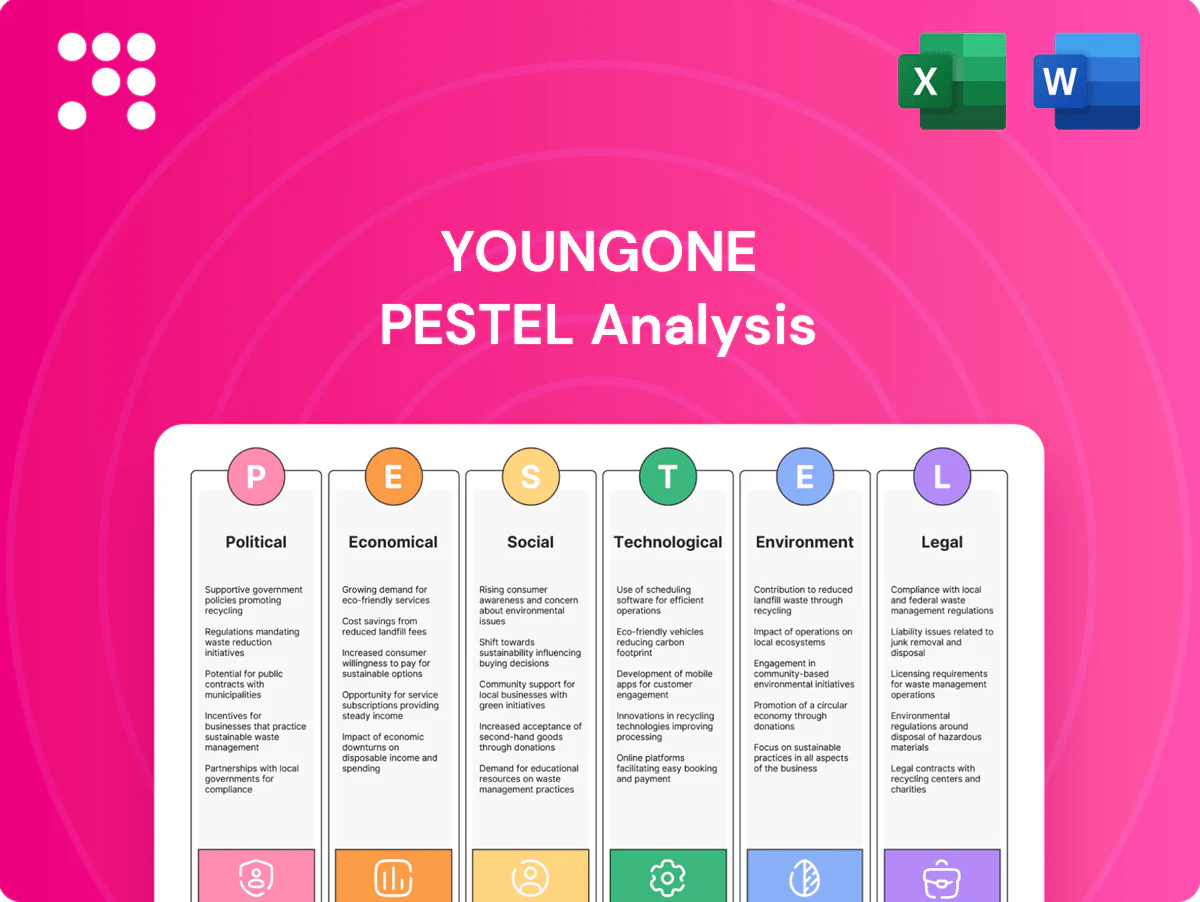

Youngone PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how political, economic, social, technological, legal and environmental forces are reshaping Youngone’s prospects with our focused PESTLE analysis—three actionable insights per factor help you spot risks and growth pockets. Ideal for investors and strategists, the full report is ready to download for immediate use—purchase now to get the complete, editable analysis.

Political factors

Trade policy volatility across sourcing hubs

Youngone’s multi-country footprint across Bangladesh, Vietnam, Myanmar and Ethiopia leaves it exposed to tariffs, quotas and rules-of-origin shifts that can swing landed costs by several percentage points; US/EU GSP changes historically move margins materially. Proactive diversification of production and HS-code optimization reduce shock exposure, while continuous monitoring of bilateral agreements and the WTO (over 1,000 trade actions since 2020) is essential.

Geopolitical tensions and supply chain security

Regional disputes and great-power competition can disrupt logistics lanes and input flows; 2023 Red Sea incidents forced reroutes adding roughly 10–14 days and raising freight costs an estimated 20–40% per industry reports, harming OTIF for brand clients. Building buffer stocks of critical materials and dual-sourcing reduces interruption risk, while scenario planning with logistics partners strengthens resilience and shortens recovery times.

Industrial and renewable energy incentives

Host governments commonly offer tax holidays of 3–10 years, SEZ corporate rates often reduced to 0–15%, and green-energy subsidies or feed-in tariff support in many markets; capturing these incentives can lower factory and solar capex by up to 20–30% (utility-scale solar capex ~US$600–900/kW in 2024). Compliance with incentive covenants necessitates robust reporting and audit trails, and long-term policy stability materially affects investment pacing and payback timing.

Labor policy and wage-setting frameworks

Minimum wage revisions and collective bargaining drive unit labor costs; ILO data shows global average wage growth was about 3.3% in 2023, increasing cost pressure for apparel suppliers like Youngone. Predictable escalation clauses (commonly 2–4% annually) can be priced into brand contracts, while engagement with tripartite bodies helps anticipate regulatory shifts. Ongoing productivity programs (automation, line balancing) offset wage inflation and protected margins.

- ILO: global wage growth ~3.3% (2023)

- Escalation clauses typically 2–4% pa

- Tripartite engagement reduces regulatory surprise

- Productivity gains key to margin protection

Customs compliance and traceability mandates

Stricter provenance checks, driven by U.S. UFLPA enforcement and EU due-diligence moves, increase documentation for Youngone across suppliers and materials.

End-to-end traceability from yarn to cut-make-trim is now critical to clear borders and meet retailer demands; audits often require batch-level records.

Digital chain-of-custody tools speed border clearances and reduce average detention risk, where non-compliance can cause 7–21 day shipment holds and severe reputational damage.

- Compliance: UFLPA presumption impacts Xinjiang-sourced inputs

- Traceability: batch-level records required

- Tools: digital custody lowers clearance friction

- Risk: 7–21 day detentions, brand harm

Tariff, origin and traceability shocks raise costs; delays 10–14 days, freight +20–40%

Youngone faces tariff/quota and rules-of-origin shocks across BD/VN/MM/Ethiopia that can swing landed costs several percentage points; WTO recorded >1,000 trade actions since 2020. Geopolitical disruptions (2023 Red Sea) added ~10–14 days and raised freight ~20–40%, harming OTIF. Incentives (tax holidays 3–10 yrs; SEZ rates 0–15%) and traceability rules (UFLPA, 7–21 day detentions) materially shape capex, margins and compliance.

| Factor | Metric | 2023–24 data |

|---|---|---|

| Trade actions | WTO cases | >1,000 since 2020 |

What is included in the product

Provides a concise PESTLE evaluation of Youngone across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives and investors, it highlights risks, opportunities and forward-looking insights ready for reports or decks.

Relieves research overload by providing a concise, visually segmented PESTLE summary of Youngone that highlights external risks and opportunities for quick reference in meetings or presentations, and is easily shareable and editable for regional or business-line notes.

Economic factors

Global demand cycles in outdoor and athleisure

Global demand cycles in outdoor and athleisure drive sharp consumer discretionary swings that create order volatility for Youngone, with brand reorder variability reported as high as ±15% quarter-on-quarter in recent seasons.

Retail inventory corrections in 2023–24 compressed factory utilization by roughly 10–20%, pressuring margins and throughput on fixed lines.

Flexible capacity and modular lines have stabilized output, while VMI and forecast-sharing programs—shown to cut stockouts and improve fill rates materially—provide critical forward visibility for planning.

Input cost fluctuations (cotton, synthetics, energy)

Raw material price swings directly alter Youngone’s COGS: cotton futures averaged roughly $0.85/lb in 2024 while polyester feedstock volatility pushed synthetic costs up to double-digit percent swings year-on-year. Hedging, multi-fiber blends and long-term supplier contracts have been used to smooth margins and reduce spot exposure. On-site energy self-generation (solar/waste-heat) has lowered grid dependency, cutting peak price exposure materially. Ability to pass costs to buyers varies by client contract terms and purchase order flexibility.

FX volatility across operating currencies

Revenue largely invoiced in USD/EUR while production and payroll are paid in local currencies, exposing margins to FX swings; EUR/USD averaged about 1.07 in 2024 and US policy rates remained at 5.25–5.50% by mid‑2025, sustaining volatility. Natural hedges and derivatives (forwards/swaps) are used to protect margins, pricing ladders with clients align invoices to currency moves, and centralized treasury enables netting and tighter liquidity control.

Scale economies and vertical integration

Youngone’s in-house materials and finishing shorten lead times and cut transaction costs—industry evidence suggests integrated suppliers can reduce lead times by about 20–30%, helping Youngone lift asset turns and improve ROIC by roughly 2–4 percentage points since 2021. Verticality enables premium technical offerings with ASPs typically 20–30% above basic lines, but heavy capital intensity demands disciplined capex; Youngone’s 2024 capex was about USD 30m.

- In-house finishing: ~20–30% shorter lead times

- ROIC lift: +2–4 pp since 2021

- Premium ASPs: +20–30%

- 2024 capex: ~USD 30m

Client concentration and credit risk

Youngone’s OEM/ODM model concentrates revenue with a few large global brands, raising client concentration and credit risk for receivables.

Diversification into varied end-markets and expansion of owned retail channels has reduced reliance on major buyers while co-development partnerships increase customer stickiness.

Credit insurance and strict AR controls are used to mitigate counterparty default risk and shorten DSO.

- Concentration exposure: reliance on large global brands

- Diversification: end-markets and owned retail reduce dependency

- Risk controls: credit insurance and tight AR policies

- Stickiness: co-development partnerships

Tariff, origin and traceability shocks raise costs; delays 10–14 days, freight +20–40%

Global athleisure demand swings drive order volatility (brand reorders ±15% q/q), causing 2023–24 factory utilization drop ~10–20% and margin pressure.

Raw-materials: cotton ~$0.85/lb (2024); polyester feedstock saw double-digit YoY swings; hedging and blends used to smooth COGS.

FX and rates: EUR/USD ~1.07 (2024), US policy rate 5.25–5.50% (mid‑2025); treasury hedges and netting used to protect margins.

Verticalization raised ASPs +20–30% and ROIC +2–4 pp since 2021; 2024 capex ≈ USD 30m.

| Metric | Value |

|---|---|

| Reorder volatility | ±15% q/q |

| Factory utilization hit | −10–20% |

| Cotton (2024) | $0.85/lb |

| EUR/USD (2024) | 1.07 |

| US rate (mid‑2025) | 5.25–5.50% |

| Premium ASP uplift | +20–30% |

| ROIC gain since 2021 | +2–4 pp |

| 2024 capex | ~USD 30m |

Preview the Actual Deliverable

Youngone PESTLE Analysis

The Youngone PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file, with no placeholders or edits needed. After checkout you’ll get this finished, professionally structured report instantly.

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how political, economic, social, technological, legal and environmental forces are reshaping Youngone’s prospects with our focused PESTLE analysis—three actionable insights per factor help you spot risks and growth pockets. Ideal for investors and strategists, the full report is ready to download for immediate use—purchase now to get the complete, editable analysis.

Political factors

Trade policy volatility across sourcing hubs

Youngone’s multi-country footprint across Bangladesh, Vietnam, Myanmar and Ethiopia leaves it exposed to tariffs, quotas and rules-of-origin shifts that can swing landed costs by several percentage points; US/EU GSP changes historically move margins materially. Proactive diversification of production and HS-code optimization reduce shock exposure, while continuous monitoring of bilateral agreements and the WTO (over 1,000 trade actions since 2020) is essential.

Geopolitical tensions and supply chain security

Regional disputes and great-power competition can disrupt logistics lanes and input flows; 2023 Red Sea incidents forced reroutes adding roughly 10–14 days and raising freight costs an estimated 20–40% per industry reports, harming OTIF for brand clients. Building buffer stocks of critical materials and dual-sourcing reduces interruption risk, while scenario planning with logistics partners strengthens resilience and shortens recovery times.

Industrial and renewable energy incentives

Host governments commonly offer tax holidays of 3–10 years, SEZ corporate rates often reduced to 0–15%, and green-energy subsidies or feed-in tariff support in many markets; capturing these incentives can lower factory and solar capex by up to 20–30% (utility-scale solar capex ~US$600–900/kW in 2024). Compliance with incentive covenants necessitates robust reporting and audit trails, and long-term policy stability materially affects investment pacing and payback timing.

Labor policy and wage-setting frameworks

Minimum wage revisions and collective bargaining drive unit labor costs; ILO data shows global average wage growth was about 3.3% in 2023, increasing cost pressure for apparel suppliers like Youngone. Predictable escalation clauses (commonly 2–4% annually) can be priced into brand contracts, while engagement with tripartite bodies helps anticipate regulatory shifts. Ongoing productivity programs (automation, line balancing) offset wage inflation and protected margins.

- ILO: global wage growth ~3.3% (2023)

- Escalation clauses typically 2–4% pa

- Tripartite engagement reduces regulatory surprise

- Productivity gains key to margin protection

Customs compliance and traceability mandates

Stricter provenance checks, driven by U.S. UFLPA enforcement and EU due-diligence moves, increase documentation for Youngone across suppliers and materials.

End-to-end traceability from yarn to cut-make-trim is now critical to clear borders and meet retailer demands; audits often require batch-level records.

Digital chain-of-custody tools speed border clearances and reduce average detention risk, where non-compliance can cause 7–21 day shipment holds and severe reputational damage.

- Compliance: UFLPA presumption impacts Xinjiang-sourced inputs

- Traceability: batch-level records required

- Tools: digital custody lowers clearance friction

- Risk: 7–21 day detentions, brand harm

Tariff, origin and traceability shocks raise costs; delays 10–14 days, freight +20–40%

Youngone faces tariff/quota and rules-of-origin shocks across BD/VN/MM/Ethiopia that can swing landed costs several percentage points; WTO recorded >1,000 trade actions since 2020. Geopolitical disruptions (2023 Red Sea) added ~10–14 days and raised freight ~20–40%, harming OTIF. Incentives (tax holidays 3–10 yrs; SEZ rates 0–15%) and traceability rules (UFLPA, 7–21 day detentions) materially shape capex, margins and compliance.

| Factor | Metric | 2023–24 data |

|---|---|---|

| Trade actions | WTO cases | >1,000 since 2020 |

What is included in the product

Provides a concise PESTLE evaluation of Youngone across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives and investors, it highlights risks, opportunities and forward-looking insights ready for reports or decks.

Relieves research overload by providing a concise, visually segmented PESTLE summary of Youngone that highlights external risks and opportunities for quick reference in meetings or presentations, and is easily shareable and editable for regional or business-line notes.

Economic factors

Global demand cycles in outdoor and athleisure

Global demand cycles in outdoor and athleisure drive sharp consumer discretionary swings that create order volatility for Youngone, with brand reorder variability reported as high as ±15% quarter-on-quarter in recent seasons.

Retail inventory corrections in 2023–24 compressed factory utilization by roughly 10–20%, pressuring margins and throughput on fixed lines.

Flexible capacity and modular lines have stabilized output, while VMI and forecast-sharing programs—shown to cut stockouts and improve fill rates materially—provide critical forward visibility for planning.

Input cost fluctuations (cotton, synthetics, energy)

Raw material price swings directly alter Youngone’s COGS: cotton futures averaged roughly $0.85/lb in 2024 while polyester feedstock volatility pushed synthetic costs up to double-digit percent swings year-on-year. Hedging, multi-fiber blends and long-term supplier contracts have been used to smooth margins and reduce spot exposure. On-site energy self-generation (solar/waste-heat) has lowered grid dependency, cutting peak price exposure materially. Ability to pass costs to buyers varies by client contract terms and purchase order flexibility.

FX volatility across operating currencies

Revenue largely invoiced in USD/EUR while production and payroll are paid in local currencies, exposing margins to FX swings; EUR/USD averaged about 1.07 in 2024 and US policy rates remained at 5.25–5.50% by mid‑2025, sustaining volatility. Natural hedges and derivatives (forwards/swaps) are used to protect margins, pricing ladders with clients align invoices to currency moves, and centralized treasury enables netting and tighter liquidity control.

Scale economies and vertical integration

Youngone’s in-house materials and finishing shorten lead times and cut transaction costs—industry evidence suggests integrated suppliers can reduce lead times by about 20–30%, helping Youngone lift asset turns and improve ROIC by roughly 2–4 percentage points since 2021. Verticality enables premium technical offerings with ASPs typically 20–30% above basic lines, but heavy capital intensity demands disciplined capex; Youngone’s 2024 capex was about USD 30m.

- In-house finishing: ~20–30% shorter lead times

- ROIC lift: +2–4 pp since 2021

- Premium ASPs: +20–30%

- 2024 capex: ~USD 30m

Client concentration and credit risk

Youngone’s OEM/ODM model concentrates revenue with a few large global brands, raising client concentration and credit risk for receivables.

Diversification into varied end-markets and expansion of owned retail channels has reduced reliance on major buyers while co-development partnerships increase customer stickiness.

Credit insurance and strict AR controls are used to mitigate counterparty default risk and shorten DSO.

- Concentration exposure: reliance on large global brands

- Diversification: end-markets and owned retail reduce dependency

- Risk controls: credit insurance and tight AR policies

- Stickiness: co-development partnerships

Tariff, origin and traceability shocks raise costs; delays 10–14 days, freight +20–40%

Global athleisure demand swings drive order volatility (brand reorders ±15% q/q), causing 2023–24 factory utilization drop ~10–20% and margin pressure.

Raw-materials: cotton ~$0.85/lb (2024); polyester feedstock saw double-digit YoY swings; hedging and blends used to smooth COGS.

FX and rates: EUR/USD ~1.07 (2024), US policy rate 5.25–5.50% (mid‑2025); treasury hedges and netting used to protect margins.

Verticalization raised ASPs +20–30% and ROIC +2–4 pp since 2021; 2024 capex ≈ USD 30m.

| Metric | Value |

|---|---|

| Reorder volatility | ±15% q/q |

| Factory utilization hit | −10–20% |

| Cotton (2024) | $0.85/lb |

| EUR/USD (2024) | 1.07 |

| US rate (mid‑2025) | 5.25–5.50% |

| Premium ASP uplift | +20–30% |

| ROIC gain since 2021 | +2–4 pp |

| 2024 capex | ~USD 30m |

Preview the Actual Deliverable

Youngone PESTLE Analysis

The Youngone PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file, with no placeholders or edits needed. After checkout you’ll get this finished, professionally structured report instantly.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how political, economic, social, technological, legal and environmental forces are reshaping Youngone’s prospects with our focused PESTLE analysis—three actionable insights per factor help you spot risks and growth pockets. Ideal for investors and strategists, the full report is ready to download for immediate use—purchase now to get the complete, editable analysis.

Political factors

Trade policy volatility across sourcing hubs

Youngone’s multi-country footprint across Bangladesh, Vietnam, Myanmar and Ethiopia leaves it exposed to tariffs, quotas and rules-of-origin shifts that can swing landed costs by several percentage points; US/EU GSP changes historically move margins materially. Proactive diversification of production and HS-code optimization reduce shock exposure, while continuous monitoring of bilateral agreements and the WTO (over 1,000 trade actions since 2020) is essential.

Geopolitical tensions and supply chain security

Regional disputes and great-power competition can disrupt logistics lanes and input flows; 2023 Red Sea incidents forced reroutes adding roughly 10–14 days and raising freight costs an estimated 20–40% per industry reports, harming OTIF for brand clients. Building buffer stocks of critical materials and dual-sourcing reduces interruption risk, while scenario planning with logistics partners strengthens resilience and shortens recovery times.

Industrial and renewable energy incentives

Host governments commonly offer tax holidays of 3–10 years, SEZ corporate rates often reduced to 0–15%, and green-energy subsidies or feed-in tariff support in many markets; capturing these incentives can lower factory and solar capex by up to 20–30% (utility-scale solar capex ~US$600–900/kW in 2024). Compliance with incentive covenants necessitates robust reporting and audit trails, and long-term policy stability materially affects investment pacing and payback timing.

Labor policy and wage-setting frameworks

Minimum wage revisions and collective bargaining drive unit labor costs; ILO data shows global average wage growth was about 3.3% in 2023, increasing cost pressure for apparel suppliers like Youngone. Predictable escalation clauses (commonly 2–4% annually) can be priced into brand contracts, while engagement with tripartite bodies helps anticipate regulatory shifts. Ongoing productivity programs (automation, line balancing) offset wage inflation and protected margins.

- ILO: global wage growth ~3.3% (2023)

- Escalation clauses typically 2–4% pa

- Tripartite engagement reduces regulatory surprise

- Productivity gains key to margin protection

Customs compliance and traceability mandates

Stricter provenance checks, driven by U.S. UFLPA enforcement and EU due-diligence moves, increase documentation for Youngone across suppliers and materials.

End-to-end traceability from yarn to cut-make-trim is now critical to clear borders and meet retailer demands; audits often require batch-level records.

Digital chain-of-custody tools speed border clearances and reduce average detention risk, where non-compliance can cause 7–21 day shipment holds and severe reputational damage.

- Compliance: UFLPA presumption impacts Xinjiang-sourced inputs

- Traceability: batch-level records required

- Tools: digital custody lowers clearance friction

- Risk: 7–21 day detentions, brand harm

Tariff, origin and traceability shocks raise costs; delays 10–14 days, freight +20–40%

Youngone faces tariff/quota and rules-of-origin shocks across BD/VN/MM/Ethiopia that can swing landed costs several percentage points; WTO recorded >1,000 trade actions since 2020. Geopolitical disruptions (2023 Red Sea) added ~10–14 days and raised freight ~20–40%, harming OTIF. Incentives (tax holidays 3–10 yrs; SEZ rates 0–15%) and traceability rules (UFLPA, 7–21 day detentions) materially shape capex, margins and compliance.

| Factor | Metric | 2023–24 data |

|---|---|---|

| Trade actions | WTO cases | >1,000 since 2020 |

What is included in the product

Provides a concise PESTLE evaluation of Youngone across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives and investors, it highlights risks, opportunities and forward-looking insights ready for reports or decks.

Relieves research overload by providing a concise, visually segmented PESTLE summary of Youngone that highlights external risks and opportunities for quick reference in meetings or presentations, and is easily shareable and editable for regional or business-line notes.

Economic factors

Global demand cycles in outdoor and athleisure

Global demand cycles in outdoor and athleisure drive sharp consumer discretionary swings that create order volatility for Youngone, with brand reorder variability reported as high as ±15% quarter-on-quarter in recent seasons.

Retail inventory corrections in 2023–24 compressed factory utilization by roughly 10–20%, pressuring margins and throughput on fixed lines.

Flexible capacity and modular lines have stabilized output, while VMI and forecast-sharing programs—shown to cut stockouts and improve fill rates materially—provide critical forward visibility for planning.

Input cost fluctuations (cotton, synthetics, energy)

Raw material price swings directly alter Youngone’s COGS: cotton futures averaged roughly $0.85/lb in 2024 while polyester feedstock volatility pushed synthetic costs up to double-digit percent swings year-on-year. Hedging, multi-fiber blends and long-term supplier contracts have been used to smooth margins and reduce spot exposure. On-site energy self-generation (solar/waste-heat) has lowered grid dependency, cutting peak price exposure materially. Ability to pass costs to buyers varies by client contract terms and purchase order flexibility.

FX volatility across operating currencies

Revenue largely invoiced in USD/EUR while production and payroll are paid in local currencies, exposing margins to FX swings; EUR/USD averaged about 1.07 in 2024 and US policy rates remained at 5.25–5.50% by mid‑2025, sustaining volatility. Natural hedges and derivatives (forwards/swaps) are used to protect margins, pricing ladders with clients align invoices to currency moves, and centralized treasury enables netting and tighter liquidity control.

Scale economies and vertical integration

Youngone’s in-house materials and finishing shorten lead times and cut transaction costs—industry evidence suggests integrated suppliers can reduce lead times by about 20–30%, helping Youngone lift asset turns and improve ROIC by roughly 2–4 percentage points since 2021. Verticality enables premium technical offerings with ASPs typically 20–30% above basic lines, but heavy capital intensity demands disciplined capex; Youngone’s 2024 capex was about USD 30m.

- In-house finishing: ~20–30% shorter lead times

- ROIC lift: +2–4 pp since 2021

- Premium ASPs: +20–30%

- 2024 capex: ~USD 30m

Client concentration and credit risk

Youngone’s OEM/ODM model concentrates revenue with a few large global brands, raising client concentration and credit risk for receivables.

Diversification into varied end-markets and expansion of owned retail channels has reduced reliance on major buyers while co-development partnerships increase customer stickiness.

Credit insurance and strict AR controls are used to mitigate counterparty default risk and shorten DSO.

- Concentration exposure: reliance on large global brands

- Diversification: end-markets and owned retail reduce dependency

- Risk controls: credit insurance and tight AR policies

- Stickiness: co-development partnerships

Tariff, origin and traceability shocks raise costs; delays 10–14 days, freight +20–40%

Global athleisure demand swings drive order volatility (brand reorders ±15% q/q), causing 2023–24 factory utilization drop ~10–20% and margin pressure.

Raw-materials: cotton ~$0.85/lb (2024); polyester feedstock saw double-digit YoY swings; hedging and blends used to smooth COGS.

FX and rates: EUR/USD ~1.07 (2024), US policy rate 5.25–5.50% (mid‑2025); treasury hedges and netting used to protect margins.

Verticalization raised ASPs +20–30% and ROIC +2–4 pp since 2021; 2024 capex ≈ USD 30m.

| Metric | Value |

|---|---|

| Reorder volatility | ±15% q/q |

| Factory utilization hit | −10–20% |

| Cotton (2024) | $0.85/lb |

| EUR/USD (2024) | 1.07 |

| US rate (mid‑2025) | 5.25–5.50% |

| Premium ASP uplift | +20–30% |

| ROIC gain since 2021 | +2–4 pp |

| 2024 capex | ~USD 30m |

Preview the Actual Deliverable

Youngone PESTLE Analysis

The Youngone PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file, with no placeholders or edits needed. After checkout you’ll get this finished, professionally structured report instantly.