Yes Bank SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Yes Bank’s SWOT analysis highlights strong retail growth and digital initiatives, balanced against capital and governance challenges that shaped recent recovery. Strengths include brand resurgence and diversified corporate lending; threats stem from regulatory scrutiny and competitive pressures. Want the full strategic picture? Purchase the complete SWOT report for an editable, research-backed Word and Excel package to plan, pitch, or invest with confidence.

Strengths

Universal product suite

Yes Bank’s universal product suite spans corporate, retail, MSME, investment banking and wealth management, enabling full-service coverage across client lifecycles. This breadth supports strong cross-sell opportunities and deeper relationships, reflected in a diversified revenue mix from both interest and fee income. With a nationwide network of over 1,000 branches and 12,000 employees, the bank shows resilience through multiple income streams.

Digital-first delivery

Yes Bank's digital-first delivery powers onboarding, payments, lending and self-serve channels, driving faster turnaround and lower cost-to-serve; digital customers reportedly exceeded 3 million by Mar 2025 with digital volumes rising materially year-over-year. The bank cites sub-24-hour retail onboarding and API-led payments enabling quicker disbursals and operational scalability. Data-driven personalization and analytics-led risk controls have reduced delinquency hotspots and improved cross-sell conversion rates.

Diversified client base

Yes Bank serves large corporates, mid-market firms, MSMEs and retail customers, spreading exposure across client segments to reduce concentration risk and smooth earnings volatility. The bank offers tailored products—corporate lending, mid-market cash management, MSME credit and retail mortgages—to match segment needs and improve margins. Cross-segment referrals and ecosystem partnerships drive fee income and customer stickiness.

Customer-centric approach

Yes Bank's customer-centric approach emphasizes relationship banking and tailored advisory, delivering bundled transaction, credit and wealth solutions that increase client stickiness and cross-sell ratios.

High service quality and responsiveness act as differentiators, reinforced by structured feedback loops and digital voice-of-customer tools that refine product design and advisory effectiveness.

- Relationship banking focus

- Bundled transaction-credit-wealth

- Service quality & responsiveness

- Feedback loops for product refinement

Partnership and ecosystem play

Yes Bank's partnership and ecosystem play spans collaborations with fintechs, payment players and platforms that accelerate product innovation and distribution through API-led integration, co-lending and embedded finance, expanding reach into new customer pools and creating diversified fee streams.

Universal banking across segments, 1,000+ branches, >3M digital users, sub-24h onboarding

Yes Bank’s universal suite across corporate, retail, MSME, investment banking and wealth supports strong cross-sell and diversified interest-plus-fee revenue. A nationwide network of 1,000+ branches and ~12,000 employees underpins distribution resilience. Digital-first delivery boasts >3 million digital customers (Mar 2025) and sub-24-hour retail onboarding, while fintech/API partnerships expand co-lending and embedded-fee channels.

| Metric | Value |

|---|---|

| Branches | 1,000+ |

| Employees | ~12,000 |

| Digital customers (Mar 2025) | >3,000,000 |

| Retail onboarding | Sub-24-hour |

What is included in the product

Provides a concise SWOT overview of Yes Bank, highlighting internal strengths and weaknesses alongside external opportunities and threats to assess its competitive position and strategic risks.

Provides a concise Yes Bank SWOT matrix for fast, visual strategy alignment, highlighting key strengths, weaknesses, opportunities, and risks to accelerate stakeholder decisions and remedial planning.

Weaknesses

Asset quality overhang

Asset quality overhang from the 2018-20 crisis (GNPA peaked near 18% in 2018) and a still-significant stressed/restructured book into 2024 keeps investors cautious and demands higher risk premia; elevated credit costs have repeatedly weighed on RoA and profitability, and the bank remains under heightened regulatory and investor scrutiny on underwriting standards and recovery performance.

Brand trust rebuild

Lingering perception gaps versus top-tier peers—HDFC/ICICI CASA >40% versus Yes Bank CASA ~18%—hamper attraction of low-cost current/savings balances, slowing CASA growth and ability to command premium pricing. Restoring trust requires several consecutive quarters of consistent profitability and stable asset-quality metrics to rebuild confidence. Communication and governance transparency gaps must be closed via clearer disclosures, stronger board oversight and regular investor engagement.

Margin sensitivity

Yes Bank's net interest margins face pressure amid intense deposit competition, forcing reliance on higher pricing to secure stable CASA and term funding. The bank's ability to manage mix-shift toward lower-yielding assets and contain cost of funds is constrained, compressing spread recovery. Volatile rate cycles leave limited headroom to pass on costs without hurting loan growth and margins.

Operational complexity

Full-service scope increases process and compliance burden, raising operating complexity across retail, corporate and treasury functions and stretching control frameworks. Higher ongoing spend on technology, risk management and product stacks elevates operating expenses and requires continual capital allocation. Integration challenges across segments and digital, branch and third-party channels slow product rollouts and can impede change management.

- Operational breadth: multiplatform compliance and control strain

- Cost pressure: elevated tech, risk and product maintenance

- Integration risk: cross-segment/channel alignment challenges

- Change velocity: slower implementation and governance cycles

Talent retention risk

Talent retention risk: Yes Bank faces intense competition for experienced bankers and fintech/tech talent, increasing hiring and retention costs and pressuring margins; loss of relationship managers or credit officers can disrupt client continuity and deal execution, while limited succession depth in risk and credit functions raises concentration and operational risk.

- Competitive hiring drives up compensation and turnover

- Higher retention costs squeeze NIMs and operating expenses

- Relationship and execution continuity at risk from attrition

- Succession depth needed in risk and credit to avoid concentration

Legacy asset-quality overhang and low CASA keep credit costs, funding mix and Opex pressured

Asset-quality overhang from the 2018 crisis (GNPA peaked near 18%) and a still-significant stressed/restructured book into 2024 keep credit costs and scrutiny elevated; CASA lag (~18% for Yes Bank vs >40% at HDFC/ICICI) pressures funding mix and NIMs; full-service complexity raises Opex and integration risk; talent attrition inflates hiring/retention costs.

| Metric | Value | Year |

|---|---|---|

| GNPA peak | ~18% | 2018 |

| Yes Bank CASA | ~18% | 2024 |

| HDFC/ICICI CASA | >40% | 2024 |

Preview Before You Purchase

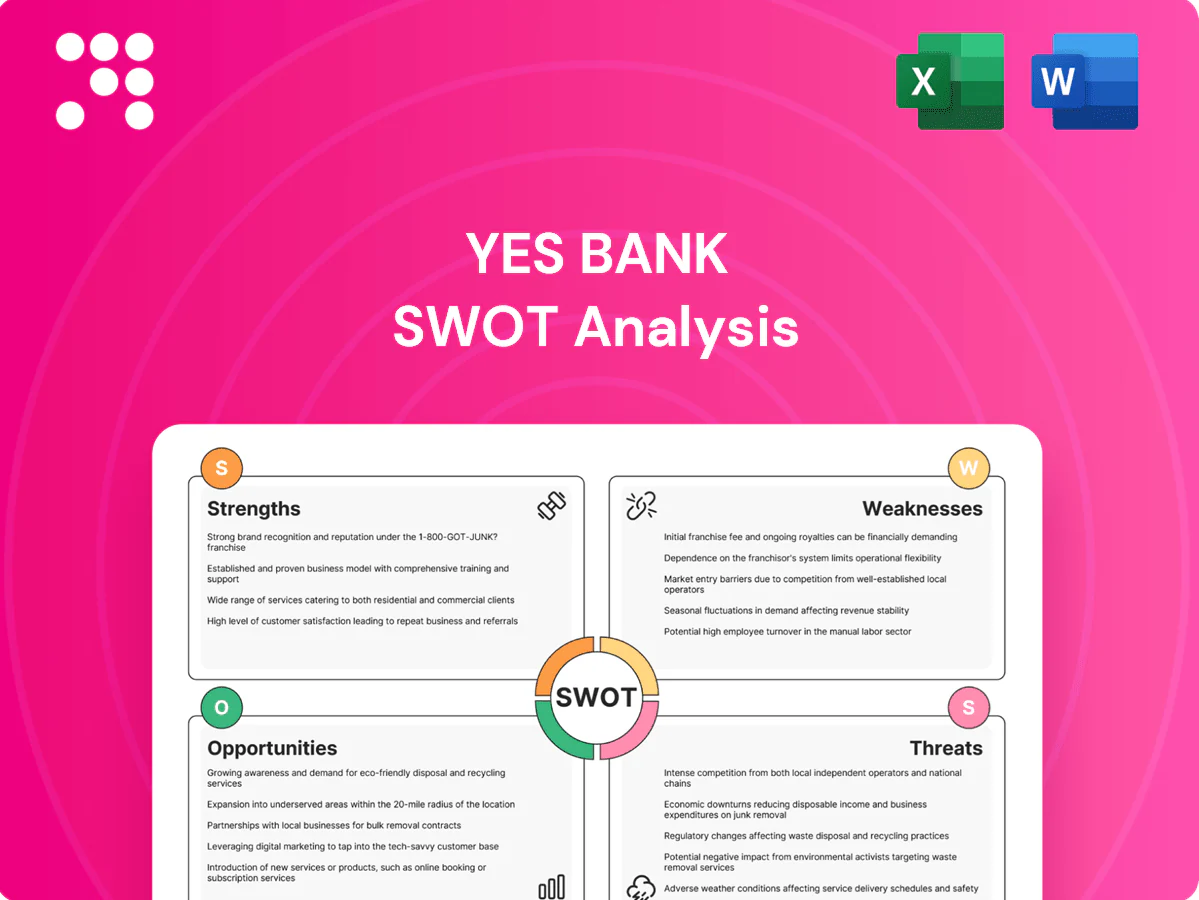

Yes Bank SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; buy to unlock the complete, editable version with detailed strengths, weaknesses, opportunities and threats for Yes Bank.

Go Beyond the Preview—Access the Full Strategic Report

Yes Bank’s SWOT analysis highlights strong retail growth and digital initiatives, balanced against capital and governance challenges that shaped recent recovery. Strengths include brand resurgence and diversified corporate lending; threats stem from regulatory scrutiny and competitive pressures. Want the full strategic picture? Purchase the complete SWOT report for an editable, research-backed Word and Excel package to plan, pitch, or invest with confidence.

Strengths

Universal product suite

Yes Bank’s universal product suite spans corporate, retail, MSME, investment banking and wealth management, enabling full-service coverage across client lifecycles. This breadth supports strong cross-sell opportunities and deeper relationships, reflected in a diversified revenue mix from both interest and fee income. With a nationwide network of over 1,000 branches and 12,000 employees, the bank shows resilience through multiple income streams.

Digital-first delivery

Yes Bank's digital-first delivery powers onboarding, payments, lending and self-serve channels, driving faster turnaround and lower cost-to-serve; digital customers reportedly exceeded 3 million by Mar 2025 with digital volumes rising materially year-over-year. The bank cites sub-24-hour retail onboarding and API-led payments enabling quicker disbursals and operational scalability. Data-driven personalization and analytics-led risk controls have reduced delinquency hotspots and improved cross-sell conversion rates.

Diversified client base

Yes Bank serves large corporates, mid-market firms, MSMEs and retail customers, spreading exposure across client segments to reduce concentration risk and smooth earnings volatility. The bank offers tailored products—corporate lending, mid-market cash management, MSME credit and retail mortgages—to match segment needs and improve margins. Cross-segment referrals and ecosystem partnerships drive fee income and customer stickiness.

Customer-centric approach

Yes Bank's customer-centric approach emphasizes relationship banking and tailored advisory, delivering bundled transaction, credit and wealth solutions that increase client stickiness and cross-sell ratios.

High service quality and responsiveness act as differentiators, reinforced by structured feedback loops and digital voice-of-customer tools that refine product design and advisory effectiveness.

- Relationship banking focus

- Bundled transaction-credit-wealth

- Service quality & responsiveness

- Feedback loops for product refinement

Partnership and ecosystem play

Yes Bank's partnership and ecosystem play spans collaborations with fintechs, payment players and platforms that accelerate product innovation and distribution through API-led integration, co-lending and embedded finance, expanding reach into new customer pools and creating diversified fee streams.

Universal banking across segments, 1,000+ branches, >3M digital users, sub-24h onboarding

Yes Bank’s universal suite across corporate, retail, MSME, investment banking and wealth supports strong cross-sell and diversified interest-plus-fee revenue. A nationwide network of 1,000+ branches and ~12,000 employees underpins distribution resilience. Digital-first delivery boasts >3 million digital customers (Mar 2025) and sub-24-hour retail onboarding, while fintech/API partnerships expand co-lending and embedded-fee channels.

| Metric | Value |

|---|---|

| Branches | 1,000+ |

| Employees | ~12,000 |

| Digital customers (Mar 2025) | >3,000,000 |

| Retail onboarding | Sub-24-hour |

What is included in the product

Provides a concise SWOT overview of Yes Bank, highlighting internal strengths and weaknesses alongside external opportunities and threats to assess its competitive position and strategic risks.

Provides a concise Yes Bank SWOT matrix for fast, visual strategy alignment, highlighting key strengths, weaknesses, opportunities, and risks to accelerate stakeholder decisions and remedial planning.

Weaknesses

Asset quality overhang

Asset quality overhang from the 2018-20 crisis (GNPA peaked near 18% in 2018) and a still-significant stressed/restructured book into 2024 keeps investors cautious and demands higher risk premia; elevated credit costs have repeatedly weighed on RoA and profitability, and the bank remains under heightened regulatory and investor scrutiny on underwriting standards and recovery performance.

Brand trust rebuild

Lingering perception gaps versus top-tier peers—HDFC/ICICI CASA >40% versus Yes Bank CASA ~18%—hamper attraction of low-cost current/savings balances, slowing CASA growth and ability to command premium pricing. Restoring trust requires several consecutive quarters of consistent profitability and stable asset-quality metrics to rebuild confidence. Communication and governance transparency gaps must be closed via clearer disclosures, stronger board oversight and regular investor engagement.

Margin sensitivity

Yes Bank's net interest margins face pressure amid intense deposit competition, forcing reliance on higher pricing to secure stable CASA and term funding. The bank's ability to manage mix-shift toward lower-yielding assets and contain cost of funds is constrained, compressing spread recovery. Volatile rate cycles leave limited headroom to pass on costs without hurting loan growth and margins.

Operational complexity

Full-service scope increases process and compliance burden, raising operating complexity across retail, corporate and treasury functions and stretching control frameworks. Higher ongoing spend on technology, risk management and product stacks elevates operating expenses and requires continual capital allocation. Integration challenges across segments and digital, branch and third-party channels slow product rollouts and can impede change management.

- Operational breadth: multiplatform compliance and control strain

- Cost pressure: elevated tech, risk and product maintenance

- Integration risk: cross-segment/channel alignment challenges

- Change velocity: slower implementation and governance cycles

Talent retention risk

Talent retention risk: Yes Bank faces intense competition for experienced bankers and fintech/tech talent, increasing hiring and retention costs and pressuring margins; loss of relationship managers or credit officers can disrupt client continuity and deal execution, while limited succession depth in risk and credit functions raises concentration and operational risk.

- Competitive hiring drives up compensation and turnover

- Higher retention costs squeeze NIMs and operating expenses

- Relationship and execution continuity at risk from attrition

- Succession depth needed in risk and credit to avoid concentration

Legacy asset-quality overhang and low CASA keep credit costs, funding mix and Opex pressured

Asset-quality overhang from the 2018 crisis (GNPA peaked near 18%) and a still-significant stressed/restructured book into 2024 keep credit costs and scrutiny elevated; CASA lag (~18% for Yes Bank vs >40% at HDFC/ICICI) pressures funding mix and NIMs; full-service complexity raises Opex and integration risk; talent attrition inflates hiring/retention costs.

| Metric | Value | Year |

|---|---|---|

| GNPA peak | ~18% | 2018 |

| Yes Bank CASA | ~18% | 2024 |

| HDFC/ICICI CASA | >40% | 2024 |

Preview Before You Purchase

Yes Bank SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; buy to unlock the complete, editable version with detailed strengths, weaknesses, opportunities and threats for Yes Bank.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Yes Bank’s SWOT analysis highlights strong retail growth and digital initiatives, balanced against capital and governance challenges that shaped recent recovery. Strengths include brand resurgence and diversified corporate lending; threats stem from regulatory scrutiny and competitive pressures. Want the full strategic picture? Purchase the complete SWOT report for an editable, research-backed Word and Excel package to plan, pitch, or invest with confidence.

Strengths

Universal product suite

Yes Bank’s universal product suite spans corporate, retail, MSME, investment banking and wealth management, enabling full-service coverage across client lifecycles. This breadth supports strong cross-sell opportunities and deeper relationships, reflected in a diversified revenue mix from both interest and fee income. With a nationwide network of over 1,000 branches and 12,000 employees, the bank shows resilience through multiple income streams.

Digital-first delivery

Yes Bank's digital-first delivery powers onboarding, payments, lending and self-serve channels, driving faster turnaround and lower cost-to-serve; digital customers reportedly exceeded 3 million by Mar 2025 with digital volumes rising materially year-over-year. The bank cites sub-24-hour retail onboarding and API-led payments enabling quicker disbursals and operational scalability. Data-driven personalization and analytics-led risk controls have reduced delinquency hotspots and improved cross-sell conversion rates.

Diversified client base

Yes Bank serves large corporates, mid-market firms, MSMEs and retail customers, spreading exposure across client segments to reduce concentration risk and smooth earnings volatility. The bank offers tailored products—corporate lending, mid-market cash management, MSME credit and retail mortgages—to match segment needs and improve margins. Cross-segment referrals and ecosystem partnerships drive fee income and customer stickiness.

Customer-centric approach

Yes Bank's customer-centric approach emphasizes relationship banking and tailored advisory, delivering bundled transaction, credit and wealth solutions that increase client stickiness and cross-sell ratios.

High service quality and responsiveness act as differentiators, reinforced by structured feedback loops and digital voice-of-customer tools that refine product design and advisory effectiveness.

- Relationship banking focus

- Bundled transaction-credit-wealth

- Service quality & responsiveness

- Feedback loops for product refinement

Partnership and ecosystem play

Yes Bank's partnership and ecosystem play spans collaborations with fintechs, payment players and platforms that accelerate product innovation and distribution through API-led integration, co-lending and embedded finance, expanding reach into new customer pools and creating diversified fee streams.

Universal banking across segments, 1,000+ branches, >3M digital users, sub-24h onboarding

Yes Bank’s universal suite across corporate, retail, MSME, investment banking and wealth supports strong cross-sell and diversified interest-plus-fee revenue. A nationwide network of 1,000+ branches and ~12,000 employees underpins distribution resilience. Digital-first delivery boasts >3 million digital customers (Mar 2025) and sub-24-hour retail onboarding, while fintech/API partnerships expand co-lending and embedded-fee channels.

| Metric | Value |

|---|---|

| Branches | 1,000+ |

| Employees | ~12,000 |

| Digital customers (Mar 2025) | >3,000,000 |

| Retail onboarding | Sub-24-hour |

What is included in the product

Provides a concise SWOT overview of Yes Bank, highlighting internal strengths and weaknesses alongside external opportunities and threats to assess its competitive position and strategic risks.

Provides a concise Yes Bank SWOT matrix for fast, visual strategy alignment, highlighting key strengths, weaknesses, opportunities, and risks to accelerate stakeholder decisions and remedial planning.

Weaknesses

Asset quality overhang

Asset quality overhang from the 2018-20 crisis (GNPA peaked near 18% in 2018) and a still-significant stressed/restructured book into 2024 keeps investors cautious and demands higher risk premia; elevated credit costs have repeatedly weighed on RoA and profitability, and the bank remains under heightened regulatory and investor scrutiny on underwriting standards and recovery performance.

Brand trust rebuild

Lingering perception gaps versus top-tier peers—HDFC/ICICI CASA >40% versus Yes Bank CASA ~18%—hamper attraction of low-cost current/savings balances, slowing CASA growth and ability to command premium pricing. Restoring trust requires several consecutive quarters of consistent profitability and stable asset-quality metrics to rebuild confidence. Communication and governance transparency gaps must be closed via clearer disclosures, stronger board oversight and regular investor engagement.

Margin sensitivity

Yes Bank's net interest margins face pressure amid intense deposit competition, forcing reliance on higher pricing to secure stable CASA and term funding. The bank's ability to manage mix-shift toward lower-yielding assets and contain cost of funds is constrained, compressing spread recovery. Volatile rate cycles leave limited headroom to pass on costs without hurting loan growth and margins.

Operational complexity

Full-service scope increases process and compliance burden, raising operating complexity across retail, corporate and treasury functions and stretching control frameworks. Higher ongoing spend on technology, risk management and product stacks elevates operating expenses and requires continual capital allocation. Integration challenges across segments and digital, branch and third-party channels slow product rollouts and can impede change management.

- Operational breadth: multiplatform compliance and control strain

- Cost pressure: elevated tech, risk and product maintenance

- Integration risk: cross-segment/channel alignment challenges

- Change velocity: slower implementation and governance cycles

Talent retention risk

Talent retention risk: Yes Bank faces intense competition for experienced bankers and fintech/tech talent, increasing hiring and retention costs and pressuring margins; loss of relationship managers or credit officers can disrupt client continuity and deal execution, while limited succession depth in risk and credit functions raises concentration and operational risk.

- Competitive hiring drives up compensation and turnover

- Higher retention costs squeeze NIMs and operating expenses

- Relationship and execution continuity at risk from attrition

- Succession depth needed in risk and credit to avoid concentration

Legacy asset-quality overhang and low CASA keep credit costs, funding mix and Opex pressured

Asset-quality overhang from the 2018 crisis (GNPA peaked near 18%) and a still-significant stressed/restructured book into 2024 keep credit costs and scrutiny elevated; CASA lag (~18% for Yes Bank vs >40% at HDFC/ICICI) pressures funding mix and NIMs; full-service complexity raises Opex and integration risk; talent attrition inflates hiring/retention costs.

| Metric | Value | Year |

|---|---|---|

| GNPA peak | ~18% | 2018 |

| Yes Bank CASA | ~18% | 2024 |

| HDFC/ICICI CASA | >40% | 2024 |

Preview Before You Purchase

Yes Bank SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; buy to unlock the complete, editable version with detailed strengths, weaknesses, opportunities and threats for Yes Bank.