Yellow Pages Group Ltd. Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

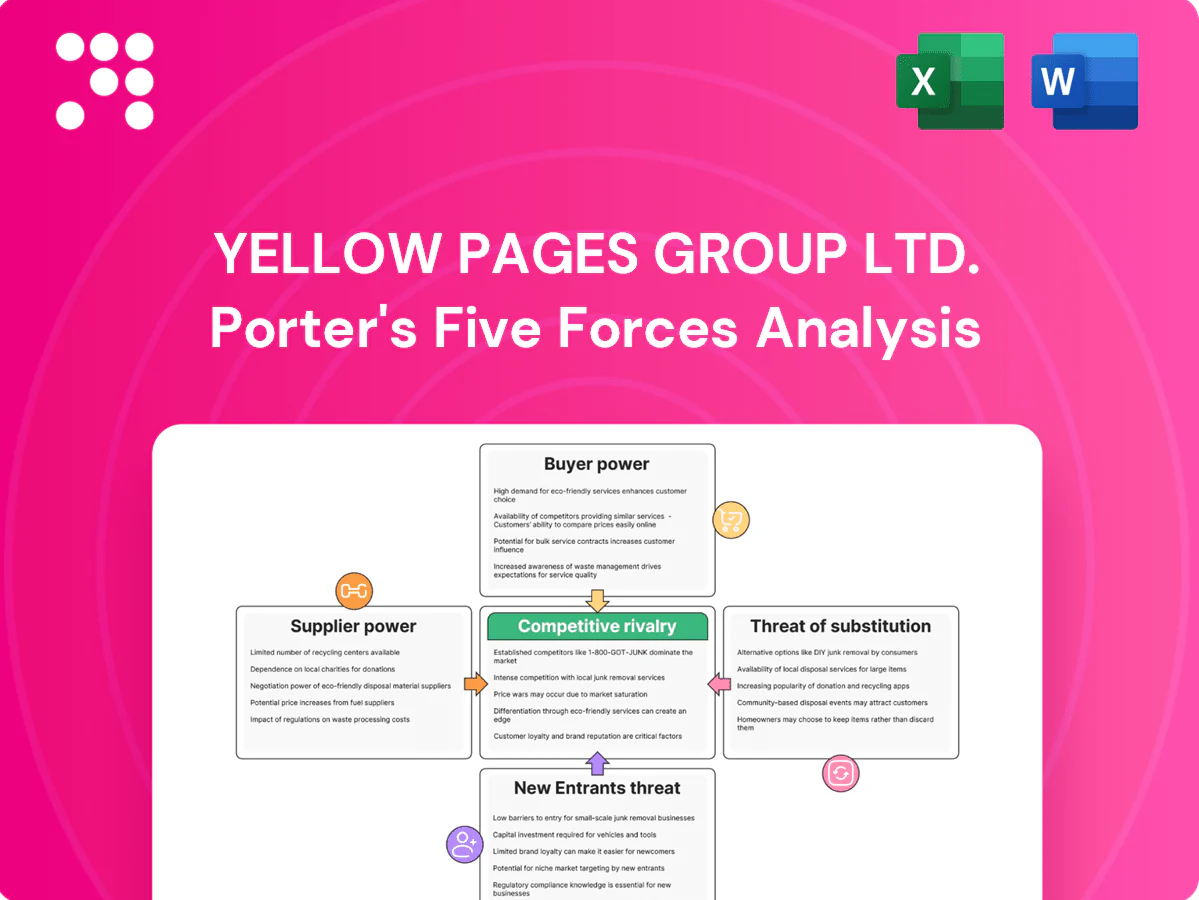

Yellow Pages Group Ltd. faces moderate buyer power, intense digital competition from search platforms and local directories, and rising substitute threats as users shift to mobile and social search. Supplier influence is limited, while regulatory and technological shifts affect entry barriers and strategic options.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Yellow Pages Group Ltd.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on major ad-tech platforms

Google (Alphabet) and Meta—with 2023 ad revenues of about 224.5bn and 134.9bn USD respectively—and Microsoft’s search/LinkedIn ads dominate the ecosystems YPG depends on, so algorithm or policy shifts can quickly change campaign performance and CPCs. This concentration gives platforms outsized pricing and data leverage, forcing YPG to diversify channels and pursue formal partner status to mitigate risk.

Software, hosting, and data tool vendors

YPG’s website builds, analytics, SEO and automation rely heavily on third‑party SaaS, hosting and data providers, and while switching is feasible it incurs migration, retraining and service risk; vendor lock‑in via proprietary features raises effective switching costs. In 2024 over 90% of enterprises used cloud services and roughly 60% adopted multi‑cloud strategies, which can restore bargaining balance.

Creative and technical talent supply

Designers, developers, SEO specialists and content creators are critical inputs for Yellow Pages Group, and New Zealand’s small population of about 5.1 million in 2024 contributes to a tight digital talent market that strengthens supplier bargaining power. Remote hiring broadens the candidate pool but raises coordination and quality-control risks, often increasing reliance on agencies and freelancers. Investing in a strong employer brand and training pipelines can lower dependency on external talent and contain wage pressure.

Telecom and infrastructure dependencies

As of 2024 Yellow Pages Group depends on reliable CDN/cloud and telecom infrastructure for digital listings; outages or supplier price hikes can breach SLAs and compress margins, while redundancy via multi-cloud and CDNs reduces dependency but increases cost; contracted SLAs and multi-cloud architectures temper supplier bargaining power.

- CDN/cloud uptime critical — outages = SLA risk

- Supplier price hikes directly impact margins

- Redundancy lowers risk but raises OPEX

- Contracted SLAs and multi-cloud moderate supplier power

Publishing partners and directory data sources

Publishing partners, local listing networks, map providers and data aggregators (Google Maps 1B+ monthly users in 2024) materially influence Yellow Pages Group Ltd distribution reach; exclusive or premium placement agreements can impose high fees and restrictive data-usage terms, and the limited number of high-quality New Zealand data sources increases supplier leverage. Building proprietary data quality and first-party relationships reduces reliance and bargaining exposure.

- Local listing networks: concentration increases supplier power

- Map providers: Google Maps >1B users (2024)

- Data scarcity in NZ: fewer high-quality sources

- Mitigation: invest in proprietary first-party data

Ad platform dominance and maps (>1bn) squeeze CPCs; cloud lock-in and NZ talent raise OPEX

Google/Meta dominance (Google ad rev $224.5bn, Meta $134.9bn in 2023) and Google Maps >1bn monthly users (2024) give platforms outsized pricing/data leverage, risking CPCs and reach. SaaS/cloud vendor lock‑in and NZ talent tightness (pop ~5.1m) raise switching costs. Multi‑cloud, SLAs and first‑party data cut exposure but increase OPEX.

| Supplier | Metric | Impact | Mitigation |

|---|---|---|---|

| Ad platforms | Google $224.5bn (2023) | Pricing/data leverage | Diversify partners |

| Cloud/CDN | 90% cloud use (2024) | Uptime/cost risk | Multi‑cloud, SLAs |

| Talent | NZ pop 5.1m (2024) | Wage/scarcity | Training, remote hire |

| Maps/data | Maps >1bn users (2024) | Distribution control | Build first‑party data |

What is included in the product

Tailored Porter's Five Forces analysis for Yellow Pages Group Ltd. uncovering competitive intensity, buyer and supplier leverage, digital substitutes and disruptive threats, entry barriers protecting incumbency, and strategic implications for pricing and profitability.

A concise one-sheet Porter's Five Forces for Yellow Pages Group—clearly maps competitive pressures (digital entrants, advertisers, substitutes, supplier/buyer power) to speed strategic decisions and prioritize remedies in pitch decks or boardroom slides.

Customers Bargaining Power

Fragmented but price-sensitive SME base

Most YPG customers are SMEs—SMEs make up 99.8% of Canadian businesses (Statistics Canada 2024)—so budgets are tight and ROI-focused. Easy agency comparison and tendency to churn if outcomes lag increases price pressure. Short contract terms amplify customer leverage. Clear performance reporting and tiered packages can stabilize retention.

Enterprise and government procurement muscle

Enterprise and government clients run formal RFPs, demand bespoke integrations and steep discounts that can make high-volume wins margin-dilutive; compliance and elevated security mandates raise delivery costs and require account-based management to protect unit economics.

Low switching costs among digital agencies

Websites, SEO and ads transfer with limited friction given CMS dominance (WordPress ~43% of sites in 2024) and Google’s ~92% search share, while standardized tools (Google Ads, Analytics, Shopify) streamline replacement; formal onboarding/offboarding processes support frequent agency rotation, though proprietary integrations and data lead-generation hooks can materially increase client stickiness.

High transparency of performance

Real-time metrics and public reviews make underperformance visible, and industry studies in 2024 show 70–90% of buyers consult online reviews, enabling quick identification of weak listings. Buyers benchmark results across providers, amplifying pressure on Yellow Pages Group to maintain competitive pricing and higher service levels. Outcome-linked pricing models, already adopted by some digital marketplaces, can align incentives and reduce disputes.

- Bargaining leverage: higher due to visible performance

- Benchmarking: cross-provider comparisons drive price competition

- Mitigation: outcome-linked pricing aligns incentives, lowers dispute risk

Bundling and cross-sell expectations

Clients increasingly demand bundled listings, web, SEO and paid media at discounted rates, shifting bargaining power to buyers seeking one-stop value; without clear differentiation these bundles compress margins for Yellow Pages Group Ltd. Packaging with proprietary data assets, advanced analytics and dedicated account support allows YPG to justify premiums and retain higher ARPU.

- Buyer leverage rises with bundle expectations

- Undifferentiated bundles lower margins

- Unique data/support enable premium pricing

SME buyers ROI-driven, price-sensitive; reviews sway 70-90%, raising churn risk

YPG customers (SMEs = 99.8% of Canadian firms, Statistics Canada 2024) are ROI-driven, price-sensitive and prone to churn; visible metrics and reviews (70–90% buyers consult reviews in 2024) increase bargaining power. Enterprise RFPs demand discounts and raise delivery costs; CMS/search concentration (WordPress ~43%, Google ~92% search share, 2024) eases switching.

| Metric | 2024 Value |

|---|---|

| SME share Canada | 99.8% |

| Google search share | ~92% |

| WordPress market | ~43% |

| Buyers using reviews | 70–90% |

Preview the Actual Deliverable

Yellow Pages Group Ltd. Porter's Five Forces Analysis

This preview shows the exact Yellow Pages Group Ltd. Porter's Five Forces Analysis you'll receive after purchase—no placeholders or samples. The full analysis is fully formatted, comprehensive and ready for immediate download and use. You're looking at the actual deliverable, complete and final.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Yellow Pages Group Ltd. faces moderate buyer power, intense digital competition from search platforms and local directories, and rising substitute threats as users shift to mobile and social search. Supplier influence is limited, while regulatory and technological shifts affect entry barriers and strategic options.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Yellow Pages Group Ltd.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on major ad-tech platforms

Google (Alphabet) and Meta—with 2023 ad revenues of about 224.5bn and 134.9bn USD respectively—and Microsoft’s search/LinkedIn ads dominate the ecosystems YPG depends on, so algorithm or policy shifts can quickly change campaign performance and CPCs. This concentration gives platforms outsized pricing and data leverage, forcing YPG to diversify channels and pursue formal partner status to mitigate risk.

Software, hosting, and data tool vendors

YPG’s website builds, analytics, SEO and automation rely heavily on third‑party SaaS, hosting and data providers, and while switching is feasible it incurs migration, retraining and service risk; vendor lock‑in via proprietary features raises effective switching costs. In 2024 over 90% of enterprises used cloud services and roughly 60% adopted multi‑cloud strategies, which can restore bargaining balance.

Creative and technical talent supply

Designers, developers, SEO specialists and content creators are critical inputs for Yellow Pages Group, and New Zealand’s small population of about 5.1 million in 2024 contributes to a tight digital talent market that strengthens supplier bargaining power. Remote hiring broadens the candidate pool but raises coordination and quality-control risks, often increasing reliance on agencies and freelancers. Investing in a strong employer brand and training pipelines can lower dependency on external talent and contain wage pressure.

Telecom and infrastructure dependencies

As of 2024 Yellow Pages Group depends on reliable CDN/cloud and telecom infrastructure for digital listings; outages or supplier price hikes can breach SLAs and compress margins, while redundancy via multi-cloud and CDNs reduces dependency but increases cost; contracted SLAs and multi-cloud architectures temper supplier bargaining power.

- CDN/cloud uptime critical — outages = SLA risk

- Supplier price hikes directly impact margins

- Redundancy lowers risk but raises OPEX

- Contracted SLAs and multi-cloud moderate supplier power

Publishing partners and directory data sources

Publishing partners, local listing networks, map providers and data aggregators (Google Maps 1B+ monthly users in 2024) materially influence Yellow Pages Group Ltd distribution reach; exclusive or premium placement agreements can impose high fees and restrictive data-usage terms, and the limited number of high-quality New Zealand data sources increases supplier leverage. Building proprietary data quality and first-party relationships reduces reliance and bargaining exposure.

- Local listing networks: concentration increases supplier power

- Map providers: Google Maps >1B users (2024)

- Data scarcity in NZ: fewer high-quality sources

- Mitigation: invest in proprietary first-party data

Ad platform dominance and maps (>1bn) squeeze CPCs; cloud lock-in and NZ talent raise OPEX

Google/Meta dominance (Google ad rev $224.5bn, Meta $134.9bn in 2023) and Google Maps >1bn monthly users (2024) give platforms outsized pricing/data leverage, risking CPCs and reach. SaaS/cloud vendor lock‑in and NZ talent tightness (pop ~5.1m) raise switching costs. Multi‑cloud, SLAs and first‑party data cut exposure but increase OPEX.

| Supplier | Metric | Impact | Mitigation |

|---|---|---|---|

| Ad platforms | Google $224.5bn (2023) | Pricing/data leverage | Diversify partners |

| Cloud/CDN | 90% cloud use (2024) | Uptime/cost risk | Multi‑cloud, SLAs |

| Talent | NZ pop 5.1m (2024) | Wage/scarcity | Training, remote hire |

| Maps/data | Maps >1bn users (2024) | Distribution control | Build first‑party data |

What is included in the product

Tailored Porter's Five Forces analysis for Yellow Pages Group Ltd. uncovering competitive intensity, buyer and supplier leverage, digital substitutes and disruptive threats, entry barriers protecting incumbency, and strategic implications for pricing and profitability.

A concise one-sheet Porter's Five Forces for Yellow Pages Group—clearly maps competitive pressures (digital entrants, advertisers, substitutes, supplier/buyer power) to speed strategic decisions and prioritize remedies in pitch decks or boardroom slides.

Customers Bargaining Power

Fragmented but price-sensitive SME base

Most YPG customers are SMEs—SMEs make up 99.8% of Canadian businesses (Statistics Canada 2024)—so budgets are tight and ROI-focused. Easy agency comparison and tendency to churn if outcomes lag increases price pressure. Short contract terms amplify customer leverage. Clear performance reporting and tiered packages can stabilize retention.

Enterprise and government procurement muscle

Enterprise and government clients run formal RFPs, demand bespoke integrations and steep discounts that can make high-volume wins margin-dilutive; compliance and elevated security mandates raise delivery costs and require account-based management to protect unit economics.

Low switching costs among digital agencies

Websites, SEO and ads transfer with limited friction given CMS dominance (WordPress ~43% of sites in 2024) and Google’s ~92% search share, while standardized tools (Google Ads, Analytics, Shopify) streamline replacement; formal onboarding/offboarding processes support frequent agency rotation, though proprietary integrations and data lead-generation hooks can materially increase client stickiness.

High transparency of performance

Real-time metrics and public reviews make underperformance visible, and industry studies in 2024 show 70–90% of buyers consult online reviews, enabling quick identification of weak listings. Buyers benchmark results across providers, amplifying pressure on Yellow Pages Group to maintain competitive pricing and higher service levels. Outcome-linked pricing models, already adopted by some digital marketplaces, can align incentives and reduce disputes.

- Bargaining leverage: higher due to visible performance

- Benchmarking: cross-provider comparisons drive price competition

- Mitigation: outcome-linked pricing aligns incentives, lowers dispute risk

Bundling and cross-sell expectations

Clients increasingly demand bundled listings, web, SEO and paid media at discounted rates, shifting bargaining power to buyers seeking one-stop value; without clear differentiation these bundles compress margins for Yellow Pages Group Ltd. Packaging with proprietary data assets, advanced analytics and dedicated account support allows YPG to justify premiums and retain higher ARPU.

- Buyer leverage rises with bundle expectations

- Undifferentiated bundles lower margins

- Unique data/support enable premium pricing

SME buyers ROI-driven, price-sensitive; reviews sway 70-90%, raising churn risk

YPG customers (SMEs = 99.8% of Canadian firms, Statistics Canada 2024) are ROI-driven, price-sensitive and prone to churn; visible metrics and reviews (70–90% buyers consult reviews in 2024) increase bargaining power. Enterprise RFPs demand discounts and raise delivery costs; CMS/search concentration (WordPress ~43%, Google ~92% search share, 2024) eases switching.

| Metric | 2024 Value |

|---|---|

| SME share Canada | 99.8% |

| Google search share | ~92% |

| WordPress market | ~43% |

| Buyers using reviews | 70–90% |

Preview the Actual Deliverable

Yellow Pages Group Ltd. Porter's Five Forces Analysis

This preview shows the exact Yellow Pages Group Ltd. Porter's Five Forces Analysis you'll receive after purchase—no placeholders or samples. The full analysis is fully formatted, comprehensive and ready for immediate download and use. You're looking at the actual deliverable, complete and final.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Yellow Pages Group Ltd. faces moderate buyer power, intense digital competition from search platforms and local directories, and rising substitute threats as users shift to mobile and social search. Supplier influence is limited, while regulatory and technological shifts affect entry barriers and strategic options.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Yellow Pages Group Ltd.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on major ad-tech platforms

Google (Alphabet) and Meta—with 2023 ad revenues of about 224.5bn and 134.9bn USD respectively—and Microsoft’s search/LinkedIn ads dominate the ecosystems YPG depends on, so algorithm or policy shifts can quickly change campaign performance and CPCs. This concentration gives platforms outsized pricing and data leverage, forcing YPG to diversify channels and pursue formal partner status to mitigate risk.

Software, hosting, and data tool vendors

YPG’s website builds, analytics, SEO and automation rely heavily on third‑party SaaS, hosting and data providers, and while switching is feasible it incurs migration, retraining and service risk; vendor lock‑in via proprietary features raises effective switching costs. In 2024 over 90% of enterprises used cloud services and roughly 60% adopted multi‑cloud strategies, which can restore bargaining balance.

Creative and technical talent supply

Designers, developers, SEO specialists and content creators are critical inputs for Yellow Pages Group, and New Zealand’s small population of about 5.1 million in 2024 contributes to a tight digital talent market that strengthens supplier bargaining power. Remote hiring broadens the candidate pool but raises coordination and quality-control risks, often increasing reliance on agencies and freelancers. Investing in a strong employer brand and training pipelines can lower dependency on external talent and contain wage pressure.

Telecom and infrastructure dependencies

As of 2024 Yellow Pages Group depends on reliable CDN/cloud and telecom infrastructure for digital listings; outages or supplier price hikes can breach SLAs and compress margins, while redundancy via multi-cloud and CDNs reduces dependency but increases cost; contracted SLAs and multi-cloud architectures temper supplier bargaining power.

- CDN/cloud uptime critical — outages = SLA risk

- Supplier price hikes directly impact margins

- Redundancy lowers risk but raises OPEX

- Contracted SLAs and multi-cloud moderate supplier power

Publishing partners and directory data sources

Publishing partners, local listing networks, map providers and data aggregators (Google Maps 1B+ monthly users in 2024) materially influence Yellow Pages Group Ltd distribution reach; exclusive or premium placement agreements can impose high fees and restrictive data-usage terms, and the limited number of high-quality New Zealand data sources increases supplier leverage. Building proprietary data quality and first-party relationships reduces reliance and bargaining exposure.

- Local listing networks: concentration increases supplier power

- Map providers: Google Maps >1B users (2024)

- Data scarcity in NZ: fewer high-quality sources

- Mitigation: invest in proprietary first-party data

Ad platform dominance and maps (>1bn) squeeze CPCs; cloud lock-in and NZ talent raise OPEX

Google/Meta dominance (Google ad rev $224.5bn, Meta $134.9bn in 2023) and Google Maps >1bn monthly users (2024) give platforms outsized pricing/data leverage, risking CPCs and reach. SaaS/cloud vendor lock‑in and NZ talent tightness (pop ~5.1m) raise switching costs. Multi‑cloud, SLAs and first‑party data cut exposure but increase OPEX.

| Supplier | Metric | Impact | Mitigation |

|---|---|---|---|

| Ad platforms | Google $224.5bn (2023) | Pricing/data leverage | Diversify partners |

| Cloud/CDN | 90% cloud use (2024) | Uptime/cost risk | Multi‑cloud, SLAs |

| Talent | NZ pop 5.1m (2024) | Wage/scarcity | Training, remote hire |

| Maps/data | Maps >1bn users (2024) | Distribution control | Build first‑party data |

What is included in the product

Tailored Porter's Five Forces analysis for Yellow Pages Group Ltd. uncovering competitive intensity, buyer and supplier leverage, digital substitutes and disruptive threats, entry barriers protecting incumbency, and strategic implications for pricing and profitability.

A concise one-sheet Porter's Five Forces for Yellow Pages Group—clearly maps competitive pressures (digital entrants, advertisers, substitutes, supplier/buyer power) to speed strategic decisions and prioritize remedies in pitch decks or boardroom slides.

Customers Bargaining Power

Fragmented but price-sensitive SME base

Most YPG customers are SMEs—SMEs make up 99.8% of Canadian businesses (Statistics Canada 2024)—so budgets are tight and ROI-focused. Easy agency comparison and tendency to churn if outcomes lag increases price pressure. Short contract terms amplify customer leverage. Clear performance reporting and tiered packages can stabilize retention.

Enterprise and government procurement muscle

Enterprise and government clients run formal RFPs, demand bespoke integrations and steep discounts that can make high-volume wins margin-dilutive; compliance and elevated security mandates raise delivery costs and require account-based management to protect unit economics.

Low switching costs among digital agencies

Websites, SEO and ads transfer with limited friction given CMS dominance (WordPress ~43% of sites in 2024) and Google’s ~92% search share, while standardized tools (Google Ads, Analytics, Shopify) streamline replacement; formal onboarding/offboarding processes support frequent agency rotation, though proprietary integrations and data lead-generation hooks can materially increase client stickiness.

High transparency of performance

Real-time metrics and public reviews make underperformance visible, and industry studies in 2024 show 70–90% of buyers consult online reviews, enabling quick identification of weak listings. Buyers benchmark results across providers, amplifying pressure on Yellow Pages Group to maintain competitive pricing and higher service levels. Outcome-linked pricing models, already adopted by some digital marketplaces, can align incentives and reduce disputes.

- Bargaining leverage: higher due to visible performance

- Benchmarking: cross-provider comparisons drive price competition

- Mitigation: outcome-linked pricing aligns incentives, lowers dispute risk

Bundling and cross-sell expectations

Clients increasingly demand bundled listings, web, SEO and paid media at discounted rates, shifting bargaining power to buyers seeking one-stop value; without clear differentiation these bundles compress margins for Yellow Pages Group Ltd. Packaging with proprietary data assets, advanced analytics and dedicated account support allows YPG to justify premiums and retain higher ARPU.

- Buyer leverage rises with bundle expectations

- Undifferentiated bundles lower margins

- Unique data/support enable premium pricing

SME buyers ROI-driven, price-sensitive; reviews sway 70-90%, raising churn risk

YPG customers (SMEs = 99.8% of Canadian firms, Statistics Canada 2024) are ROI-driven, price-sensitive and prone to churn; visible metrics and reviews (70–90% buyers consult reviews in 2024) increase bargaining power. Enterprise RFPs demand discounts and raise delivery costs; CMS/search concentration (WordPress ~43%, Google ~92% search share, 2024) eases switching.

| Metric | 2024 Value |

|---|---|

| SME share Canada | 99.8% |

| Google search share | ~92% |

| WordPress market | ~43% |

| Buyers using reviews | 70–90% |

Preview the Actual Deliverable

Yellow Pages Group Ltd. Porter's Five Forces Analysis

This preview shows the exact Yellow Pages Group Ltd. Porter's Five Forces Analysis you'll receive after purchase—no placeholders or samples. The full analysis is fully formatted, comprehensive and ready for immediate download and use. You're looking at the actual deliverable, complete and final.