Yue Yuen PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our Yue Yuen PESTLE Analysis—three to five concise insights reveal how regulatory shifts, global supply chains, and sustainability trends shape the company’s outlook. Ideal for investors and strategists, this brief highlights risk hotspots and growth levers you can act on today. Purchase the full report to access detailed, ready-to-use findings and slide-ready charts for immediate impact.

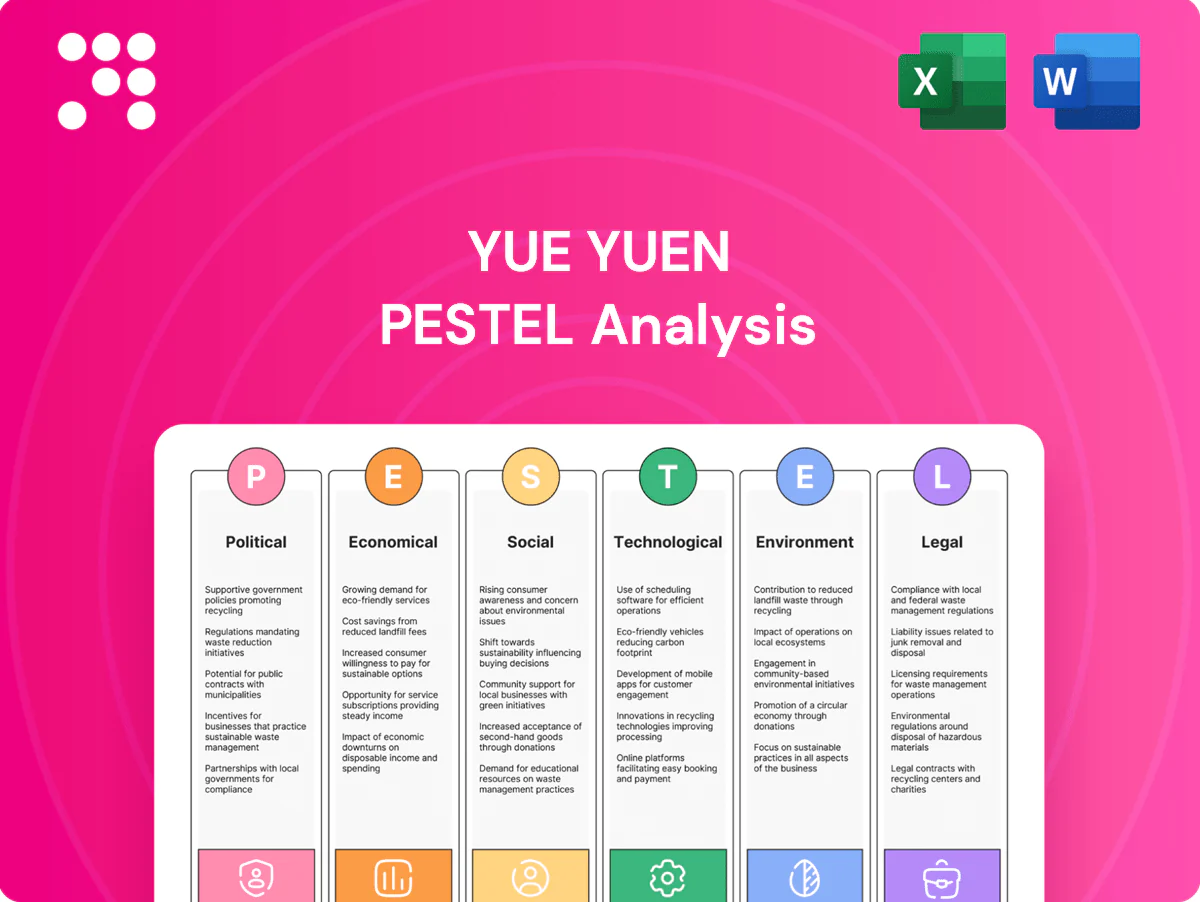

Political factors

Geopolitics and trade

US-China tensions and Section 301 tariffs, which cover roughly $360 billion of Chinese goods, continue to reshape OEM orders, tariffs and routing choices for footwear manufacturers.

Yue Yuen’s large plant footprint in Vietnam, Indonesia and China hedges direct tariff exposure but raises coordination and logistics complexity across suppliers and customers.

Preferential deals like RCEP (in force since 1 Jan 2022) and ASEAN FTAs can cut duty costs and influence plant allocation, while persistent brand de-risking favors diversified sourcing partners.

Industrial policy shifts

Shifts in industrial policy—eg local tax breaks, export rebates and infrastructure grants in ASEAN—can lower unit costs and improve Yue Yuen’s site economics, especially as RCEP now covers ~30% of global GDP and eases regional rules of origin. Subsidy rollbacks or tighter localization mandates can compress margins and raise capital costs. Government support for upstream material clusters shortens lead times and stabilizes input prices. Policy predictability remains a decisive site-selection criterion.

Labor politics

Minimum wage setting and rising labor activism in Vietnam, Indonesia and China—with regional minimums rising roughly 5–10% in 2024—pressure Yue Yuen’s cost base and continuity. Election-driven policy shifts can accelerate wage hikes or change union leverage, affecting manufacturing margins. Maintaining stable labor relations is crucial to meet strict brand delivery windows and avoid costly disruptions. Workforce upskilling and productivity programs can reduce unit labor cost and soften wage pressure.

Cross-border logistics governance

Cross-border logistics governance affects Yue Yuen: Shanghai (47.5M TEU 2023) and Ningbo-Zhoushan congestion and customs rules reshape cycle times; sanctions on rubber/leather inputs have caused episodic component shortages in 2023–24. Customs modernization (single window, AEO) has cut clearance times up to 40% and can lower working capital tied in transit by ~20%.

- Port efficiency: quay productivity, berth wait times

- Customs: single window/AEO → -40% clearance

- Sanctions: supply shocks for inputs

- Political stability: critical for on-time shipments

Mainland China retail policy

Mainland China retail policy directly shapes Pou Sheng’s store licensing, openings and marketing; disruptions from local COVID-style contingency measures can quickly cut foot traffic and weekly store sales. Tax and mandatory e-invoicing rollouts have increased back-office processing costs and tightened promotion mechanics, while PIPL and data-localization rules (post-2021) constrain omnichannel customer data flows. China retail sales were RMB 45.3 trillion in 2023, underscoring scale and regulatory sensitivity.

- Licensing/store approvals impact expansion

- Contingency measures alter footfall and sales

- E-invoicing/tax rules raise compliance costs

- Data localization/PIPL limits cross-border omnichannel data

Tariff shocks reroute OEM supply chains as RCEP, ASEAN offsets meet wage and port pressures

Geopolitical tensions and Section 301 tariffs reshape OEM routing; Yue Yuen’s China/Indonesia/Vietnam footprint hedges tariffs but raises coordination costs. Preferential FTAs (RCEP since 2022 ~30% global GDP) and ASEAN incentives cut duties; wage pressures (Vietnam/Indonesia/China +5–10% in 2024) and labor activism raise unit costs. Customs AEO/-40% clearance and port bottlenecks (Shanghai 47.5M TEU 2023) affect lead times.

| Indicator | Value |

|---|---|

| RCEP coverage | ~30% global GDP |

| Shanghai throughput 2023 | 47.5M TEU |

| China retail 2023 | RMB 45.3T |

| Wage rise 2024 | +5–10% |

| Customs AEO | -40% clearance |

What is included in the product

Explores how external macro-environmental factors uniquely affect Yue Yuen across Political, Economic, Social, Technological, Environmental and Legal dimensions, offering data-backed subpoints, forward-looking insights and actionable implications tailored to its region and industry to support executives, consultants and investors.

Concise, visually segmented Yue Yuen PESTLE summary for quick referencing in meetings or presentations, editable for regional or business-line notes and easily dropped into PowerPoints. Ideal for aligning teams, supporting external risk discussions, and sharing across devices for on-the-go reviews.

Economic factors

Global demand cycles

Footwear orders closely follow consumer discretionary cycles in the US, EU and China, with the global footwear market valued at about US$365 billion in 2023 (Statista), so demand swings in these regions materially affect OEM volumes. Inventory corrections by major brands have historically caused sharp order volatility and short-term cancellations. Recovery phases favor suppliers with flexible capacity and fast turn times, while longer booking visibility reduces utilization and margin risk for large OEMs.

FX and cost inflation

USD strength versus CNY (~7.25), VND (~24,000/US$) and IDR (~15,200/US$) magnifies conversion effects on Yue Yuen’s dollar-linked revenues and local-cost base. Wage inflation in Vietnam/Indonesia ran about 6–8% YoY into 2024, pressuring margins unless productivity rises. Raw materials (natural rubber up ~20% in 2024, higher EVA/PU and textile costs) and Brent (~85/bbl) drive COGS volatility. Hedging and multi-year supplier contracts are used to smooth swings.

China consumer health

Pou Sheng comps hinge on employment, income and consumer sentiment in Tier 1–3 cities, with urban surveyed unemployment around 5.2% in 2024 affecting footfall and spending. Promotional intensity across brands compresses gross margins and slows sell-through. E-commerce penetration (~50% of retail in 2024) shifts product mix and raises fulfillment costs. Store rationalization and franchise models have been used to stabilize profitability.

Freight and lead times

Red Sea reroutes since Nov 2023 have forced longer sailings (adding ~10–14 days) and tightened ocean capacity, lifting landed costs and reducing delivery reliability; nearshoring by brands increases competition for Yue Yuen but creates JV/manufacturing relocation opportunities. Improved S&OP can cut expedite fees (roughly 1–3% of COGS) and markdown risk, while higher buffer stocks raise inventory days and working capital needs.

- Reroutes: +10–14 days

- Expedite fees: ~1–3% of COGS

- Nearshoring: JV opportunities

- Buffer stocks: ↑ inventory days → ↑ working capital

Capital costs and investment

Interest rates (US Fed funds ~5.25–5.50% in 2024–25; China 1Y LPR 3.65%) raise financing costs and can delay Yue Yuen capex for automation and logistics upgrades, while tighter credit reduces downstream retailers’ purchasing power. ROIC depends on utilization and the automated vs manual line mix; automation raises upfront capex but can improve gross margins if utilization >80%. Government-backed financing or tax incentives (site-level subsidies) can cut effective capex and tilt site economics.

- Interest-rate pressure: higher borrowing costs

- Retail credit squeeze: lower order volumes

- ROIC hinge: utilization >80% favors automation

- State financing: lowers WACC, improves NPV

Tariff shocks reroute OEM supply chains as RCEP, ASEAN offsets meet wage and port pressures

Demand tied to US/EU/China cycles (global footwear US$365bn 2023) creates order volatility; recovery favors flexible plants. FX (USD/CNY~7.25; VND~24,000; IDR~15,200), wage inflation 6–8% and raw materials (rubber +20% 2024; Brent ~US$85/bbl) pressure margins. Fed funds 5.25–5.50% and China 1Y LPR 3.65% raise financing costs; e‑commerce ~50% of retail shifts mix and costs.

| Metric | Value |

|---|---|

| Global market (2023) | US$365bn |

| USD/CNY | ~7.25 |

| Wage inflation (VN/ID) | 6–8% |

| Rubber (2024) | +20% |

| Fed funds | 5.25–5.50% |

Full Version Awaits

Yue Yuen PESTLE Analysis

The Yue Yuen PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It contains comprehensive political, economic, social, technological, legal, and environmental insights specific to Yue Yuen. No placeholders or teasers—this is the final file available for instant download upon payment.

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our Yue Yuen PESTLE Analysis—three to five concise insights reveal how regulatory shifts, global supply chains, and sustainability trends shape the company’s outlook. Ideal for investors and strategists, this brief highlights risk hotspots and growth levers you can act on today. Purchase the full report to access detailed, ready-to-use findings and slide-ready charts for immediate impact.

Political factors

Geopolitics and trade

US-China tensions and Section 301 tariffs, which cover roughly $360 billion of Chinese goods, continue to reshape OEM orders, tariffs and routing choices for footwear manufacturers.

Yue Yuen’s large plant footprint in Vietnam, Indonesia and China hedges direct tariff exposure but raises coordination and logistics complexity across suppliers and customers.

Preferential deals like RCEP (in force since 1 Jan 2022) and ASEAN FTAs can cut duty costs and influence plant allocation, while persistent brand de-risking favors diversified sourcing partners.

Industrial policy shifts

Shifts in industrial policy—eg local tax breaks, export rebates and infrastructure grants in ASEAN—can lower unit costs and improve Yue Yuen’s site economics, especially as RCEP now covers ~30% of global GDP and eases regional rules of origin. Subsidy rollbacks or tighter localization mandates can compress margins and raise capital costs. Government support for upstream material clusters shortens lead times and stabilizes input prices. Policy predictability remains a decisive site-selection criterion.

Labor politics

Minimum wage setting and rising labor activism in Vietnam, Indonesia and China—with regional minimums rising roughly 5–10% in 2024—pressure Yue Yuen’s cost base and continuity. Election-driven policy shifts can accelerate wage hikes or change union leverage, affecting manufacturing margins. Maintaining stable labor relations is crucial to meet strict brand delivery windows and avoid costly disruptions. Workforce upskilling and productivity programs can reduce unit labor cost and soften wage pressure.

Cross-border logistics governance

Cross-border logistics governance affects Yue Yuen: Shanghai (47.5M TEU 2023) and Ningbo-Zhoushan congestion and customs rules reshape cycle times; sanctions on rubber/leather inputs have caused episodic component shortages in 2023–24. Customs modernization (single window, AEO) has cut clearance times up to 40% and can lower working capital tied in transit by ~20%.

- Port efficiency: quay productivity, berth wait times

- Customs: single window/AEO → -40% clearance

- Sanctions: supply shocks for inputs

- Political stability: critical for on-time shipments

Mainland China retail policy

Mainland China retail policy directly shapes Pou Sheng’s store licensing, openings and marketing; disruptions from local COVID-style contingency measures can quickly cut foot traffic and weekly store sales. Tax and mandatory e-invoicing rollouts have increased back-office processing costs and tightened promotion mechanics, while PIPL and data-localization rules (post-2021) constrain omnichannel customer data flows. China retail sales were RMB 45.3 trillion in 2023, underscoring scale and regulatory sensitivity.

- Licensing/store approvals impact expansion

- Contingency measures alter footfall and sales

- E-invoicing/tax rules raise compliance costs

- Data localization/PIPL limits cross-border omnichannel data

Tariff shocks reroute OEM supply chains as RCEP, ASEAN offsets meet wage and port pressures

Geopolitical tensions and Section 301 tariffs reshape OEM routing; Yue Yuen’s China/Indonesia/Vietnam footprint hedges tariffs but raises coordination costs. Preferential FTAs (RCEP since 2022 ~30% global GDP) and ASEAN incentives cut duties; wage pressures (Vietnam/Indonesia/China +5–10% in 2024) and labor activism raise unit costs. Customs AEO/-40% clearance and port bottlenecks (Shanghai 47.5M TEU 2023) affect lead times.

| Indicator | Value |

|---|---|

| RCEP coverage | ~30% global GDP |

| Shanghai throughput 2023 | 47.5M TEU |

| China retail 2023 | RMB 45.3T |

| Wage rise 2024 | +5–10% |

| Customs AEO | -40% clearance |

What is included in the product

Explores how external macro-environmental factors uniquely affect Yue Yuen across Political, Economic, Social, Technological, Environmental and Legal dimensions, offering data-backed subpoints, forward-looking insights and actionable implications tailored to its region and industry to support executives, consultants and investors.

Concise, visually segmented Yue Yuen PESTLE summary for quick referencing in meetings or presentations, editable for regional or business-line notes and easily dropped into PowerPoints. Ideal for aligning teams, supporting external risk discussions, and sharing across devices for on-the-go reviews.

Economic factors

Global demand cycles

Footwear orders closely follow consumer discretionary cycles in the US, EU and China, with the global footwear market valued at about US$365 billion in 2023 (Statista), so demand swings in these regions materially affect OEM volumes. Inventory corrections by major brands have historically caused sharp order volatility and short-term cancellations. Recovery phases favor suppliers with flexible capacity and fast turn times, while longer booking visibility reduces utilization and margin risk for large OEMs.

FX and cost inflation

USD strength versus CNY (~7.25), VND (~24,000/US$) and IDR (~15,200/US$) magnifies conversion effects on Yue Yuen’s dollar-linked revenues and local-cost base. Wage inflation in Vietnam/Indonesia ran about 6–8% YoY into 2024, pressuring margins unless productivity rises. Raw materials (natural rubber up ~20% in 2024, higher EVA/PU and textile costs) and Brent (~85/bbl) drive COGS volatility. Hedging and multi-year supplier contracts are used to smooth swings.

China consumer health

Pou Sheng comps hinge on employment, income and consumer sentiment in Tier 1–3 cities, with urban surveyed unemployment around 5.2% in 2024 affecting footfall and spending. Promotional intensity across brands compresses gross margins and slows sell-through. E-commerce penetration (~50% of retail in 2024) shifts product mix and raises fulfillment costs. Store rationalization and franchise models have been used to stabilize profitability.

Freight and lead times

Red Sea reroutes since Nov 2023 have forced longer sailings (adding ~10–14 days) and tightened ocean capacity, lifting landed costs and reducing delivery reliability; nearshoring by brands increases competition for Yue Yuen but creates JV/manufacturing relocation opportunities. Improved S&OP can cut expedite fees (roughly 1–3% of COGS) and markdown risk, while higher buffer stocks raise inventory days and working capital needs.

- Reroutes: +10–14 days

- Expedite fees: ~1–3% of COGS

- Nearshoring: JV opportunities

- Buffer stocks: ↑ inventory days → ↑ working capital

Capital costs and investment

Interest rates (US Fed funds ~5.25–5.50% in 2024–25; China 1Y LPR 3.65%) raise financing costs and can delay Yue Yuen capex for automation and logistics upgrades, while tighter credit reduces downstream retailers’ purchasing power. ROIC depends on utilization and the automated vs manual line mix; automation raises upfront capex but can improve gross margins if utilization >80%. Government-backed financing or tax incentives (site-level subsidies) can cut effective capex and tilt site economics.

- Interest-rate pressure: higher borrowing costs

- Retail credit squeeze: lower order volumes

- ROIC hinge: utilization >80% favors automation

- State financing: lowers WACC, improves NPV

Tariff shocks reroute OEM supply chains as RCEP, ASEAN offsets meet wage and port pressures

Demand tied to US/EU/China cycles (global footwear US$365bn 2023) creates order volatility; recovery favors flexible plants. FX (USD/CNY~7.25; VND~24,000; IDR~15,200), wage inflation 6–8% and raw materials (rubber +20% 2024; Brent ~US$85/bbl) pressure margins. Fed funds 5.25–5.50% and China 1Y LPR 3.65% raise financing costs; e‑commerce ~50% of retail shifts mix and costs.

| Metric | Value |

|---|---|

| Global market (2023) | US$365bn |

| USD/CNY | ~7.25 |

| Wage inflation (VN/ID) | 6–8% |

| Rubber (2024) | +20% |

| Fed funds | 5.25–5.50% |

Full Version Awaits

Yue Yuen PESTLE Analysis

The Yue Yuen PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It contains comprehensive political, economic, social, technological, legal, and environmental insights specific to Yue Yuen. No placeholders or teasers—this is the final file available for instant download upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our Yue Yuen PESTLE Analysis—three to five concise insights reveal how regulatory shifts, global supply chains, and sustainability trends shape the company’s outlook. Ideal for investors and strategists, this brief highlights risk hotspots and growth levers you can act on today. Purchase the full report to access detailed, ready-to-use findings and slide-ready charts for immediate impact.

Political factors

Geopolitics and trade

US-China tensions and Section 301 tariffs, which cover roughly $360 billion of Chinese goods, continue to reshape OEM orders, tariffs and routing choices for footwear manufacturers.

Yue Yuen’s large plant footprint in Vietnam, Indonesia and China hedges direct tariff exposure but raises coordination and logistics complexity across suppliers and customers.

Preferential deals like RCEP (in force since 1 Jan 2022) and ASEAN FTAs can cut duty costs and influence plant allocation, while persistent brand de-risking favors diversified sourcing partners.

Industrial policy shifts

Shifts in industrial policy—eg local tax breaks, export rebates and infrastructure grants in ASEAN—can lower unit costs and improve Yue Yuen’s site economics, especially as RCEP now covers ~30% of global GDP and eases regional rules of origin. Subsidy rollbacks or tighter localization mandates can compress margins and raise capital costs. Government support for upstream material clusters shortens lead times and stabilizes input prices. Policy predictability remains a decisive site-selection criterion.

Labor politics

Minimum wage setting and rising labor activism in Vietnam, Indonesia and China—with regional minimums rising roughly 5–10% in 2024—pressure Yue Yuen’s cost base and continuity. Election-driven policy shifts can accelerate wage hikes or change union leverage, affecting manufacturing margins. Maintaining stable labor relations is crucial to meet strict brand delivery windows and avoid costly disruptions. Workforce upskilling and productivity programs can reduce unit labor cost and soften wage pressure.

Cross-border logistics governance

Cross-border logistics governance affects Yue Yuen: Shanghai (47.5M TEU 2023) and Ningbo-Zhoushan congestion and customs rules reshape cycle times; sanctions on rubber/leather inputs have caused episodic component shortages in 2023–24. Customs modernization (single window, AEO) has cut clearance times up to 40% and can lower working capital tied in transit by ~20%.

- Port efficiency: quay productivity, berth wait times

- Customs: single window/AEO → -40% clearance

- Sanctions: supply shocks for inputs

- Political stability: critical for on-time shipments

Mainland China retail policy

Mainland China retail policy directly shapes Pou Sheng’s store licensing, openings and marketing; disruptions from local COVID-style contingency measures can quickly cut foot traffic and weekly store sales. Tax and mandatory e-invoicing rollouts have increased back-office processing costs and tightened promotion mechanics, while PIPL and data-localization rules (post-2021) constrain omnichannel customer data flows. China retail sales were RMB 45.3 trillion in 2023, underscoring scale and regulatory sensitivity.

- Licensing/store approvals impact expansion

- Contingency measures alter footfall and sales

- E-invoicing/tax rules raise compliance costs

- Data localization/PIPL limits cross-border omnichannel data

Tariff shocks reroute OEM supply chains as RCEP, ASEAN offsets meet wage and port pressures

Geopolitical tensions and Section 301 tariffs reshape OEM routing; Yue Yuen’s China/Indonesia/Vietnam footprint hedges tariffs but raises coordination costs. Preferential FTAs (RCEP since 2022 ~30% global GDP) and ASEAN incentives cut duties; wage pressures (Vietnam/Indonesia/China +5–10% in 2024) and labor activism raise unit costs. Customs AEO/-40% clearance and port bottlenecks (Shanghai 47.5M TEU 2023) affect lead times.

| Indicator | Value |

|---|---|

| RCEP coverage | ~30% global GDP |

| Shanghai throughput 2023 | 47.5M TEU |

| China retail 2023 | RMB 45.3T |

| Wage rise 2024 | +5–10% |

| Customs AEO | -40% clearance |

What is included in the product

Explores how external macro-environmental factors uniquely affect Yue Yuen across Political, Economic, Social, Technological, Environmental and Legal dimensions, offering data-backed subpoints, forward-looking insights and actionable implications tailored to its region and industry to support executives, consultants and investors.

Concise, visually segmented Yue Yuen PESTLE summary for quick referencing in meetings or presentations, editable for regional or business-line notes and easily dropped into PowerPoints. Ideal for aligning teams, supporting external risk discussions, and sharing across devices for on-the-go reviews.

Economic factors

Global demand cycles

Footwear orders closely follow consumer discretionary cycles in the US, EU and China, with the global footwear market valued at about US$365 billion in 2023 (Statista), so demand swings in these regions materially affect OEM volumes. Inventory corrections by major brands have historically caused sharp order volatility and short-term cancellations. Recovery phases favor suppliers with flexible capacity and fast turn times, while longer booking visibility reduces utilization and margin risk for large OEMs.

FX and cost inflation

USD strength versus CNY (~7.25), VND (~24,000/US$) and IDR (~15,200/US$) magnifies conversion effects on Yue Yuen’s dollar-linked revenues and local-cost base. Wage inflation in Vietnam/Indonesia ran about 6–8% YoY into 2024, pressuring margins unless productivity rises. Raw materials (natural rubber up ~20% in 2024, higher EVA/PU and textile costs) and Brent (~85/bbl) drive COGS volatility. Hedging and multi-year supplier contracts are used to smooth swings.

China consumer health

Pou Sheng comps hinge on employment, income and consumer sentiment in Tier 1–3 cities, with urban surveyed unemployment around 5.2% in 2024 affecting footfall and spending. Promotional intensity across brands compresses gross margins and slows sell-through. E-commerce penetration (~50% of retail in 2024) shifts product mix and raises fulfillment costs. Store rationalization and franchise models have been used to stabilize profitability.

Freight and lead times

Red Sea reroutes since Nov 2023 have forced longer sailings (adding ~10–14 days) and tightened ocean capacity, lifting landed costs and reducing delivery reliability; nearshoring by brands increases competition for Yue Yuen but creates JV/manufacturing relocation opportunities. Improved S&OP can cut expedite fees (roughly 1–3% of COGS) and markdown risk, while higher buffer stocks raise inventory days and working capital needs.

- Reroutes: +10–14 days

- Expedite fees: ~1–3% of COGS

- Nearshoring: JV opportunities

- Buffer stocks: ↑ inventory days → ↑ working capital

Capital costs and investment

Interest rates (US Fed funds ~5.25–5.50% in 2024–25; China 1Y LPR 3.65%) raise financing costs and can delay Yue Yuen capex for automation and logistics upgrades, while tighter credit reduces downstream retailers’ purchasing power. ROIC depends on utilization and the automated vs manual line mix; automation raises upfront capex but can improve gross margins if utilization >80%. Government-backed financing or tax incentives (site-level subsidies) can cut effective capex and tilt site economics.

- Interest-rate pressure: higher borrowing costs

- Retail credit squeeze: lower order volumes

- ROIC hinge: utilization >80% favors automation

- State financing: lowers WACC, improves NPV

Tariff shocks reroute OEM supply chains as RCEP, ASEAN offsets meet wage and port pressures

Demand tied to US/EU/China cycles (global footwear US$365bn 2023) creates order volatility; recovery favors flexible plants. FX (USD/CNY~7.25; VND~24,000; IDR~15,200), wage inflation 6–8% and raw materials (rubber +20% 2024; Brent ~US$85/bbl) pressure margins. Fed funds 5.25–5.50% and China 1Y LPR 3.65% raise financing costs; e‑commerce ~50% of retail shifts mix and costs.

| Metric | Value |

|---|---|

| Global market (2023) | US$365bn |

| USD/CNY | ~7.25 |

| Wage inflation (VN/ID) | 6–8% |

| Rubber (2024) | +20% |

| Fed funds | 5.25–5.50% |

Full Version Awaits

Yue Yuen PESTLE Analysis

The Yue Yuen PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It contains comprehensive political, economic, social, technological, legal, and environmental insights specific to Yue Yuen. No placeholders or teasers—this is the final file available for instant download upon payment.