadth, high reliability and integrated global logistics and consignment support, preserving margin and share.

Design-in and qualification stickiness

Once Yageo components are qualified, switching costs rise as revalidation commonly requires 6–12 months and carries added failure-risk and warranty exposure, tempering buyer power mid-cycle. Buyers typically reopen competition at new design cycles (commonly 2–5 years) to reset pricing. Automotive and industrial approvals such as AEC-Q extend part lifetimes and traceability requirements, prompting periodic rebids often every 3–7 years.

Dual-sourcing and approved vendor lists

Most buyers mandate multi-sourcing, so being one of two or three approved suppliers caps pricing upside and forces volume-based or tiered margins; approved-vendor lists commonly name 2–3 providers. Share allocations can shift quickly with lead-time or quality delta, and customers reallocate volumes based on delivery and PPAP/AEC pass rates. Maintaining top-tier on-time delivery and PPAP/AEC credentials is essential to defend share.

High price sensitivity in commoditized SKUs

Standard resistors and MLCCs are highly substitutable, pushing negotiations to penny-level discounts on components often priced in the $0.01–$0.10 range; buyers evaluate total cost of ownership including packaging, reel sizes and logistics, and in downturns excess inventory magnifies buyer leverage, forcing suppliers to offer tighter terms unless specialty specs or value-add services justify premiums.

- High substitutability → penny-level pricing pressure

- Buyers focus on TCO: packaging, reel sizes, logistics

- Premiums require specialty specs or services

- Downturn inventory increases buyer leverage

Demand cyclicality and inventory swings

Electronics cycles drive abrupt order cuts and pushouts that force price concessions, while automotive and industrial segments—which represented roughly 40% of passive components demand in 2024—offer steadier but still corrective inventory behavior.

Buyers increasingly demand vendor-managed inventory and consignment to shift holding costs to suppliers; Yageo must balance high fab utilization with disciplined pricing to avoid margin erosion amid these swings.

Passive components market $64.3B, auto/industrial 40%; suppliers face yearly sourcing cost pressure

Tier-1 OEMs and EMS concentrate volumes and force aggressive cost-downs during annual sourcing cycles. Buyers shift share among qualified vendors and reopen competition at 2–5 year design cycles, tempering supplier pricing. Yageo defends margins via breadth, reliability, VMI/consignment and AEC-Q qualifications. 2024 passive market ~64.3B with automotive/industrial ~40%.

| Metric | 2024 |

|---|---|

| Passive market | $64.3B |

| Auto/Industrial share | ~40% |

| Typical pricing | $0.01–$0.10 |

Preview Before You Purchase

Yageo Porter's Five Forces Analysis

This preview shows the exact Yageo Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed is the full, professionally formatted file, ready for download and immediate use. What you see here is exactly what will be available to you after payment.