Yunnan Yuntianhua PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE analysis of Yunnan Yuntianhua—three to five concise insights into political risks, economic drivers, social trends, and regulatory shifts shaping its future. Ideal for investors and strategists, this brief reveals key external pressures and growth opportunities. Purchase the full, editable report to access the complete deep-dive and actionable recommendations for confident decision-making.

Political factors

Central agri-input policy support

China's 14th Five-Year Plan (2021–25) foregrounds food security and, combined with subsidies, VAT rebates and favorable rail freight for agri-inputs, strengthens demand visibility for urea, DAP and NPK; China accounts for roughly 30% of global fertilizer consumption. Support is often cyclical or performance-contingent, and a policy shift toward greener inputs could reallocate incentives across product lines.

Energy and coal governance

Coal mining and coal-chemical sectors face quota management, intensified safety inspections and temporary production caps that constrain feedstock for ammonia/urea chains. China produced about 4.35 billion tonnes of coal in 2023, so provincial coordination in Yunnan can materially buffer or amplify supply shocks to Yuntianhua. Government strategic stockpiling directives have in past years caused abrupt local price spikes and volatility in feedstock costs.

Export controls and trade diplomacy

China intermittently tightened fertilizer export inspections and quotas in 2023–2024 to protect domestic supply and stabilize prices, forcing Yunnan Yuntianhua to shift its export mix and press margins while weighing capacity utilization trade-offs. Trade relations with Southeast Asia and Belt and Road partners continue to shape market access and route choices. Currency moves and customs facilitation policies in 2024 materially affect price competitiveness and delivery times.

Regional development and SOE ecosystem

Local governments in Yunnan actively promote industrial clusters, logistics hubs and park infrastructure that lower operating frictions for chemical producers, while coordination with state-linked utilities helps secure priority power and rail capacity for large SOEs.

Compliance with regional industrial upgrading and emissions standards often forces incremental capex for process upgrades and pollution controls, even as preferential land allocations and concessional financing are increasingly conditional on performance and environmental benchmarks.

- Cluster infrastructure reduces logistics costs and time-to-market

- State utility coordination secures power/rail capacity for large plants

- Industrial upgrade rules drive mandatory capex for emissions controls

- Preferential land/finance tied to performance and environmental KPIs

Geopolitical volatility in inputs

Phosphate rock sourcing and sulfur imports are geopolitically sensitive; Morocco holds roughly 70% of global phosphate reserves (USGS 2024), concentrating supply risk. Disruptions have triggered Chinese domestic allocation and state procurement; bilateral agreements can secure volumes but at policy-determined prices, creating planning uncertainty for Yunnan Yuntianhua.

- Morocco ~70% reserves (USGS 2024)

- State procurement stabilizes supply at policy prices

- High planning uncertainty for raw-material strategies

China policy and coal caps tighten fertilizer markets; Morocco phosphate concentration risks supply

China's 14th Five-Year Plan and subsidies sustain domestic fertilizer demand (China ~30% of global consumption), but greener-input policy risks shifting incentives. Coal quotas and safety caps (China coal 4.35bn t in 2023) constrain ammonia feedstock and add volatility. Export inspections in 2023–24 tightened margins; Morocco holds ~70% phosphate reserves (USGS 2024), concentrating raw-material risk.

| Factor | Key metric |

|---|---|

| China fertilizer share | ~30% |

| China coal (2023) | 4.35bn t |

| Phosphate reserves | Morocco ~70% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Yunnan Yuntianhua, with data-backed trends, region- and industry-specific examples, forward-looking scenario insights and actionable implications—designed for executives, advisors and investors and formatted for direct inclusion in plans, decks or reports.

A clear, concise PESTLE summary of Yunnan Yuntianhua that’s visually segmented by factor for rapid risk assessment and easy insertion into presentations, enabling teams to align quickly on external threats, regulatory shifts, and market positioning during planning sessions.

Economic factors

Commodity price cycles

Fertilizer margins for Yunnan Yuntianhua closely track ammonia, sulfur, phosphate rock and energy, with energy comprising roughly 30–50% of ammonia production cost and ammonia prices swinging up to about ±60% between 2021–24, driving substantial margin volatility. Global crop-price cycles affect farmer affordability and application rates—fertilizer use declined an estimated 5–8% during the 2022–23 price spike. Counter-cyclical inventory management is therefore critical to stabilize quarterly earnings, while hedging and long-term offtake agreements reduce spot exposure but introduce basis risk.

Domestic demand elasticity

China maintains a baseline fertilizer demand via a policy to secure roughly 120 million hectares of grain and mechanization rates above 70%, while the zero-growth fertilizer-use target achieved in 2020 and ongoing efficiency programs have cut per-hectare application rates.

FX and export competitiveness

RMB movements (around 7.2 CNY/USD in 2024) materially alter Yunnan Yuntianhua’s export pricing versus buyers in Russia, the Middle East and North Africa, shifting competitiveness against peers priced in stronger currencies. Freight and container rates have fallen roughly 70% from 2021 peaks, improving netbacks to Southeast and South Asia but keeping margins sensitive to short-term spikes. Export curbs, rebates and tariff changes periodically open or close arbitrage windows, forcing rapid route and customer reallocation. Active portfolio mix optimization across currencies and destinations is essential to defend margins amid FX and logistics volatility.

Capital intensity and financing

Ammonia, DAP and coal-chemical assets at Yunnan Yuntianhua demand heavy maintenance capex and periodic debottlenecking, compressing free cash flow and extending payback horizons. Interest-rate backdrop (China 1Y LPR 3.65% in 2024) and access to green finance materially shape WACC and project affordability. Timing capex to market cycles drives ROIC, while government-backed credit lines are increasingly conditional on ESG metrics and emissions targets.

- Capex intensity: high maintenance and debottlenecking needs

- WACC driver: 1Y LPR 3.65% (2024) and green finance terms

- ROIC hinge: project timing vs market windows

- Credit: government lines tied to ESG compliance

Energy cost and power availability

Electricity and coal prices directly drive Yunnan Yuntianhua's urea and phosphate conversion costs; China industrial power tariffs averaged about 0.68 CNY/kWh in 2023 (NDRC), while thermal coal price volatility in 2024 raised feedstock costs. Yunnan's hydropower seasonality lowers tariffs during wet months but increases variability and operational scheduling risk. Demand response programs can mandate peak curtailments; long-term power contracts hedge price swings but limit flexibility.

- 0.68 CNY/kWh average industrial tariff (2023, NDRC)

- Hydropower seasonality: lower seasonal tariffs, higher variability

- Demand response may curtail peak operations

- Long-term contracts hedge volatility but reduce operational flexibility

China policy and coal caps tighten fertilizer markets; Morocco phosphate concentration risks supply

Fertilizer margins track ammonia/sulfur/phosphate and energy (energy = 30–50% of ammonia cost; ammonia ±60% 2021–24), causing high margin volatility. China policy secures baseline demand (zero-growth use since 2020; application fell ~5–8% during 2022–23 spike). Key drivers: RMB ~7.2 CNY/USD (2024), 1Y LPR 3.65% (2024), industrial power ~0.68 CNY/kWh (2023).

| Metric | Value |

|---|---|

| Ammonia price swing (2021–24) | ±60% |

| Energy share of ammonia cost | 30–50% |

| Fertilizer use dip (2022–23) | 5–8% |

| RMB/USD (2024) | ~7.2 |

| 1Y LPR (2024) | 3.65% |

| Industrial power (2023) | 0.68 CNY/kWh |

What You See Is What You Get

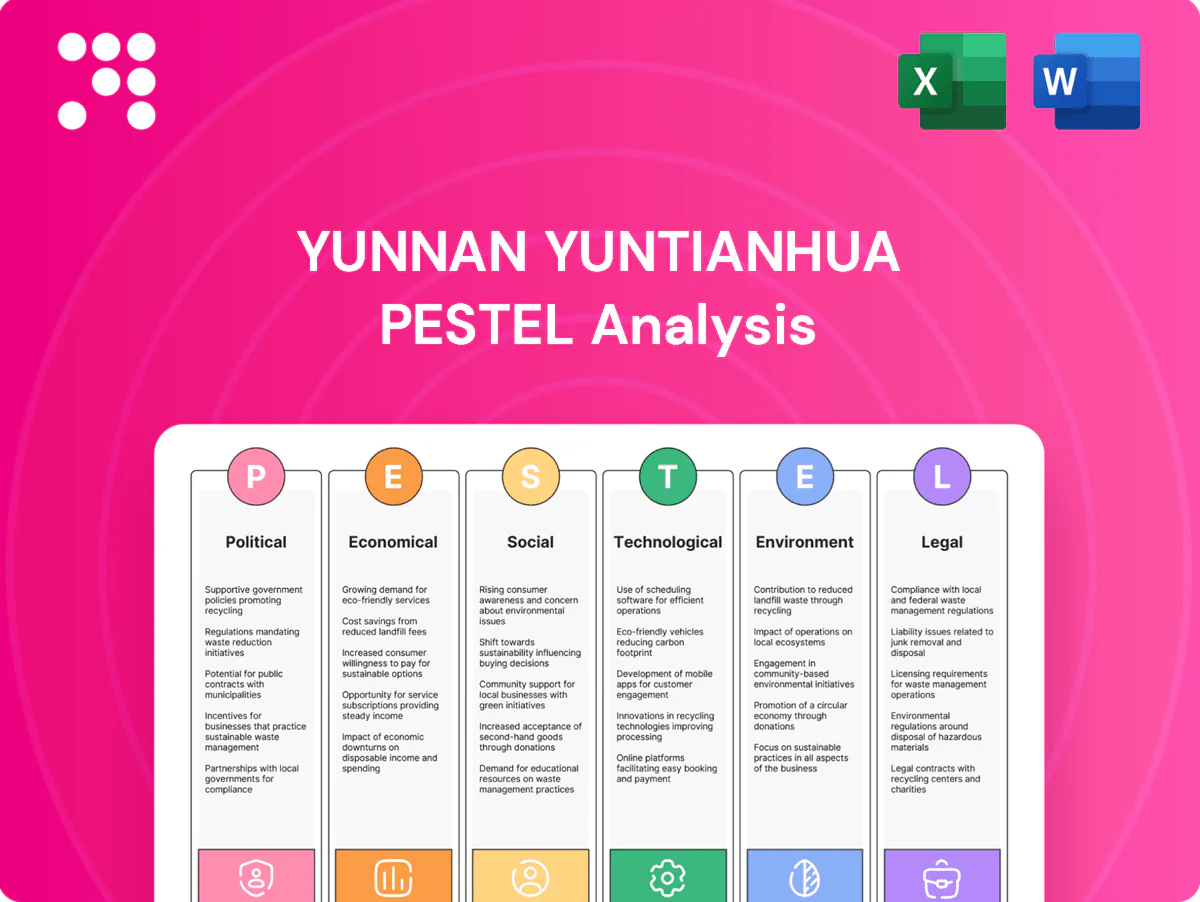

Yunnan Yuntianhua PESTLE Analysis

The preview shown here is the exact Yunnan Yuntianhua PESTLE analysis you’ll receive after purchase—fully formatted, comprehensive, and ready to use. It covers political, economic, social, technological, legal, and environmental factors affecting the company. No placeholders or teasers—this is the final file available for immediate download.

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE analysis of Yunnan Yuntianhua—three to five concise insights into political risks, economic drivers, social trends, and regulatory shifts shaping its future. Ideal for investors and strategists, this brief reveals key external pressures and growth opportunities. Purchase the full, editable report to access the complete deep-dive and actionable recommendations for confident decision-making.

Political factors

Central agri-input policy support

China's 14th Five-Year Plan (2021–25) foregrounds food security and, combined with subsidies, VAT rebates and favorable rail freight for agri-inputs, strengthens demand visibility for urea, DAP and NPK; China accounts for roughly 30% of global fertilizer consumption. Support is often cyclical or performance-contingent, and a policy shift toward greener inputs could reallocate incentives across product lines.

Energy and coal governance

Coal mining and coal-chemical sectors face quota management, intensified safety inspections and temporary production caps that constrain feedstock for ammonia/urea chains. China produced about 4.35 billion tonnes of coal in 2023, so provincial coordination in Yunnan can materially buffer or amplify supply shocks to Yuntianhua. Government strategic stockpiling directives have in past years caused abrupt local price spikes and volatility in feedstock costs.

Export controls and trade diplomacy

China intermittently tightened fertilizer export inspections and quotas in 2023–2024 to protect domestic supply and stabilize prices, forcing Yunnan Yuntianhua to shift its export mix and press margins while weighing capacity utilization trade-offs. Trade relations with Southeast Asia and Belt and Road partners continue to shape market access and route choices. Currency moves and customs facilitation policies in 2024 materially affect price competitiveness and delivery times.

Regional development and SOE ecosystem

Local governments in Yunnan actively promote industrial clusters, logistics hubs and park infrastructure that lower operating frictions for chemical producers, while coordination with state-linked utilities helps secure priority power and rail capacity for large SOEs.

Compliance with regional industrial upgrading and emissions standards often forces incremental capex for process upgrades and pollution controls, even as preferential land allocations and concessional financing are increasingly conditional on performance and environmental benchmarks.

- Cluster infrastructure reduces logistics costs and time-to-market

- State utility coordination secures power/rail capacity for large plants

- Industrial upgrade rules drive mandatory capex for emissions controls

- Preferential land/finance tied to performance and environmental KPIs

Geopolitical volatility in inputs

Phosphate rock sourcing and sulfur imports are geopolitically sensitive; Morocco holds roughly 70% of global phosphate reserves (USGS 2024), concentrating supply risk. Disruptions have triggered Chinese domestic allocation and state procurement; bilateral agreements can secure volumes but at policy-determined prices, creating planning uncertainty for Yunnan Yuntianhua.

- Morocco ~70% reserves (USGS 2024)

- State procurement stabilizes supply at policy prices

- High planning uncertainty for raw-material strategies

China policy and coal caps tighten fertilizer markets; Morocco phosphate concentration risks supply

China's 14th Five-Year Plan and subsidies sustain domestic fertilizer demand (China ~30% of global consumption), but greener-input policy risks shifting incentives. Coal quotas and safety caps (China coal 4.35bn t in 2023) constrain ammonia feedstock and add volatility. Export inspections in 2023–24 tightened margins; Morocco holds ~70% phosphate reserves (USGS 2024), concentrating raw-material risk.

| Factor | Key metric |

|---|---|

| China fertilizer share | ~30% |

| China coal (2023) | 4.35bn t |

| Phosphate reserves | Morocco ~70% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Yunnan Yuntianhua, with data-backed trends, region- and industry-specific examples, forward-looking scenario insights and actionable implications—designed for executives, advisors and investors and formatted for direct inclusion in plans, decks or reports.

A clear, concise PESTLE summary of Yunnan Yuntianhua that’s visually segmented by factor for rapid risk assessment and easy insertion into presentations, enabling teams to align quickly on external threats, regulatory shifts, and market positioning during planning sessions.

Economic factors

Commodity price cycles

Fertilizer margins for Yunnan Yuntianhua closely track ammonia, sulfur, phosphate rock and energy, with energy comprising roughly 30–50% of ammonia production cost and ammonia prices swinging up to about ±60% between 2021–24, driving substantial margin volatility. Global crop-price cycles affect farmer affordability and application rates—fertilizer use declined an estimated 5–8% during the 2022–23 price spike. Counter-cyclical inventory management is therefore critical to stabilize quarterly earnings, while hedging and long-term offtake agreements reduce spot exposure but introduce basis risk.

Domestic demand elasticity

China maintains a baseline fertilizer demand via a policy to secure roughly 120 million hectares of grain and mechanization rates above 70%, while the zero-growth fertilizer-use target achieved in 2020 and ongoing efficiency programs have cut per-hectare application rates.

FX and export competitiveness

RMB movements (around 7.2 CNY/USD in 2024) materially alter Yunnan Yuntianhua’s export pricing versus buyers in Russia, the Middle East and North Africa, shifting competitiveness against peers priced in stronger currencies. Freight and container rates have fallen roughly 70% from 2021 peaks, improving netbacks to Southeast and South Asia but keeping margins sensitive to short-term spikes. Export curbs, rebates and tariff changes periodically open or close arbitrage windows, forcing rapid route and customer reallocation. Active portfolio mix optimization across currencies and destinations is essential to defend margins amid FX and logistics volatility.

Capital intensity and financing

Ammonia, DAP and coal-chemical assets at Yunnan Yuntianhua demand heavy maintenance capex and periodic debottlenecking, compressing free cash flow and extending payback horizons. Interest-rate backdrop (China 1Y LPR 3.65% in 2024) and access to green finance materially shape WACC and project affordability. Timing capex to market cycles drives ROIC, while government-backed credit lines are increasingly conditional on ESG metrics and emissions targets.

- Capex intensity: high maintenance and debottlenecking needs

- WACC driver: 1Y LPR 3.65% (2024) and green finance terms

- ROIC hinge: project timing vs market windows

- Credit: government lines tied to ESG compliance

Energy cost and power availability

Electricity and coal prices directly drive Yunnan Yuntianhua's urea and phosphate conversion costs; China industrial power tariffs averaged about 0.68 CNY/kWh in 2023 (NDRC), while thermal coal price volatility in 2024 raised feedstock costs. Yunnan's hydropower seasonality lowers tariffs during wet months but increases variability and operational scheduling risk. Demand response programs can mandate peak curtailments; long-term power contracts hedge price swings but limit flexibility.

- 0.68 CNY/kWh average industrial tariff (2023, NDRC)

- Hydropower seasonality: lower seasonal tariffs, higher variability

- Demand response may curtail peak operations

- Long-term contracts hedge volatility but reduce operational flexibility

China policy and coal caps tighten fertilizer markets; Morocco phosphate concentration risks supply

Fertilizer margins track ammonia/sulfur/phosphate and energy (energy = 30–50% of ammonia cost; ammonia ±60% 2021–24), causing high margin volatility. China policy secures baseline demand (zero-growth use since 2020; application fell ~5–8% during 2022–23 spike). Key drivers: RMB ~7.2 CNY/USD (2024), 1Y LPR 3.65% (2024), industrial power ~0.68 CNY/kWh (2023).

| Metric | Value |

|---|---|

| Ammonia price swing (2021–24) | ±60% |

| Energy share of ammonia cost | 30–50% |

| Fertilizer use dip (2022–23) | 5–8% |

| RMB/USD (2024) | ~7.2 |

| 1Y LPR (2024) | 3.65% |

| Industrial power (2023) | 0.68 CNY/kWh |

What You See Is What You Get

Yunnan Yuntianhua PESTLE Analysis

The preview shown here is the exact Yunnan Yuntianhua PESTLE analysis you’ll receive after purchase—fully formatted, comprehensive, and ready to use. It covers political, economic, social, technological, legal, and environmental factors affecting the company. No placeholders or teasers—this is the final file available for immediate download.

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE analysis of Yunnan Yuntianhua—three to five concise insights into political risks, economic drivers, social trends, and regulatory shifts shaping its future. Ideal for investors and strategists, this brief reveals key external pressures and growth opportunities. Purchase the full, editable report to access the complete deep-dive and actionable recommendations for confident decision-making.

Political factors

Central agri-input policy support

China's 14th Five-Year Plan (2021–25) foregrounds food security and, combined with subsidies, VAT rebates and favorable rail freight for agri-inputs, strengthens demand visibility for urea, DAP and NPK; China accounts for roughly 30% of global fertilizer consumption. Support is often cyclical or performance-contingent, and a policy shift toward greener inputs could reallocate incentives across product lines.

Energy and coal governance

Coal mining and coal-chemical sectors face quota management, intensified safety inspections and temporary production caps that constrain feedstock for ammonia/urea chains. China produced about 4.35 billion tonnes of coal in 2023, so provincial coordination in Yunnan can materially buffer or amplify supply shocks to Yuntianhua. Government strategic stockpiling directives have in past years caused abrupt local price spikes and volatility in feedstock costs.

Export controls and trade diplomacy

China intermittently tightened fertilizer export inspections and quotas in 2023–2024 to protect domestic supply and stabilize prices, forcing Yunnan Yuntianhua to shift its export mix and press margins while weighing capacity utilization trade-offs. Trade relations with Southeast Asia and Belt and Road partners continue to shape market access and route choices. Currency moves and customs facilitation policies in 2024 materially affect price competitiveness and delivery times.

Regional development and SOE ecosystem

Local governments in Yunnan actively promote industrial clusters, logistics hubs and park infrastructure that lower operating frictions for chemical producers, while coordination with state-linked utilities helps secure priority power and rail capacity for large SOEs.

Compliance with regional industrial upgrading and emissions standards often forces incremental capex for process upgrades and pollution controls, even as preferential land allocations and concessional financing are increasingly conditional on performance and environmental benchmarks.

- Cluster infrastructure reduces logistics costs and time-to-market

- State utility coordination secures power/rail capacity for large plants

- Industrial upgrade rules drive mandatory capex for emissions controls

- Preferential land/finance tied to performance and environmental KPIs

Geopolitical volatility in inputs

Phosphate rock sourcing and sulfur imports are geopolitically sensitive; Morocco holds roughly 70% of global phosphate reserves (USGS 2024), concentrating supply risk. Disruptions have triggered Chinese domestic allocation and state procurement; bilateral agreements can secure volumes but at policy-determined prices, creating planning uncertainty for Yunnan Yuntianhua.

- Morocco ~70% reserves (USGS 2024)

- State procurement stabilizes supply at policy prices

- High planning uncertainty for raw-material strategies

China policy and coal caps tighten fertilizer markets; Morocco phosphate concentration risks supply

China's 14th Five-Year Plan and subsidies sustain domestic fertilizer demand (China ~30% of global consumption), but greener-input policy risks shifting incentives. Coal quotas and safety caps (China coal 4.35bn t in 2023) constrain ammonia feedstock and add volatility. Export inspections in 2023–24 tightened margins; Morocco holds ~70% phosphate reserves (USGS 2024), concentrating raw-material risk.

| Factor | Key metric |

|---|---|

| China fertilizer share | ~30% |

| China coal (2023) | 4.35bn t |

| Phosphate reserves | Morocco ~70% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Yunnan Yuntianhua, with data-backed trends, region- and industry-specific examples, forward-looking scenario insights and actionable implications—designed for executives, advisors and investors and formatted for direct inclusion in plans, decks or reports.

A clear, concise PESTLE summary of Yunnan Yuntianhua that’s visually segmented by factor for rapid risk assessment and easy insertion into presentations, enabling teams to align quickly on external threats, regulatory shifts, and market positioning during planning sessions.

Economic factors

Commodity price cycles

Fertilizer margins for Yunnan Yuntianhua closely track ammonia, sulfur, phosphate rock and energy, with energy comprising roughly 30–50% of ammonia production cost and ammonia prices swinging up to about ±60% between 2021–24, driving substantial margin volatility. Global crop-price cycles affect farmer affordability and application rates—fertilizer use declined an estimated 5–8% during the 2022–23 price spike. Counter-cyclical inventory management is therefore critical to stabilize quarterly earnings, while hedging and long-term offtake agreements reduce spot exposure but introduce basis risk.

Domestic demand elasticity

China maintains a baseline fertilizer demand via a policy to secure roughly 120 million hectares of grain and mechanization rates above 70%, while the zero-growth fertilizer-use target achieved in 2020 and ongoing efficiency programs have cut per-hectare application rates.

FX and export competitiveness

RMB movements (around 7.2 CNY/USD in 2024) materially alter Yunnan Yuntianhua’s export pricing versus buyers in Russia, the Middle East and North Africa, shifting competitiveness against peers priced in stronger currencies. Freight and container rates have fallen roughly 70% from 2021 peaks, improving netbacks to Southeast and South Asia but keeping margins sensitive to short-term spikes. Export curbs, rebates and tariff changes periodically open or close arbitrage windows, forcing rapid route and customer reallocation. Active portfolio mix optimization across currencies and destinations is essential to defend margins amid FX and logistics volatility.

Capital intensity and financing

Ammonia, DAP and coal-chemical assets at Yunnan Yuntianhua demand heavy maintenance capex and periodic debottlenecking, compressing free cash flow and extending payback horizons. Interest-rate backdrop (China 1Y LPR 3.65% in 2024) and access to green finance materially shape WACC and project affordability. Timing capex to market cycles drives ROIC, while government-backed credit lines are increasingly conditional on ESG metrics and emissions targets.

- Capex intensity: high maintenance and debottlenecking needs

- WACC driver: 1Y LPR 3.65% (2024) and green finance terms

- ROIC hinge: project timing vs market windows

- Credit: government lines tied to ESG compliance

Energy cost and power availability

Electricity and coal prices directly drive Yunnan Yuntianhua's urea and phosphate conversion costs; China industrial power tariffs averaged about 0.68 CNY/kWh in 2023 (NDRC), while thermal coal price volatility in 2024 raised feedstock costs. Yunnan's hydropower seasonality lowers tariffs during wet months but increases variability and operational scheduling risk. Demand response programs can mandate peak curtailments; long-term power contracts hedge price swings but limit flexibility.

- 0.68 CNY/kWh average industrial tariff (2023, NDRC)

- Hydropower seasonality: lower seasonal tariffs, higher variability

- Demand response may curtail peak operations

- Long-term contracts hedge volatility but reduce operational flexibility

China policy and coal caps tighten fertilizer markets; Morocco phosphate concentration risks supply

Fertilizer margins track ammonia/sulfur/phosphate and energy (energy = 30–50% of ammonia cost; ammonia ±60% 2021–24), causing high margin volatility. China policy secures baseline demand (zero-growth use since 2020; application fell ~5–8% during 2022–23 spike). Key drivers: RMB ~7.2 CNY/USD (2024), 1Y LPR 3.65% (2024), industrial power ~0.68 CNY/kWh (2023).

| Metric | Value |

|---|---|

| Ammonia price swing (2021–24) | ±60% |

| Energy share of ammonia cost | 30–50% |

| Fertilizer use dip (2022–23) | 5–8% |

| RMB/USD (2024) | ~7.2 |

| 1Y LPR (2024) | 3.65% |

| Industrial power (2023) | 0.68 CNY/kWh |

What You See Is What You Get

Yunnan Yuntianhua PESTLE Analysis

The preview shown here is the exact Yunnan Yuntianhua PESTLE analysis you’ll receive after purchase—fully formatted, comprehensive, and ready to use. It covers political, economic, social, technological, legal, and environmental factors affecting the company. No placeholders or teasers—this is the final file available for immediate download.