Youngone Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

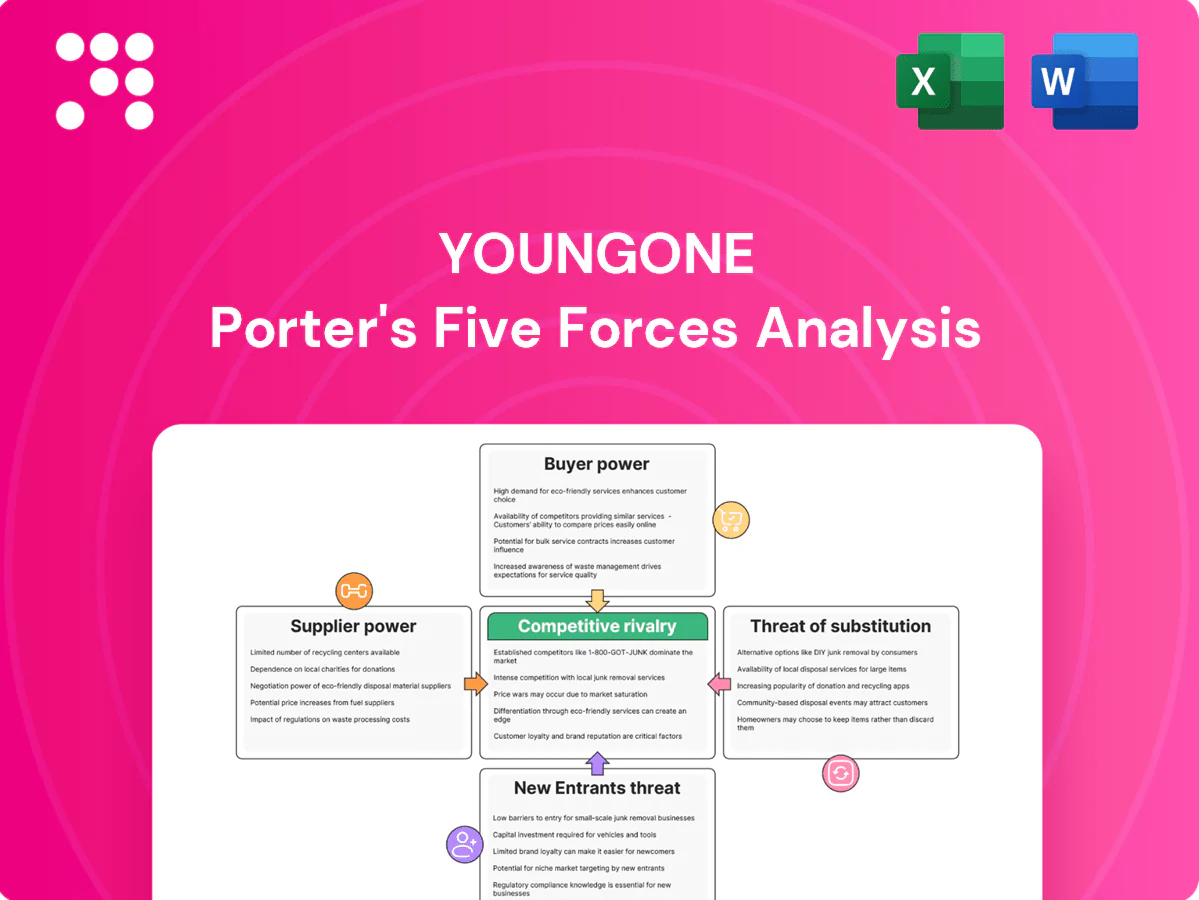

Youngone Porter's Five Forces snapshot highlights supplier leverage, buyer power, substitution risks and competitive rivalry—revealing strategic pressure points and potential growth levers. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Youngone’s competitive dynamics in detail.

Suppliers Bargaining Power

Vertical integration dampens supplier leverage

Youngone’s in-house fabric mills, trim production and logistics cut reliance on external suppliers, lowering input-price vulnerability and securing supply continuity. This vertical integration enables backward planning and compresses design-to-production cycles, accelerating time-to-market. Internal capacity also strengthens negotiating leverage with remaining vendors, shifting bargaining power in Youngone’s favor.

Specialized materials suppliers remain influential

Specialized inputs like high-performance membranes, technical foams, and advanced chemicals are sourced from a limited group of certified suppliers, giving those vendors notable leverage over Youngone. Certification requirements, IP protections, and stringent specifications narrow alternatives, allowing premiums and extended lead times. Dual- and multi-sourcing mitigate risk but seldom fully neutralize supplier bargaining power.

Commodity price volatility transmits upstream power

Global polyester, nylon, cotton and energy prices remain cyclical — Brent crude surged to about $130/bbl in 2022 and averaged near $87/bbl in 2023, feeding feedstock swings that have caused raw-material cost moves often in the 20–40% range across 2021–24. Even with vertical integration, Youngone faces margin volatility and tougher quoting when inputs jump. Hedging programs and renewables cap exposure but cannot eliminate swings, and customer resistance to full pass-throughs intensifies margin squeeze.

Geographic concentration and logistics risk

Geographic concentration exposes Youngone to weather events, port congestion and geopolitical shocks that can sever key raw-material corridors; about 80% of global merchandise trade by volume moves by sea (UNCTAD). Limited nearby alternatives increase local supplier leverage, while multi-country sourcing diversifies risk but raises coordination and logistics costs; supplier development programs can gradually reduce regional bottlenecks.

- 80% global trade by volume via sea (UNCTAD)

- Local suppliers gain leverage when alternatives scarce

- Multi-country sourcing = higher coordination costs

- Supplier development reduces regional bottlenecks over time

Sustainability and compliance elevate supplier gatekeeping

Sustainability mandates—OEKO-TEX reporting over 12,000 certified companies and bluesign partnerships near 3,000 in 2024—shrink Youngone’s approved supplier pool, raising supplier gatekeeping and price leverage.

Mandatory traceability covering roughly 25% of apparel volume in 2024 and a ~40% rise in compliance audits (2020–24) increase switching frictions and data transparency demands.

Certified suppliers exploit certification scarcity for higher margins, while Youngone’s vertical investments in cleaner processes and CAPEX reallocations reclaim control.

- Certification density: OEKO-TEX ~12,000; bluesign ~3,000 (2024)

- Traceability coverage ~25% (2024)

- Compliance audits +40% (2020–24)

- Verticalization reduces supplier leverage via in-house clean processes

Verticalization trims supplier risk; certifications scarce, Brent at $87, traceability 25%

Youngone’s verticalization (in-house mills, trims, logistics) reduces supplier dependence and boosts leverage. Specialized inputs and certification scarcity (OEKO-TEX ~12,000; bluesign ~3,000 in 2024) keep supplier power elevated. Commodity swings (Brent ~$87 avg 2023) and 25% traceability coverage raise switching costs and margin volatility.

| Metric | Value |

|---|---|

| Sea trade share (UNCTAD) | 80% |

| Brent avg 2023 | $87/bbl |

| OEKO-TEX (2024) | ~12,000 |

| bluesign (2024) | ~3,000 |

| Traceability coverage (2024) | ~25% |

| Compliance audits (2020–24) | +40% |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, substitutes and entry barriers tailored exclusively for Youngone, identifying disruptive threats and strategic levers; fully editable for reports and decks.

One-sheet Porter's Five Forces for Youngone — instantly visualize supplier, buyer, competitor, entrant, and substitute pressure with a crisp spider chart for faster strategic decisions. Customize scores, swap in current data, and paste directly into pitch decks or board reports for immediate clarity.

Customers Bargaining Power

Concentrated global brand buyers wield price pressure

Large outdoor, athletic and workwear brands consolidate volumes and negotiate aggressively, driving FOB and payment-term concessions of up to 10% in 2024 for many suppliers.

Their scale and multi-season planning visibility lets buyers demand lower costs and steady allocations; vendor scorecards in 2024 typically link allocations to cost, quality and ESG, with ESG weighting growing industrywide.

Losing a key program can materially reduce facility utilization and revenue volatility for suppliers like Youngone.

Technical co-development raises switching costs

ODM collaboration on patterns, fit blocks and performance specs embeds proprietary know-how, creating knowledge lock-in. Tooling, molds and testing protocols often exceed $100,000 per style and retooling or qualification can add 4–12 weeks to lead times. Switching vendors therefore risks delays and quality drift for buyers. This reality softens price demands on complex, high‑spec products.

Lead-time and agility expectations intensify leverage

Brands demand rapid drops, continuous replenishment, and size-color flexibility, forcing vendors to hold greige inventory and enable fast changeovers to avoid losing allocations. Failure to hit agreed speed targets shifts orders to more agile suppliers, boosting customer bargaining power. Advanced planning and nearshoring can convert speed into bargaining parity for vendors.

ESG and traceability requirements shape terms

Buyers increasingly demand emissions data, recycled-content claims and labor-compliance proofs, and the EU CSRD rollout in 2024 raised buyer reporting expectations; failure to comply has led brands to cut suppliers and compress margins. Youngone’s investments in renewable energy and certified processes bolster its bid-win rate and enable value-based pricing on sustainable product lines.

- CSRD 2024: higher reporting standards

- SBTi >5,000 signatories (2024)

- Non‑compliance risks lost orders and margin pressure

- Renewables/certifications justify premium pricing

Multi-sourcing policies cap dependence

Most global apparel brands split styles across multiple factories and countries; by 2024 roughly 75% of top 100 brands used multi-sourcing to reduce single-vendor risk, improving their negotiating stance. Youngone counters by emphasizing reliability and product innovation to secure core allocations and negotiates longer framework agreements to stabilize volumes and margins.

- Multi-sourcing adoption ~75% (top 100 brands, 2024)

- Youngone leverages reliability + innovation to win core slots

- Longer frameworks reduce volume volatility and secure terms

Buyers squeeze margins with up to 10% FOB concessions; certified suppliers earn premium

Buyers exert strong leverage: 2024 FOB/payment concessions up to 10% and multi-sourcing by ~75% of top brands compress margins. ESG reporting (CSRD 2024) and SBTi adoption raise compliance costs but allow premium pricing for certified suppliers. Speed, allocation loss risk and ODM lock‑in create mixed bargaining dynamics favoring large brands on price but rewarding reliable, certified suppliers.

| Metric | 2024 Value |

|---|---|

| FOB/payment concessions | up to 10% |

| Top brands multi-sourcing | ~75% |

| SBTi signatories | >5,000 |

What You See Is What You Get

Youngone Porter's Five Forces Analysis

This preview shows the exact Youngone Porter's Five Forces Analysis you'll receive—no placeholders or mockups. The full document is professionally formatted, complete with supplier, buyer, rivalry, substitute, and entry threat assessments. Once purchased, you’ll get immediate access to this same ready-to-use file for download and use.

Go Beyond the Preview—Access the Full Strategic Report

Youngone Porter's Five Forces snapshot highlights supplier leverage, buyer power, substitution risks and competitive rivalry—revealing strategic pressure points and potential growth levers. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Youngone’s competitive dynamics in detail.

Suppliers Bargaining Power

Vertical integration dampens supplier leverage

Youngone’s in-house fabric mills, trim production and logistics cut reliance on external suppliers, lowering input-price vulnerability and securing supply continuity. This vertical integration enables backward planning and compresses design-to-production cycles, accelerating time-to-market. Internal capacity also strengthens negotiating leverage with remaining vendors, shifting bargaining power in Youngone’s favor.

Specialized materials suppliers remain influential

Specialized inputs like high-performance membranes, technical foams, and advanced chemicals are sourced from a limited group of certified suppliers, giving those vendors notable leverage over Youngone. Certification requirements, IP protections, and stringent specifications narrow alternatives, allowing premiums and extended lead times. Dual- and multi-sourcing mitigate risk but seldom fully neutralize supplier bargaining power.

Commodity price volatility transmits upstream power

Global polyester, nylon, cotton and energy prices remain cyclical — Brent crude surged to about $130/bbl in 2022 and averaged near $87/bbl in 2023, feeding feedstock swings that have caused raw-material cost moves often in the 20–40% range across 2021–24. Even with vertical integration, Youngone faces margin volatility and tougher quoting when inputs jump. Hedging programs and renewables cap exposure but cannot eliminate swings, and customer resistance to full pass-throughs intensifies margin squeeze.

Geographic concentration and logistics risk

Geographic concentration exposes Youngone to weather events, port congestion and geopolitical shocks that can sever key raw-material corridors; about 80% of global merchandise trade by volume moves by sea (UNCTAD). Limited nearby alternatives increase local supplier leverage, while multi-country sourcing diversifies risk but raises coordination and logistics costs; supplier development programs can gradually reduce regional bottlenecks.

- 80% global trade by volume via sea (UNCTAD)

- Local suppliers gain leverage when alternatives scarce

- Multi-country sourcing = higher coordination costs

- Supplier development reduces regional bottlenecks over time

Sustainability and compliance elevate supplier gatekeeping

Sustainability mandates—OEKO-TEX reporting over 12,000 certified companies and bluesign partnerships near 3,000 in 2024—shrink Youngone’s approved supplier pool, raising supplier gatekeeping and price leverage.

Mandatory traceability covering roughly 25% of apparel volume in 2024 and a ~40% rise in compliance audits (2020–24) increase switching frictions and data transparency demands.

Certified suppliers exploit certification scarcity for higher margins, while Youngone’s vertical investments in cleaner processes and CAPEX reallocations reclaim control.

- Certification density: OEKO-TEX ~12,000; bluesign ~3,000 (2024)

- Traceability coverage ~25% (2024)

- Compliance audits +40% (2020–24)

- Verticalization reduces supplier leverage via in-house clean processes

Verticalization trims supplier risk; certifications scarce, Brent at $87, traceability 25%

Youngone’s verticalization (in-house mills, trims, logistics) reduces supplier dependence and boosts leverage. Specialized inputs and certification scarcity (OEKO-TEX ~12,000; bluesign ~3,000 in 2024) keep supplier power elevated. Commodity swings (Brent ~$87 avg 2023) and 25% traceability coverage raise switching costs and margin volatility.

| Metric | Value |

|---|---|

| Sea trade share (UNCTAD) | 80% |

| Brent avg 2023 | $87/bbl |

| OEKO-TEX (2024) | ~12,000 |

| bluesign (2024) | ~3,000 |

| Traceability coverage (2024) | ~25% |

| Compliance audits (2020–24) | +40% |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, substitutes and entry barriers tailored exclusively for Youngone, identifying disruptive threats and strategic levers; fully editable for reports and decks.

One-sheet Porter's Five Forces for Youngone — instantly visualize supplier, buyer, competitor, entrant, and substitute pressure with a crisp spider chart for faster strategic decisions. Customize scores, swap in current data, and paste directly into pitch decks or board reports for immediate clarity.

Customers Bargaining Power

Concentrated global brand buyers wield price pressure

Large outdoor, athletic and workwear brands consolidate volumes and negotiate aggressively, driving FOB and payment-term concessions of up to 10% in 2024 for many suppliers.

Their scale and multi-season planning visibility lets buyers demand lower costs and steady allocations; vendor scorecards in 2024 typically link allocations to cost, quality and ESG, with ESG weighting growing industrywide.

Losing a key program can materially reduce facility utilization and revenue volatility for suppliers like Youngone.

Technical co-development raises switching costs

ODM collaboration on patterns, fit blocks and performance specs embeds proprietary know-how, creating knowledge lock-in. Tooling, molds and testing protocols often exceed $100,000 per style and retooling or qualification can add 4–12 weeks to lead times. Switching vendors therefore risks delays and quality drift for buyers. This reality softens price demands on complex, high‑spec products.

Lead-time and agility expectations intensify leverage

Brands demand rapid drops, continuous replenishment, and size-color flexibility, forcing vendors to hold greige inventory and enable fast changeovers to avoid losing allocations. Failure to hit agreed speed targets shifts orders to more agile suppliers, boosting customer bargaining power. Advanced planning and nearshoring can convert speed into bargaining parity for vendors.

ESG and traceability requirements shape terms

Buyers increasingly demand emissions data, recycled-content claims and labor-compliance proofs, and the EU CSRD rollout in 2024 raised buyer reporting expectations; failure to comply has led brands to cut suppliers and compress margins. Youngone’s investments in renewable energy and certified processes bolster its bid-win rate and enable value-based pricing on sustainable product lines.

- CSRD 2024: higher reporting standards

- SBTi >5,000 signatories (2024)

- Non‑compliance risks lost orders and margin pressure

- Renewables/certifications justify premium pricing

Multi-sourcing policies cap dependence

Most global apparel brands split styles across multiple factories and countries; by 2024 roughly 75% of top 100 brands used multi-sourcing to reduce single-vendor risk, improving their negotiating stance. Youngone counters by emphasizing reliability and product innovation to secure core allocations and negotiates longer framework agreements to stabilize volumes and margins.

- Multi-sourcing adoption ~75% (top 100 brands, 2024)

- Youngone leverages reliability + innovation to win core slots

- Longer frameworks reduce volume volatility and secure terms

Buyers squeeze margins with up to 10% FOB concessions; certified suppliers earn premium

Buyers exert strong leverage: 2024 FOB/payment concessions up to 10% and multi-sourcing by ~75% of top brands compress margins. ESG reporting (CSRD 2024) and SBTi adoption raise compliance costs but allow premium pricing for certified suppliers. Speed, allocation loss risk and ODM lock‑in create mixed bargaining dynamics favoring large brands on price but rewarding reliable, certified suppliers.

| Metric | 2024 Value |

|---|---|

| FOB/payment concessions | up to 10% |

| Top brands multi-sourcing | ~75% |

| SBTi signatories | >5,000 |

What You See Is What You Get

Youngone Porter's Five Forces Analysis

This preview shows the exact Youngone Porter's Five Forces Analysis you'll receive—no placeholders or mockups. The full document is professionally formatted, complete with supplier, buyer, rivalry, substitute, and entry threat assessments. Once purchased, you’ll get immediate access to this same ready-to-use file for download and use.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Youngone Porter's Five Forces snapshot highlights supplier leverage, buyer power, substitution risks and competitive rivalry—revealing strategic pressure points and potential growth levers. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Youngone’s competitive dynamics in detail.

Suppliers Bargaining Power

Vertical integration dampens supplier leverage

Youngone’s in-house fabric mills, trim production and logistics cut reliance on external suppliers, lowering input-price vulnerability and securing supply continuity. This vertical integration enables backward planning and compresses design-to-production cycles, accelerating time-to-market. Internal capacity also strengthens negotiating leverage with remaining vendors, shifting bargaining power in Youngone’s favor.

Specialized materials suppliers remain influential

Specialized inputs like high-performance membranes, technical foams, and advanced chemicals are sourced from a limited group of certified suppliers, giving those vendors notable leverage over Youngone. Certification requirements, IP protections, and stringent specifications narrow alternatives, allowing premiums and extended lead times. Dual- and multi-sourcing mitigate risk but seldom fully neutralize supplier bargaining power.

Commodity price volatility transmits upstream power

Global polyester, nylon, cotton and energy prices remain cyclical — Brent crude surged to about $130/bbl in 2022 and averaged near $87/bbl in 2023, feeding feedstock swings that have caused raw-material cost moves often in the 20–40% range across 2021–24. Even with vertical integration, Youngone faces margin volatility and tougher quoting when inputs jump. Hedging programs and renewables cap exposure but cannot eliminate swings, and customer resistance to full pass-throughs intensifies margin squeeze.

Geographic concentration and logistics risk

Geographic concentration exposes Youngone to weather events, port congestion and geopolitical shocks that can sever key raw-material corridors; about 80% of global merchandise trade by volume moves by sea (UNCTAD). Limited nearby alternatives increase local supplier leverage, while multi-country sourcing diversifies risk but raises coordination and logistics costs; supplier development programs can gradually reduce regional bottlenecks.

- 80% global trade by volume via sea (UNCTAD)

- Local suppliers gain leverage when alternatives scarce

- Multi-country sourcing = higher coordination costs

- Supplier development reduces regional bottlenecks over time

Sustainability and compliance elevate supplier gatekeeping

Sustainability mandates—OEKO-TEX reporting over 12,000 certified companies and bluesign partnerships near 3,000 in 2024—shrink Youngone’s approved supplier pool, raising supplier gatekeeping and price leverage.

Mandatory traceability covering roughly 25% of apparel volume in 2024 and a ~40% rise in compliance audits (2020–24) increase switching frictions and data transparency demands.

Certified suppliers exploit certification scarcity for higher margins, while Youngone’s vertical investments in cleaner processes and CAPEX reallocations reclaim control.

- Certification density: OEKO-TEX ~12,000; bluesign ~3,000 (2024)

- Traceability coverage ~25% (2024)

- Compliance audits +40% (2020–24)

- Verticalization reduces supplier leverage via in-house clean processes

Verticalization trims supplier risk; certifications scarce, Brent at $87, traceability 25%

Youngone’s verticalization (in-house mills, trims, logistics) reduces supplier dependence and boosts leverage. Specialized inputs and certification scarcity (OEKO-TEX ~12,000; bluesign ~3,000 in 2024) keep supplier power elevated. Commodity swings (Brent ~$87 avg 2023) and 25% traceability coverage raise switching costs and margin volatility.

| Metric | Value |

|---|---|

| Sea trade share (UNCTAD) | 80% |

| Brent avg 2023 | $87/bbl |

| OEKO-TEX (2024) | ~12,000 |

| bluesign (2024) | ~3,000 |

| Traceability coverage (2024) | ~25% |

| Compliance audits (2020–24) | +40% |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, substitutes and entry barriers tailored exclusively for Youngone, identifying disruptive threats and strategic levers; fully editable for reports and decks.

One-sheet Porter's Five Forces for Youngone — instantly visualize supplier, buyer, competitor, entrant, and substitute pressure with a crisp spider chart for faster strategic decisions. Customize scores, swap in current data, and paste directly into pitch decks or board reports for immediate clarity.

Customers Bargaining Power

Concentrated global brand buyers wield price pressure

Large outdoor, athletic and workwear brands consolidate volumes and negotiate aggressively, driving FOB and payment-term concessions of up to 10% in 2024 for many suppliers.

Their scale and multi-season planning visibility lets buyers demand lower costs and steady allocations; vendor scorecards in 2024 typically link allocations to cost, quality and ESG, with ESG weighting growing industrywide.

Losing a key program can materially reduce facility utilization and revenue volatility for suppliers like Youngone.

Technical co-development raises switching costs

ODM collaboration on patterns, fit blocks and performance specs embeds proprietary know-how, creating knowledge lock-in. Tooling, molds and testing protocols often exceed $100,000 per style and retooling or qualification can add 4–12 weeks to lead times. Switching vendors therefore risks delays and quality drift for buyers. This reality softens price demands on complex, high‑spec products.

Lead-time and agility expectations intensify leverage

Brands demand rapid drops, continuous replenishment, and size-color flexibility, forcing vendors to hold greige inventory and enable fast changeovers to avoid losing allocations. Failure to hit agreed speed targets shifts orders to more agile suppliers, boosting customer bargaining power. Advanced planning and nearshoring can convert speed into bargaining parity for vendors.

ESG and traceability requirements shape terms

Buyers increasingly demand emissions data, recycled-content claims and labor-compliance proofs, and the EU CSRD rollout in 2024 raised buyer reporting expectations; failure to comply has led brands to cut suppliers and compress margins. Youngone’s investments in renewable energy and certified processes bolster its bid-win rate and enable value-based pricing on sustainable product lines.

- CSRD 2024: higher reporting standards

- SBTi >5,000 signatories (2024)

- Non‑compliance risks lost orders and margin pressure

- Renewables/certifications justify premium pricing

Multi-sourcing policies cap dependence

Most global apparel brands split styles across multiple factories and countries; by 2024 roughly 75% of top 100 brands used multi-sourcing to reduce single-vendor risk, improving their negotiating stance. Youngone counters by emphasizing reliability and product innovation to secure core allocations and negotiates longer framework agreements to stabilize volumes and margins.

- Multi-sourcing adoption ~75% (top 100 brands, 2024)

- Youngone leverages reliability + innovation to win core slots

- Longer frameworks reduce volume volatility and secure terms

Buyers squeeze margins with up to 10% FOB concessions; certified suppliers earn premium

Buyers exert strong leverage: 2024 FOB/payment concessions up to 10% and multi-sourcing by ~75% of top brands compress margins. ESG reporting (CSRD 2024) and SBTi adoption raise compliance costs but allow premium pricing for certified suppliers. Speed, allocation loss risk and ODM lock‑in create mixed bargaining dynamics favoring large brands on price but rewarding reliable, certified suppliers.

| Metric | 2024 Value |

|---|---|

| FOB/payment concessions | up to 10% |

| Top brands multi-sourcing | ~75% |

| SBTi signatories | >5,000 |

What You See Is What You Get

Youngone Porter's Five Forces Analysis

This preview shows the exact Youngone Porter's Five Forces Analysis you'll receive—no placeholders or mockups. The full document is professionally formatted, complete with supplier, buyer, rivalry, substitute, and entry threat assessments. Once purchased, you’ll get immediate access to this same ready-to-use file for download and use.