Yuexiu Property Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Yuexiu Property faces moderate buyer power, intense developer rivalry, and location-driven supplier constraints that shape its margins and growth choices.

Regulatory shifts and urbanization trends heighten entry barriers yet create niche opportunities in mixed-use and affordable housing segments.

Substitutes and financing risk remain watchpoints that could compress returns if macro conditions worsen.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Yuexiu Property’s competitive dynamics and strategic implications in depth.

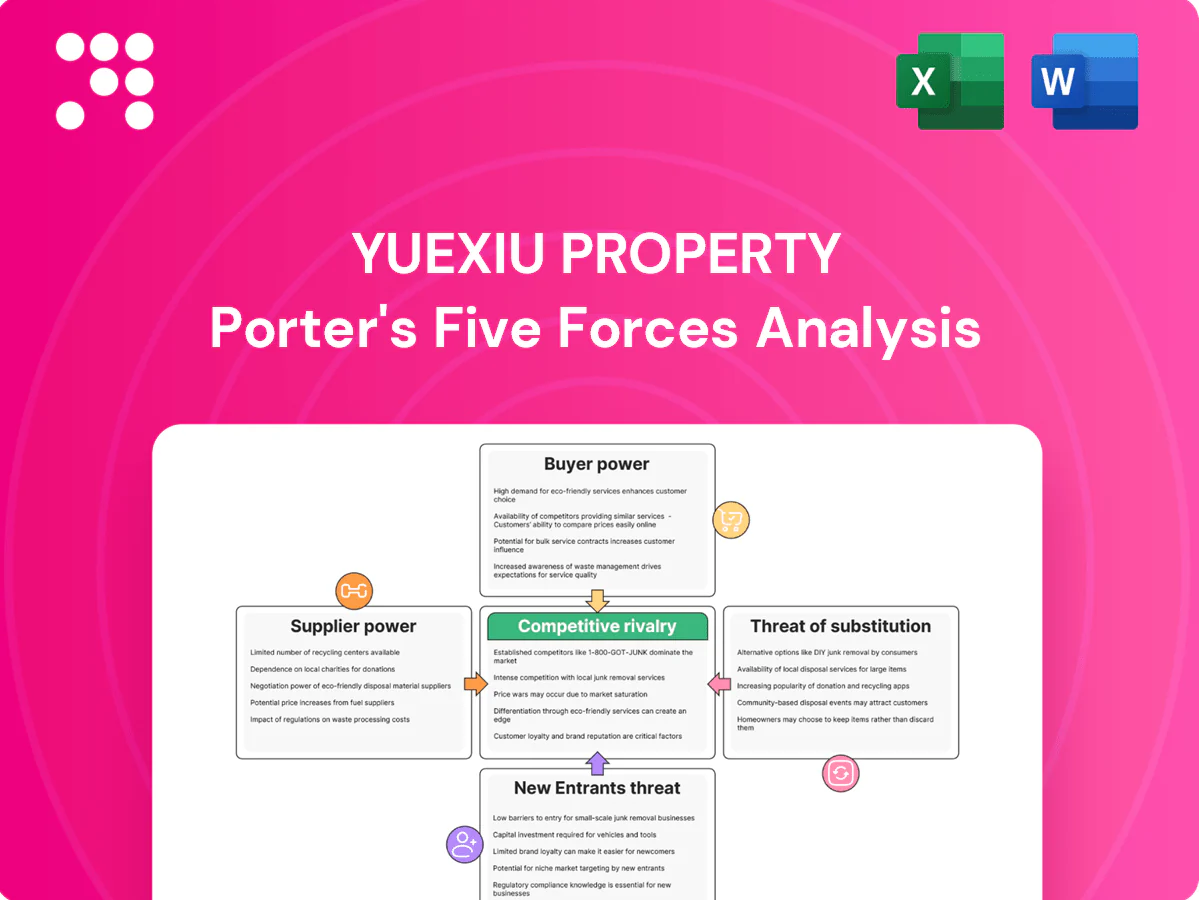

Suppliers Bargaining Power

Fragmented construction inputs

China's building-materials sector is highly fragmented despite scale—national cement output was about 2.18 billion tonnes in 2023 and crude steel production ~1.03 billion tonnes, diluting individual supplier leverage and enabling Yuexiu to multi-source cement, steel and fittings across provinces. Long-term framework contracts help stabilize cost and quality, while switching costs exist but remain manageable due to industry standardization and regional supplier depth.

Land as a strategic supplier

Primary urban land in China is state-owned and effectively 100% controlled by local governments, creating quasi-monopoly power over supply; auction and tender formats account for the lion’s share of transfers (historically exceeding 90%), driving price discovery and access. Yuexiu’s SOE parentage (Yuexiu Group) and municipal ties in Guangzhou mitigate bidding pressure and financing constraints. Nonetheless, prime central-city parcels remain scarce and command significant premiums, pressuring margins and land-cost intensity.

Specialized services dependence

Specialized design institutes, MEP engineers and façade specialists can exert significant bargaining power over Yuexiu Property (HKEX: 0123) on complex projects, because technical IP and capacity constraints materially raise switching costs. Yuexiu offsets this by building in-house MEP/façade capabilities and maintaining preferred-vendor rosters. Pipeline visibility as a major Guangdong developer helps secure priority terms from constrained suppliers.

Financing as a supply input

Capital providers and state banks shape Yuexiu Property project cadence and financing cost; China’s 1-year LPR stood at 3.45% in 2024, anchoring onshore lending pricing while regulatory curbs boost the leverage of approved lenders. Yuexiu’s investment-grade SOE ties typically secure lower borrowing spreads versus private peers, but credit cycles in 2024 showed abrupt tightening risks that can raise marginal funding costs quickly.

- State banks: dominant project financier

- 1y LPR 2024: 3.45%

- SOE status: lower spreads vs peers

- Credit cycles: sudden tightening risk

Property management ecosystems

Where third-party O&M is used, scale PMCs push standardized fee schedules, limiting supplier markup; in 2024 Yuexiu’s in-house property management arm reduces external dependency and bargaining leverage of vendors.

Cross-selling and bundled services across Yuexiu’s portfolio strengthen negotiating position, while service-quality SLAs tie payments to KPIs to keep costs and outcomes aligned.

- 2024: in-house PM reduces supplier dependency

- Standardized PMC fees constrain vendor margins

- Bundled services improve procurement leverage

- SLAs align cost with service KPIs

Fragmented materials, auctioned land scarcity, lender pressure 3.45%

Fragmented building-materials supply (cement 2.18bn t, crude steel 1.03bn t in 2023) limits single-supplier leverage and enables multi-sourcing for Yuexiu.

Primary land is state-owned and auction-dominated; Yuexiu’s SOE parentage eases land access though prime urban plots remain scarce and costly.

Specialized contractors and lenders (1y LPR 2024: 3.45%) can squeeze margins, but in-house MEP/façade and PM capabilities reduce external supplier power.

| Metric | Value |

|---|---|

| Cement output 2023 | 2.18bn t |

| Crude steel 2023 | 1.03bn t |

| 1y LPR 2024 | 3.45% |

What is included in the product

Tailored Porter's Five Forces analysis for Yuexiu Property uncovering competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and strategic implications for pricing, profitability and market positioning—fully editable for integration into investor reports, strategy decks, or academic work.

A concise one-sheet Porter’s Five Forces summary for Yuexiu Property—ideal for quick investment or strategic decisions. Customize pressure levels by region, regulation or market data to reflect evolving risks and opportunities.

Customers Bargaining Power

Price-sensitive homebuyers

Households face affordability constraints as urban disposable income growth slowed to about 3% in 2024, boosting price sensitivity; widespread discounting and promotions have become common, increasing buyer leverage. Yuexiu’s strong brand and a delivery track record in tier-1/2 cities lets it sustain a premium, yet sentiment still swings quickly on macro headlines and policy shifts.

Institutional commercial tenants

Anchor tenants and MNCs wield strong bargaining power, routinely securing rent-free periods and fit-out subsidies during negotiations. Vacancy risk in emerging CBDs in 2024 heightened tenant leverage, forcing landlords to offer deeper concessions. Yuexiu leverages mixed-use synergies—retail, hotel and office—to attract and retain anchors, while longer lease terms smooth cash flows yet lock in those concessions.

Develop-to-sell intermediaries

Channel agents and online platforms materially shape sales velocity for Yuexiu, with agent commissions in China typically around 1–3% giving intermediaries leverage in weak markets; Yuexiu offsets this by balancing direct and channel sales to control SG&A and distribution costs, while ramping digital lead-generation to cut dependence on high-commission channels.

After-sales expectations

Buyers demand strong warranties and rapid defect remediation, and social media amplification—China had about 1.05 billion mobile internet users in 2024 (CNNIC)—increases implicit buyer power by widening reputational and refund risk for developers. Yuexiu Property (HKEX: 0123) leverages its property management arm to differentiate service and accelerate rectification, lowering refund and penalty exposure. Faster fixes reduce contract breach claims and negative online virality.

- Warranty focus: faster rectification lowers refund/penalty risk

- Social amplification: ~1.05 billion mobile users in 2024

- Differentiator: Yuexiu’s in-house management improves response speed

Corporate buyers and SOEs

Corporate buyers and SOEs buy industrial and office blocks with strong bargaining power, often extracting meaningful discounts in exchange for large, certain take-ups; Yuexiu mitigates this by bundling assets across its portfolio to preserve pricing. The group structures deals with staged payments and sale-leaseback options to balance price concessions against financing certainty for sellers. Counterparty credibility often trumps headline price in negotiations, enabling Yuexiu to protect margins while closing large transactions.

- Bulk buyers: high negotiation leverage

- Yuexiu tactic: portfolio bundling to retain value

- Deal terms: structured payments, sale-leasebacks

- Outcome: trade-off between price and take-up certainty

Urban income ~3% increases price bargaining; operators bundle as mobile users hit 1.05bn

Customer bargaining rose in 2024 as urban disposable income growth slowed to ~3%, boosting price sensitivity; widespread discounting increased leverage. Anchor tenants and bulk buyers extract concessions but Yuexiu offsets via mixed-use synergies, portfolio bundling and in-house property management. Digital channels (1.05 billion mobile users in 2024) magnify reputational risk.

| Metric | 2024 | Impact |

|---|---|---|

| Urban disposable income growth | ~3% | Higher price sensitivity |

| Mobile users | 1.05bn | Amplified reputational risk |

Same Document Delivered

Yuexiu Property Porter's Five Forces Analysis

This preview is the exact Porter’s Five Forces analysis of Yuexiu Property you’ll receive—no placeholders or samples. The full document is professionally formatted, comprehensive, and ready for immediate download upon purchase. What you see here is precisely the deliverable available to you instantly after payment.

Don't Miss the Bigger Picture

Yuexiu Property faces moderate buyer power, intense developer rivalry, and location-driven supplier constraints that shape its margins and growth choices.

Regulatory shifts and urbanization trends heighten entry barriers yet create niche opportunities in mixed-use and affordable housing segments.

Substitutes and financing risk remain watchpoints that could compress returns if macro conditions worsen.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Yuexiu Property’s competitive dynamics and strategic implications in depth.

Suppliers Bargaining Power

Fragmented construction inputs

China's building-materials sector is highly fragmented despite scale—national cement output was about 2.18 billion tonnes in 2023 and crude steel production ~1.03 billion tonnes, diluting individual supplier leverage and enabling Yuexiu to multi-source cement, steel and fittings across provinces. Long-term framework contracts help stabilize cost and quality, while switching costs exist but remain manageable due to industry standardization and regional supplier depth.

Land as a strategic supplier

Primary urban land in China is state-owned and effectively 100% controlled by local governments, creating quasi-monopoly power over supply; auction and tender formats account for the lion’s share of transfers (historically exceeding 90%), driving price discovery and access. Yuexiu’s SOE parentage (Yuexiu Group) and municipal ties in Guangzhou mitigate bidding pressure and financing constraints. Nonetheless, prime central-city parcels remain scarce and command significant premiums, pressuring margins and land-cost intensity.

Specialized services dependence

Specialized design institutes, MEP engineers and façade specialists can exert significant bargaining power over Yuexiu Property (HKEX: 0123) on complex projects, because technical IP and capacity constraints materially raise switching costs. Yuexiu offsets this by building in-house MEP/façade capabilities and maintaining preferred-vendor rosters. Pipeline visibility as a major Guangdong developer helps secure priority terms from constrained suppliers.

Financing as a supply input

Capital providers and state banks shape Yuexiu Property project cadence and financing cost; China’s 1-year LPR stood at 3.45% in 2024, anchoring onshore lending pricing while regulatory curbs boost the leverage of approved lenders. Yuexiu’s investment-grade SOE ties typically secure lower borrowing spreads versus private peers, but credit cycles in 2024 showed abrupt tightening risks that can raise marginal funding costs quickly.

- State banks: dominant project financier

- 1y LPR 2024: 3.45%

- SOE status: lower spreads vs peers

- Credit cycles: sudden tightening risk

Property management ecosystems

Where third-party O&M is used, scale PMCs push standardized fee schedules, limiting supplier markup; in 2024 Yuexiu’s in-house property management arm reduces external dependency and bargaining leverage of vendors.

Cross-selling and bundled services across Yuexiu’s portfolio strengthen negotiating position, while service-quality SLAs tie payments to KPIs to keep costs and outcomes aligned.

- 2024: in-house PM reduces supplier dependency

- Standardized PMC fees constrain vendor margins

- Bundled services improve procurement leverage

- SLAs align cost with service KPIs

Fragmented materials, auctioned land scarcity, lender pressure 3.45%

Fragmented building-materials supply (cement 2.18bn t, crude steel 1.03bn t in 2023) limits single-supplier leverage and enables multi-sourcing for Yuexiu.

Primary land is state-owned and auction-dominated; Yuexiu’s SOE parentage eases land access though prime urban plots remain scarce and costly.

Specialized contractors and lenders (1y LPR 2024: 3.45%) can squeeze margins, but in-house MEP/façade and PM capabilities reduce external supplier power.

| Metric | Value |

|---|---|

| Cement output 2023 | 2.18bn t |

| Crude steel 2023 | 1.03bn t |

| 1y LPR 2024 | 3.45% |

What is included in the product

Tailored Porter's Five Forces analysis for Yuexiu Property uncovering competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and strategic implications for pricing, profitability and market positioning—fully editable for integration into investor reports, strategy decks, or academic work.

A concise one-sheet Porter’s Five Forces summary for Yuexiu Property—ideal for quick investment or strategic decisions. Customize pressure levels by region, regulation or market data to reflect evolving risks and opportunities.

Customers Bargaining Power

Price-sensitive homebuyers

Households face affordability constraints as urban disposable income growth slowed to about 3% in 2024, boosting price sensitivity; widespread discounting and promotions have become common, increasing buyer leverage. Yuexiu’s strong brand and a delivery track record in tier-1/2 cities lets it sustain a premium, yet sentiment still swings quickly on macro headlines and policy shifts.

Institutional commercial tenants

Anchor tenants and MNCs wield strong bargaining power, routinely securing rent-free periods and fit-out subsidies during negotiations. Vacancy risk in emerging CBDs in 2024 heightened tenant leverage, forcing landlords to offer deeper concessions. Yuexiu leverages mixed-use synergies—retail, hotel and office—to attract and retain anchors, while longer lease terms smooth cash flows yet lock in those concessions.

Develop-to-sell intermediaries

Channel agents and online platforms materially shape sales velocity for Yuexiu, with agent commissions in China typically around 1–3% giving intermediaries leverage in weak markets; Yuexiu offsets this by balancing direct and channel sales to control SG&A and distribution costs, while ramping digital lead-generation to cut dependence on high-commission channels.

After-sales expectations

Buyers demand strong warranties and rapid defect remediation, and social media amplification—China had about 1.05 billion mobile internet users in 2024 (CNNIC)—increases implicit buyer power by widening reputational and refund risk for developers. Yuexiu Property (HKEX: 0123) leverages its property management arm to differentiate service and accelerate rectification, lowering refund and penalty exposure. Faster fixes reduce contract breach claims and negative online virality.

- Warranty focus: faster rectification lowers refund/penalty risk

- Social amplification: ~1.05 billion mobile users in 2024

- Differentiator: Yuexiu’s in-house management improves response speed

Corporate buyers and SOEs

Corporate buyers and SOEs buy industrial and office blocks with strong bargaining power, often extracting meaningful discounts in exchange for large, certain take-ups; Yuexiu mitigates this by bundling assets across its portfolio to preserve pricing. The group structures deals with staged payments and sale-leaseback options to balance price concessions against financing certainty for sellers. Counterparty credibility often trumps headline price in negotiations, enabling Yuexiu to protect margins while closing large transactions.

- Bulk buyers: high negotiation leverage

- Yuexiu tactic: portfolio bundling to retain value

- Deal terms: structured payments, sale-leasebacks

- Outcome: trade-off between price and take-up certainty

Urban income ~3% increases price bargaining; operators bundle as mobile users hit 1.05bn

Customer bargaining rose in 2024 as urban disposable income growth slowed to ~3%, boosting price sensitivity; widespread discounting increased leverage. Anchor tenants and bulk buyers extract concessions but Yuexiu offsets via mixed-use synergies, portfolio bundling and in-house property management. Digital channels (1.05 billion mobile users in 2024) magnify reputational risk.

| Metric | 2024 | Impact |

|---|---|---|

| Urban disposable income growth | ~3% | Higher price sensitivity |

| Mobile users | 1.05bn | Amplified reputational risk |

Same Document Delivered

Yuexiu Property Porter's Five Forces Analysis

This preview is the exact Porter’s Five Forces analysis of Yuexiu Property you’ll receive—no placeholders or samples. The full document is professionally formatted, comprehensive, and ready for immediate download upon purchase. What you see here is precisely the deliverable available to you instantly after payment.

Description

Don't Miss the Bigger Picture

Yuexiu Property faces moderate buyer power, intense developer rivalry, and location-driven supplier constraints that shape its margins and growth choices.

Regulatory shifts and urbanization trends heighten entry barriers yet create niche opportunities in mixed-use and affordable housing segments.

Substitutes and financing risk remain watchpoints that could compress returns if macro conditions worsen.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Yuexiu Property’s competitive dynamics and strategic implications in depth.

Suppliers Bargaining Power

Fragmented construction inputs

China's building-materials sector is highly fragmented despite scale—national cement output was about 2.18 billion tonnes in 2023 and crude steel production ~1.03 billion tonnes, diluting individual supplier leverage and enabling Yuexiu to multi-source cement, steel and fittings across provinces. Long-term framework contracts help stabilize cost and quality, while switching costs exist but remain manageable due to industry standardization and regional supplier depth.

Land as a strategic supplier

Primary urban land in China is state-owned and effectively 100% controlled by local governments, creating quasi-monopoly power over supply; auction and tender formats account for the lion’s share of transfers (historically exceeding 90%), driving price discovery and access. Yuexiu’s SOE parentage (Yuexiu Group) and municipal ties in Guangzhou mitigate bidding pressure and financing constraints. Nonetheless, prime central-city parcels remain scarce and command significant premiums, pressuring margins and land-cost intensity.

Specialized services dependence

Specialized design institutes, MEP engineers and façade specialists can exert significant bargaining power over Yuexiu Property (HKEX: 0123) on complex projects, because technical IP and capacity constraints materially raise switching costs. Yuexiu offsets this by building in-house MEP/façade capabilities and maintaining preferred-vendor rosters. Pipeline visibility as a major Guangdong developer helps secure priority terms from constrained suppliers.

Financing as a supply input

Capital providers and state banks shape Yuexiu Property project cadence and financing cost; China’s 1-year LPR stood at 3.45% in 2024, anchoring onshore lending pricing while regulatory curbs boost the leverage of approved lenders. Yuexiu’s investment-grade SOE ties typically secure lower borrowing spreads versus private peers, but credit cycles in 2024 showed abrupt tightening risks that can raise marginal funding costs quickly.

- State banks: dominant project financier

- 1y LPR 2024: 3.45%

- SOE status: lower spreads vs peers

- Credit cycles: sudden tightening risk

Property management ecosystems

Where third-party O&M is used, scale PMCs push standardized fee schedules, limiting supplier markup; in 2024 Yuexiu’s in-house property management arm reduces external dependency and bargaining leverage of vendors.

Cross-selling and bundled services across Yuexiu’s portfolio strengthen negotiating position, while service-quality SLAs tie payments to KPIs to keep costs and outcomes aligned.

- 2024: in-house PM reduces supplier dependency

- Standardized PMC fees constrain vendor margins

- Bundled services improve procurement leverage

- SLAs align cost with service KPIs

Fragmented materials, auctioned land scarcity, lender pressure 3.45%

Fragmented building-materials supply (cement 2.18bn t, crude steel 1.03bn t in 2023) limits single-supplier leverage and enables multi-sourcing for Yuexiu.

Primary land is state-owned and auction-dominated; Yuexiu’s SOE parentage eases land access though prime urban plots remain scarce and costly.

Specialized contractors and lenders (1y LPR 2024: 3.45%) can squeeze margins, but in-house MEP/façade and PM capabilities reduce external supplier power.

| Metric | Value |

|---|---|

| Cement output 2023 | 2.18bn t |

| Crude steel 2023 | 1.03bn t |

| 1y LPR 2024 | 3.45% |

What is included in the product

Tailored Porter's Five Forces analysis for Yuexiu Property uncovering competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and strategic implications for pricing, profitability and market positioning—fully editable for integration into investor reports, strategy decks, or academic work.

A concise one-sheet Porter’s Five Forces summary for Yuexiu Property—ideal for quick investment or strategic decisions. Customize pressure levels by region, regulation or market data to reflect evolving risks and opportunities.

Customers Bargaining Power

Price-sensitive homebuyers

Households face affordability constraints as urban disposable income growth slowed to about 3% in 2024, boosting price sensitivity; widespread discounting and promotions have become common, increasing buyer leverage. Yuexiu’s strong brand and a delivery track record in tier-1/2 cities lets it sustain a premium, yet sentiment still swings quickly on macro headlines and policy shifts.

Institutional commercial tenants

Anchor tenants and MNCs wield strong bargaining power, routinely securing rent-free periods and fit-out subsidies during negotiations. Vacancy risk in emerging CBDs in 2024 heightened tenant leverage, forcing landlords to offer deeper concessions. Yuexiu leverages mixed-use synergies—retail, hotel and office—to attract and retain anchors, while longer lease terms smooth cash flows yet lock in those concessions.

Develop-to-sell intermediaries

Channel agents and online platforms materially shape sales velocity for Yuexiu, with agent commissions in China typically around 1–3% giving intermediaries leverage in weak markets; Yuexiu offsets this by balancing direct and channel sales to control SG&A and distribution costs, while ramping digital lead-generation to cut dependence on high-commission channels.

After-sales expectations

Buyers demand strong warranties and rapid defect remediation, and social media amplification—China had about 1.05 billion mobile internet users in 2024 (CNNIC)—increases implicit buyer power by widening reputational and refund risk for developers. Yuexiu Property (HKEX: 0123) leverages its property management arm to differentiate service and accelerate rectification, lowering refund and penalty exposure. Faster fixes reduce contract breach claims and negative online virality.

- Warranty focus: faster rectification lowers refund/penalty risk

- Social amplification: ~1.05 billion mobile users in 2024

- Differentiator: Yuexiu’s in-house management improves response speed

Corporate buyers and SOEs

Corporate buyers and SOEs buy industrial and office blocks with strong bargaining power, often extracting meaningful discounts in exchange for large, certain take-ups; Yuexiu mitigates this by bundling assets across its portfolio to preserve pricing. The group structures deals with staged payments and sale-leaseback options to balance price concessions against financing certainty for sellers. Counterparty credibility often trumps headline price in negotiations, enabling Yuexiu to protect margins while closing large transactions.

- Bulk buyers: high negotiation leverage

- Yuexiu tactic: portfolio bundling to retain value

- Deal terms: structured payments, sale-leasebacks

- Outcome: trade-off between price and take-up certainty

Urban income ~3% increases price bargaining; operators bundle as mobile users hit 1.05bn

Customer bargaining rose in 2024 as urban disposable income growth slowed to ~3%, boosting price sensitivity; widespread discounting increased leverage. Anchor tenants and bulk buyers extract concessions but Yuexiu offsets via mixed-use synergies, portfolio bundling and in-house property management. Digital channels (1.05 billion mobile users in 2024) magnify reputational risk.

| Metric | 2024 | Impact |

|---|---|---|

| Urban disposable income growth | ~3% | Higher price sensitivity |

| Mobile users | 1.05bn | Amplified reputational risk |

Same Document Delivered

Yuexiu Property Porter's Five Forces Analysis

This preview is the exact Porter’s Five Forces analysis of Yuexiu Property you’ll receive—no placeholders or samples. The full document is professionally formatted, comprehensive, and ready for immediate download upon purchase. What you see here is precisely the deliverable available to you instantly after payment.