Yankuang Energy Group PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our PESTLE Analysis of Yankuang Energy Group—three to five expert-backed insights on regulatory shifts, market drivers, and environmental risks that could reshape profitability. Designed for investors and strategists, this brief reveals where threats and opportunities lie. Purchase the full report to access the complete, actionable breakdown and templates for immediate use.

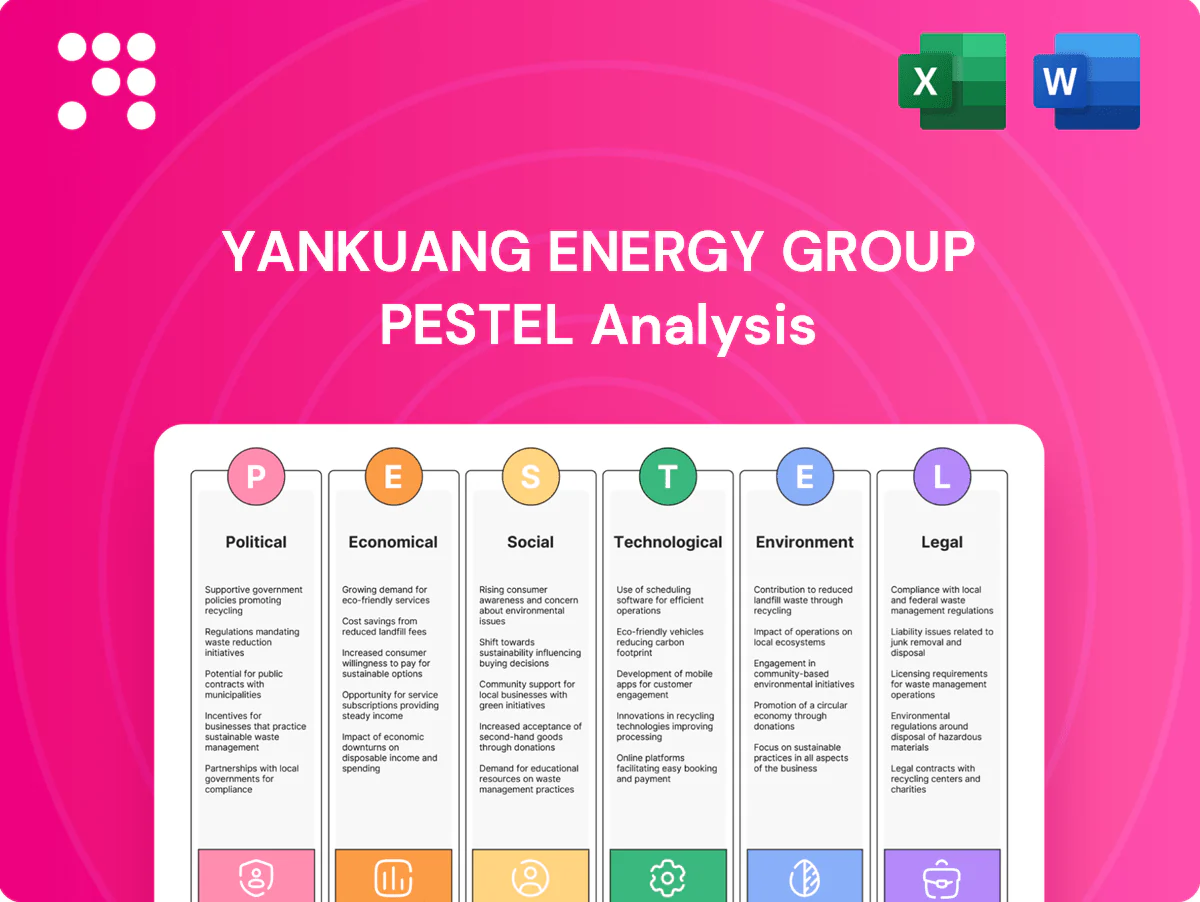

Political factors

China energy security priorities

China’s energy security policy in 2024 maintains coal as a baseload priority — coal-fired generation supplied roughly 60% of power — with continued approvals for capacity and reserve production supporting Yankuang’s coal and power subsidiaries. Yankuang benefits from supportive dispatch rules and mandated stockpiling during shortages, though Beijing’s rapid policy shifts toward emissions targets (peak CO2 by 2030, carbon neutrality by 2060) mean expansion can quickly pivot to restraint; close alignment with provincial planners is critical.

Price interventions and market guidance

Authorities have imposed administrative price bands and stepped-up NDRC oversight since 2023, effectively capping benchmark thermal coal around RMB 700–1,200/tonne in practice to curb volatility; this stabilizes power costs but compresses producer margins during short-lived spikes. Yankuang must manage profitability within these bands and accept that contracting with utilities is increasingly policy-driven rather than purely market-based.

Dual-control on energy intensity

Provincial dual-control targets, typically mandating 1–3% annual cuts in energy intensity and binding total consumption caps, directly constrain coal demand growth and can blunt industrial burn. Stricter targets accelerate fuel-switching and efficiency investments, shifting the mix away from thermal coal. Yankuang faces planning uncertainty as enforcement intensity varies across provinces, and compliance drives mine scheduling and shipment timing to meet regional quotas.

Geopolitical trade dynamics

Geopolitical trade dynamics shape seaborne coal flows and pricing through import/export policies and bilateral relations, with China sourcing significant coal volumes from Indonesia and Australia; coal still supplies about 60% of China’s power generation (2023), so restrictions or domestic-preference rules directly alter Yankuang’s sales mix. Yankuang’s exposure to international markets is both risk and opportunity as logistics and customs changes can swiftly open or close arbitrage windows.

- Import/export rules: shift seaborne pricing

- Domestic preferences: change sales mix and margins

- International exposure: adds market volatility and upside

- Logistics/customs: can rapidly alter arbitrage

SOE governance and local government ties

As a large state-linked energy group supervised by Shandong SASAC and listed on Shanghai SSE (600188), Yankuang operates under SOE governance standards and central/regional performance mandates.

Local governments in Shandong exert strong influence over land use, permitting and infrastructure access, affecting project timelines and costs.

Political backing can ease expansion yet raises public-service and employment expectations; stakeholder coordination with regulators and localities is continuous.

- State owner: Shandong SASAC

- Ticker: 600188 (SSE)

- Key impact: permitting, land, infrastructure

Policy sustains coal baseload (~60%), price bands compress margins as emissions targets loom

State energy policy in 2024 keeps coal as baseload (~60% of power in 2023), supporting Yankuang’s coal and power units while emissions targets (peak CO2 by 2030, neutrality by 2060) create potential for abrupt restraint.

NDRC oversight and de facto thermal coal bands (~RMB 700–1,200/tonne) stabilize prices but compress margins; provincial dual-control cuts (~1–3% annual intensity) constrain demand.

Shandong SASAC ownership (ticker 600188) ensures regulatory support but raises public-service and permitting obligations.

| Factor | Metric (2023/24) | Impact |

|---|---|---|

| Coal share | ~60% power | Baseload support |

| Price band | RMB 700–1,200/t | Margin pressure |

| Dual-control | 1–3% cuts | Demand constraint |

| Ownership | Shandong SASAC, 600188 | Permitting influence |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Yankuang Energy Group, with tailored subpoints linking macro trends to operational, regulatory and market risks and opportunities. Backed by data and forward-looking insights to support executives, investors and scenario planning.

A clean, summarized PESTLE of Yankuang Energy Group for easy reference in meetings or presentations, visually segmented by category to speed stakeholder alignment and support risk and market-positioning discussions.

Economic factors

Coal price cyclicality

Benchmark thermal and coking coal prices (Newcastle, ARA/API2) swing with power and steel demand and global supply shocks, with moves that can exceed 50% year-on-year in stressed periods. Earnings for Yankuang Energy are highly leveraged to price movements versus relatively fixed extraction costs, amplifying volatility in net income. Hedging and long-term offtake contracts smooth cash flow and reduce downside but cap upside, so capital allocation and capex should be timed to cycle positioning.

Domestic power demand outlook

China electricity consumption rose about 6% in 2023 while coal-fired generation remained near 60% of the power mix in 2024 (NEA), underpinning thermal coal offtake for producers like Yankuang. Strong industrial activity, 2023–24 heatwaves and accelerating electrification of transport and heating have driven peak loads. Double-digit annual solar/wind buildouts and efficiency gains add substitution pressure. Yankuang must align coal deliveries to sharper summer/winter seasonal peaks.

Cost inflation and logistics

Rising input costs for explosives, steel, labor and rail tariffs have materially pressured Yankuang's unit cash costs in 2024, while rail and port bottlenecks widened basis differentials during peak seasons.

Operational excellence and proximity to end-markets help protect margins by shortening haulage distances and turnaround times.

Early contracting of rail and shipping slots reduces volatility and secures capacity.

FX and interest rate exposure

Yankuang faces FX sensitivity from foreign-currency debt, equipment imports and growing overseas sales, with earnings exposed to RMB moves; 1-year LPR around 3.45% (mid-2024) means rate cycles materially affect borrowing costs and project NPVs. Prudent treasury management and hedging programs are used to mitigate FX and rate risk, while access to credit markets dictates the timing of expansion.

- Foreign currency debt exposure: import and export-driven

- Interest-rate sensitivity: 1-year LPR ~3.45% (mid-2024)

- Hedging and treasury controls mitigate risk

- Credit access shapes capex timing

Coal-chemical and power diversification

Yankuang Energy's downstream coal-to-chemicals and captive power businesses smooth revenue and absorb volatile coal feedstock, with margins tied tightly to oil/naphtha spreads and regional power tariffs. Integration increases operational and regulatory complexity but materially enhances resilience against commodity swings. High capital intensity necessitates strict project hurdle rates and phased investment.

- Downstream stabilizes cash flow

- Margins driven by oil/naphtha spreads & power tariffs

- Integration = higher complexity, greater resilience

- Capital intensity demands disciplined hurdle rates

Policy sustains coal baseload (~60%), price bands compress margins as emissions targets loom

Yankuang earnings are highly leveraged to benchmark coal prices that have swung over 50% YoY in stressed periods; hedging/offtake limits downside but caps upside. China electricity use rose ~6% in 2023 and coal remained ~60% of generation in 2024, supporting thermal offtake. 1-year LPR ~3.45% (mid-2024) and FX/debt exposures affect project NPVs and capex timing.

| Metric | Value | Impact |

|---|---|---|

| Coal price volatility | >50% YoY moves | High earnings volatility |

| China power mix | Coal ~60% (2024) | Stable thermal demand |

| Electricity demand | +6% (2023) | Peak load pressure |

| 1-yr LPR | ~3.45% (mid-2024) | Borrowing cost sensitivity |

What You See Is What You Get

Yankuang Energy Group PESTLE Analysis

The Yankuang Energy Group PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It presents complete, professionally structured political, economic, social, technological, legal, and environmental insights specific to Yankuang. No placeholders or teasers—this is the final file available for immediate download.

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our PESTLE Analysis of Yankuang Energy Group—three to five expert-backed insights on regulatory shifts, market drivers, and environmental risks that could reshape profitability. Designed for investors and strategists, this brief reveals where threats and opportunities lie. Purchase the full report to access the complete, actionable breakdown and templates for immediate use.

Political factors

China energy security priorities

China’s energy security policy in 2024 maintains coal as a baseload priority — coal-fired generation supplied roughly 60% of power — with continued approvals for capacity and reserve production supporting Yankuang’s coal and power subsidiaries. Yankuang benefits from supportive dispatch rules and mandated stockpiling during shortages, though Beijing’s rapid policy shifts toward emissions targets (peak CO2 by 2030, carbon neutrality by 2060) mean expansion can quickly pivot to restraint; close alignment with provincial planners is critical.

Price interventions and market guidance

Authorities have imposed administrative price bands and stepped-up NDRC oversight since 2023, effectively capping benchmark thermal coal around RMB 700–1,200/tonne in practice to curb volatility; this stabilizes power costs but compresses producer margins during short-lived spikes. Yankuang must manage profitability within these bands and accept that contracting with utilities is increasingly policy-driven rather than purely market-based.

Dual-control on energy intensity

Provincial dual-control targets, typically mandating 1–3% annual cuts in energy intensity and binding total consumption caps, directly constrain coal demand growth and can blunt industrial burn. Stricter targets accelerate fuel-switching and efficiency investments, shifting the mix away from thermal coal. Yankuang faces planning uncertainty as enforcement intensity varies across provinces, and compliance drives mine scheduling and shipment timing to meet regional quotas.

Geopolitical trade dynamics

Geopolitical trade dynamics shape seaborne coal flows and pricing through import/export policies and bilateral relations, with China sourcing significant coal volumes from Indonesia and Australia; coal still supplies about 60% of China’s power generation (2023), so restrictions or domestic-preference rules directly alter Yankuang’s sales mix. Yankuang’s exposure to international markets is both risk and opportunity as logistics and customs changes can swiftly open or close arbitrage windows.

- Import/export rules: shift seaborne pricing

- Domestic preferences: change sales mix and margins

- International exposure: adds market volatility and upside

- Logistics/customs: can rapidly alter arbitrage

SOE governance and local government ties

As a large state-linked energy group supervised by Shandong SASAC and listed on Shanghai SSE (600188), Yankuang operates under SOE governance standards and central/regional performance mandates.

Local governments in Shandong exert strong influence over land use, permitting and infrastructure access, affecting project timelines and costs.

Political backing can ease expansion yet raises public-service and employment expectations; stakeholder coordination with regulators and localities is continuous.

- State owner: Shandong SASAC

- Ticker: 600188 (SSE)

- Key impact: permitting, land, infrastructure

Policy sustains coal baseload (~60%), price bands compress margins as emissions targets loom

State energy policy in 2024 keeps coal as baseload (~60% of power in 2023), supporting Yankuang’s coal and power units while emissions targets (peak CO2 by 2030, neutrality by 2060) create potential for abrupt restraint.

NDRC oversight and de facto thermal coal bands (~RMB 700–1,200/tonne) stabilize prices but compress margins; provincial dual-control cuts (~1–3% annual intensity) constrain demand.

Shandong SASAC ownership (ticker 600188) ensures regulatory support but raises public-service and permitting obligations.

| Factor | Metric (2023/24) | Impact |

|---|---|---|

| Coal share | ~60% power | Baseload support |

| Price band | RMB 700–1,200/t | Margin pressure |

| Dual-control | 1–3% cuts | Demand constraint |

| Ownership | Shandong SASAC, 600188 | Permitting influence |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Yankuang Energy Group, with tailored subpoints linking macro trends to operational, regulatory and market risks and opportunities. Backed by data and forward-looking insights to support executives, investors and scenario planning.

A clean, summarized PESTLE of Yankuang Energy Group for easy reference in meetings or presentations, visually segmented by category to speed stakeholder alignment and support risk and market-positioning discussions.

Economic factors

Coal price cyclicality

Benchmark thermal and coking coal prices (Newcastle, ARA/API2) swing with power and steel demand and global supply shocks, with moves that can exceed 50% year-on-year in stressed periods. Earnings for Yankuang Energy are highly leveraged to price movements versus relatively fixed extraction costs, amplifying volatility in net income. Hedging and long-term offtake contracts smooth cash flow and reduce downside but cap upside, so capital allocation and capex should be timed to cycle positioning.

Domestic power demand outlook

China electricity consumption rose about 6% in 2023 while coal-fired generation remained near 60% of the power mix in 2024 (NEA), underpinning thermal coal offtake for producers like Yankuang. Strong industrial activity, 2023–24 heatwaves and accelerating electrification of transport and heating have driven peak loads. Double-digit annual solar/wind buildouts and efficiency gains add substitution pressure. Yankuang must align coal deliveries to sharper summer/winter seasonal peaks.

Cost inflation and logistics

Rising input costs for explosives, steel, labor and rail tariffs have materially pressured Yankuang's unit cash costs in 2024, while rail and port bottlenecks widened basis differentials during peak seasons.

Operational excellence and proximity to end-markets help protect margins by shortening haulage distances and turnaround times.

Early contracting of rail and shipping slots reduces volatility and secures capacity.

FX and interest rate exposure

Yankuang faces FX sensitivity from foreign-currency debt, equipment imports and growing overseas sales, with earnings exposed to RMB moves; 1-year LPR around 3.45% (mid-2024) means rate cycles materially affect borrowing costs and project NPVs. Prudent treasury management and hedging programs are used to mitigate FX and rate risk, while access to credit markets dictates the timing of expansion.

- Foreign currency debt exposure: import and export-driven

- Interest-rate sensitivity: 1-year LPR ~3.45% (mid-2024)

- Hedging and treasury controls mitigate risk

- Credit access shapes capex timing

Coal-chemical and power diversification

Yankuang Energy's downstream coal-to-chemicals and captive power businesses smooth revenue and absorb volatile coal feedstock, with margins tied tightly to oil/naphtha spreads and regional power tariffs. Integration increases operational and regulatory complexity but materially enhances resilience against commodity swings. High capital intensity necessitates strict project hurdle rates and phased investment.

- Downstream stabilizes cash flow

- Margins driven by oil/naphtha spreads & power tariffs

- Integration = higher complexity, greater resilience

- Capital intensity demands disciplined hurdle rates

Policy sustains coal baseload (~60%), price bands compress margins as emissions targets loom

Yankuang earnings are highly leveraged to benchmark coal prices that have swung over 50% YoY in stressed periods; hedging/offtake limits downside but caps upside. China electricity use rose ~6% in 2023 and coal remained ~60% of generation in 2024, supporting thermal offtake. 1-year LPR ~3.45% (mid-2024) and FX/debt exposures affect project NPVs and capex timing.

| Metric | Value | Impact |

|---|---|---|

| Coal price volatility | >50% YoY moves | High earnings volatility |

| China power mix | Coal ~60% (2024) | Stable thermal demand |

| Electricity demand | +6% (2023) | Peak load pressure |

| 1-yr LPR | ~3.45% (mid-2024) | Borrowing cost sensitivity |

What You See Is What You Get

Yankuang Energy Group PESTLE Analysis

The Yankuang Energy Group PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It presents complete, professionally structured political, economic, social, technological, legal, and environmental insights specific to Yankuang. No placeholders or teasers—this is the final file available for immediate download.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our PESTLE Analysis of Yankuang Energy Group—three to five expert-backed insights on regulatory shifts, market drivers, and environmental risks that could reshape profitability. Designed for investors and strategists, this brief reveals where threats and opportunities lie. Purchase the full report to access the complete, actionable breakdown and templates for immediate use.

Political factors

China energy security priorities

China’s energy security policy in 2024 maintains coal as a baseload priority — coal-fired generation supplied roughly 60% of power — with continued approvals for capacity and reserve production supporting Yankuang’s coal and power subsidiaries. Yankuang benefits from supportive dispatch rules and mandated stockpiling during shortages, though Beijing’s rapid policy shifts toward emissions targets (peak CO2 by 2030, carbon neutrality by 2060) mean expansion can quickly pivot to restraint; close alignment with provincial planners is critical.

Price interventions and market guidance

Authorities have imposed administrative price bands and stepped-up NDRC oversight since 2023, effectively capping benchmark thermal coal around RMB 700–1,200/tonne in practice to curb volatility; this stabilizes power costs but compresses producer margins during short-lived spikes. Yankuang must manage profitability within these bands and accept that contracting with utilities is increasingly policy-driven rather than purely market-based.

Dual-control on energy intensity

Provincial dual-control targets, typically mandating 1–3% annual cuts in energy intensity and binding total consumption caps, directly constrain coal demand growth and can blunt industrial burn. Stricter targets accelerate fuel-switching and efficiency investments, shifting the mix away from thermal coal. Yankuang faces planning uncertainty as enforcement intensity varies across provinces, and compliance drives mine scheduling and shipment timing to meet regional quotas.

Geopolitical trade dynamics

Geopolitical trade dynamics shape seaborne coal flows and pricing through import/export policies and bilateral relations, with China sourcing significant coal volumes from Indonesia and Australia; coal still supplies about 60% of China’s power generation (2023), so restrictions or domestic-preference rules directly alter Yankuang’s sales mix. Yankuang’s exposure to international markets is both risk and opportunity as logistics and customs changes can swiftly open or close arbitrage windows.

- Import/export rules: shift seaborne pricing

- Domestic preferences: change sales mix and margins

- International exposure: adds market volatility and upside

- Logistics/customs: can rapidly alter arbitrage

SOE governance and local government ties

As a large state-linked energy group supervised by Shandong SASAC and listed on Shanghai SSE (600188), Yankuang operates under SOE governance standards and central/regional performance mandates.

Local governments in Shandong exert strong influence over land use, permitting and infrastructure access, affecting project timelines and costs.

Political backing can ease expansion yet raises public-service and employment expectations; stakeholder coordination with regulators and localities is continuous.

- State owner: Shandong SASAC

- Ticker: 600188 (SSE)

- Key impact: permitting, land, infrastructure

Policy sustains coal baseload (~60%), price bands compress margins as emissions targets loom

State energy policy in 2024 keeps coal as baseload (~60% of power in 2023), supporting Yankuang’s coal and power units while emissions targets (peak CO2 by 2030, neutrality by 2060) create potential for abrupt restraint.

NDRC oversight and de facto thermal coal bands (~RMB 700–1,200/tonne) stabilize prices but compress margins; provincial dual-control cuts (~1–3% annual intensity) constrain demand.

Shandong SASAC ownership (ticker 600188) ensures regulatory support but raises public-service and permitting obligations.

| Factor | Metric (2023/24) | Impact |

|---|---|---|

| Coal share | ~60% power | Baseload support |

| Price band | RMB 700–1,200/t | Margin pressure |

| Dual-control | 1–3% cuts | Demand constraint |

| Ownership | Shandong SASAC, 600188 | Permitting influence |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Yankuang Energy Group, with tailored subpoints linking macro trends to operational, regulatory and market risks and opportunities. Backed by data and forward-looking insights to support executives, investors and scenario planning.

A clean, summarized PESTLE of Yankuang Energy Group for easy reference in meetings or presentations, visually segmented by category to speed stakeholder alignment and support risk and market-positioning discussions.

Economic factors

Coal price cyclicality

Benchmark thermal and coking coal prices (Newcastle, ARA/API2) swing with power and steel demand and global supply shocks, with moves that can exceed 50% year-on-year in stressed periods. Earnings for Yankuang Energy are highly leveraged to price movements versus relatively fixed extraction costs, amplifying volatility in net income. Hedging and long-term offtake contracts smooth cash flow and reduce downside but cap upside, so capital allocation and capex should be timed to cycle positioning.

Domestic power demand outlook

China electricity consumption rose about 6% in 2023 while coal-fired generation remained near 60% of the power mix in 2024 (NEA), underpinning thermal coal offtake for producers like Yankuang. Strong industrial activity, 2023–24 heatwaves and accelerating electrification of transport and heating have driven peak loads. Double-digit annual solar/wind buildouts and efficiency gains add substitution pressure. Yankuang must align coal deliveries to sharper summer/winter seasonal peaks.

Cost inflation and logistics

Rising input costs for explosives, steel, labor and rail tariffs have materially pressured Yankuang's unit cash costs in 2024, while rail and port bottlenecks widened basis differentials during peak seasons.

Operational excellence and proximity to end-markets help protect margins by shortening haulage distances and turnaround times.

Early contracting of rail and shipping slots reduces volatility and secures capacity.

FX and interest rate exposure

Yankuang faces FX sensitivity from foreign-currency debt, equipment imports and growing overseas sales, with earnings exposed to RMB moves; 1-year LPR around 3.45% (mid-2024) means rate cycles materially affect borrowing costs and project NPVs. Prudent treasury management and hedging programs are used to mitigate FX and rate risk, while access to credit markets dictates the timing of expansion.

- Foreign currency debt exposure: import and export-driven

- Interest-rate sensitivity: 1-year LPR ~3.45% (mid-2024)

- Hedging and treasury controls mitigate risk

- Credit access shapes capex timing

Coal-chemical and power diversification

Yankuang Energy's downstream coal-to-chemicals and captive power businesses smooth revenue and absorb volatile coal feedstock, with margins tied tightly to oil/naphtha spreads and regional power tariffs. Integration increases operational and regulatory complexity but materially enhances resilience against commodity swings. High capital intensity necessitates strict project hurdle rates and phased investment.

- Downstream stabilizes cash flow

- Margins driven by oil/naphtha spreads & power tariffs

- Integration = higher complexity, greater resilience

- Capital intensity demands disciplined hurdle rates

Policy sustains coal baseload (~60%), price bands compress margins as emissions targets loom

Yankuang earnings are highly leveraged to benchmark coal prices that have swung over 50% YoY in stressed periods; hedging/offtake limits downside but caps upside. China electricity use rose ~6% in 2023 and coal remained ~60% of generation in 2024, supporting thermal offtake. 1-year LPR ~3.45% (mid-2024) and FX/debt exposures affect project NPVs and capex timing.

| Metric | Value | Impact |

|---|---|---|

| Coal price volatility | >50% YoY moves | High earnings volatility |

| China power mix | Coal ~60% (2024) | Stable thermal demand |

| Electricity demand | +6% (2023) | Peak load pressure |

| 1-yr LPR | ~3.45% (mid-2024) | Borrowing cost sensitivity |

What You See Is What You Get

Yankuang Energy Group PESTLE Analysis

The Yankuang Energy Group PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It presents complete, professionally structured political, economic, social, technological, legal, and environmental insights specific to Yankuang. No placeholders or teasers—this is the final file available for immediate download.