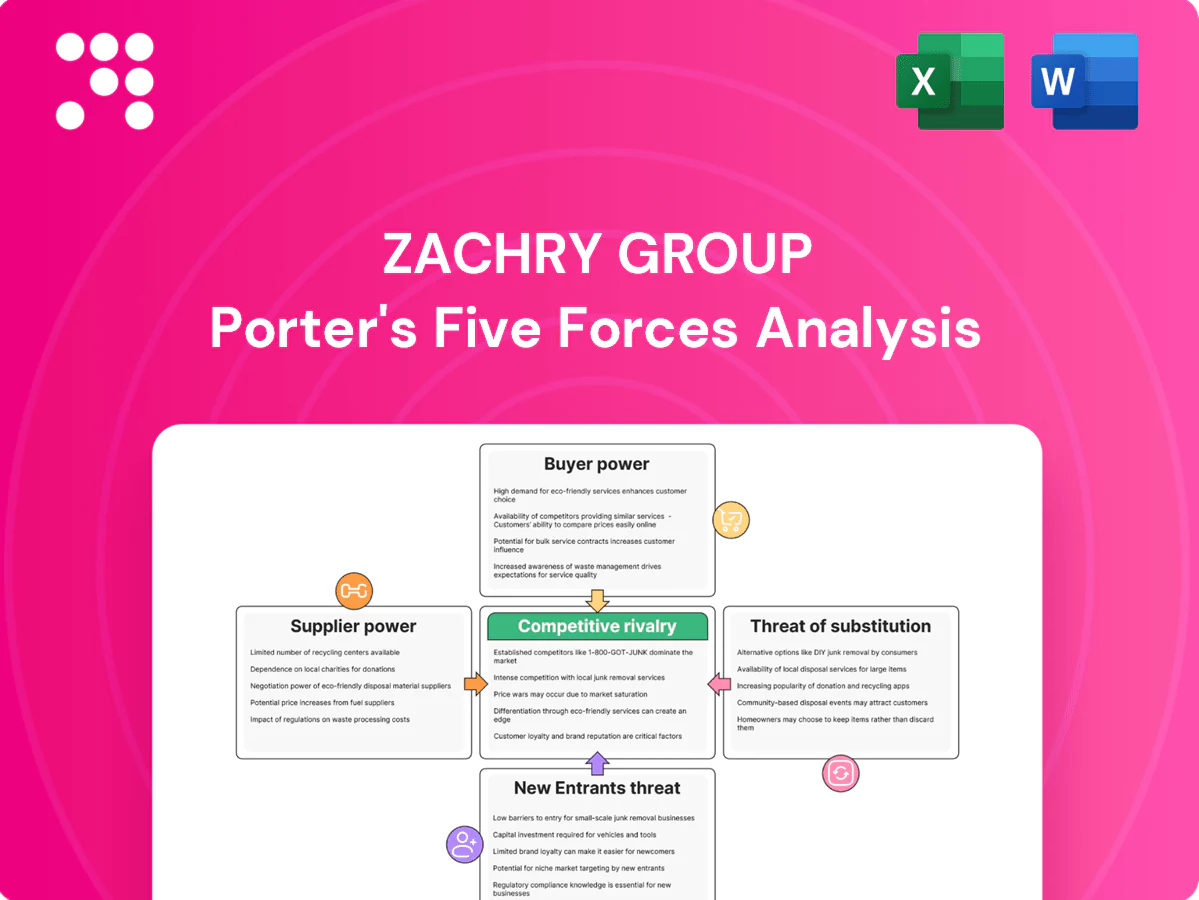

Zachry Group Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Zachry Group operates in a capital-intensive, project-driven market where supplier leverage, client concentration, and regulatory barriers shape profitability; competitive rivalry is high but long-term contracts and specialized capabilities offer advantage. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Concentrated critical inputs

Zachry depends on concentrated suppliers for steel, specialty alloys, heavy equipment and industrial OEM packages, with three primary large-turbine OEMs (GE, Siemens Energy, Mitsubishi Heavy Industries) dominating critical equipment supply. Limited alternatives for turbines, compressors, valves and controls increase supplier leverage. Long lead times of 12–24 months amplify price and schedule risk. Strict qualification and compliance further shrink the vendor pool.

Skilled craft labor and unions

Access to certified welders, pipefitters, electricians and specialty supervisors is a bottleneck in hot markets: in 2024 certified welders averaged roughly $24/hr and trade premiums commonly rose 20–50% during peak demand. Regional labor tightness and unionization (construction unionization stayed above 10% in 2024) elevate wages and restrict scheduling flexibility. Retention and training investments reduce vacancies but do not remove supplier leverage, and turnarounds/outages can briefly double day rates.

Logistics and heavy-lift dependencies

Oversized modules require scarce heavy-haul, rail, and crane capacity, with industry reports in 2024 noting up to 30% premiums for specialized lifts and heavy-haul escorts. Port congestion, permitting and escort rules add timing leverage to logistics providers—U.S. gate delays in 2024 averaged double-digit percentage increases versus 2020. Seasonal and regional constraints further compress options; contingency planning reduces but cannot fully eliminate these dependencies.

Specialty subcontractors and NDE services

Highly specialized testing, coatings, refractory and NDE services have few interchangeable providers, with qualification, safety records and owner-approved lists tightly constraining substitution; in 2024 industry commentary highlighted continued crew scarcity during peak outages. Peak outage windows amplify supplier leverage while framework agreements stabilize rates but not availability, which remains the primary constraint on Zachry’s scheduling and margins.

- Few interchangeable providers

- Owner-approved lists limit substitutes

- Peak outages boost supplier leverage

- Frameworks fix price, not availability

Input price volatility exposure

Commodity metals, fuel, and OEM equipment pricing swung materially during long project cycles, with 2024 metal and fuel volatility commonly in the 15–25% range, driving frequent supplier escalation clauses that shift cost risk to EPC contractors like Zachry.

Hedging and early procurement reduce exposure but tie up working capital and can raise financing costs; owners often resist full pass-throughs, leaving Zachry squeezed between supplier claims and client budgets.

- Supply cost volatility: 15–25% (2024)

- Escalation clauses: commonly invoked

- Mitigation trade-off: hedging vs working capital

Concentrated OEMs, scarce trades, 12–24 month lead times drive cost and schedule risk

Zachry faces high supplier leverage from concentrated OEMs and scarce specialist trades; turbine/compressor markets offer few substitutes and 12–24 month lead times. Certified welder average wage ~$24/hr in 2024 with trade premiums up 20–50% at peaks, and logistics/heavy-lift premiums reached ~30%. Commodity volatility (metals/fuel) ran 15–25% in 2024, forcing escalation clauses and hedging that tie working capital.

| Metric | 2024 Value |

|---|---|

| Lead times (critical OEM) | 12–24 months |

| Certified welder avg wage | $24/hr |

| Trade premiums (peak) | 20–50% |

| Logistics/heavy-lift premium | ~30% |

| Metals/fuel volatility | 15–25% |

What is included in the product

Tailored exclusively for Zachry Group, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, and market entry risks, while identifying disruptive substitutes and emerging threats to market share. Fully editable for use in investor materials, strategy decks, or academic projects.

A single-sheet Porter's Five Forces summary for Zachry Group that clarifies competitive pressures and eases strategic decisions—editable force levels, instant radar visualization, and clean layout ready for pitch decks or dashboards.

Customers Bargaining Power

Large, sophisticated owners

Large, sophisticated owners in energy, chemicals and power centralize procurement and in 2024 ran competitive tenders in over 80% of major capital projects, benchmarking bids against global EPCs and enforcing strict commercial terms.

Prequalification filters awards to incumbents with proven safety and quality records, shrinking the bidder pool and raising barriers for newcomers.

Negotiating leverage typically sits with buyers at award, compressing EPC margins and shifting risk onto contractors.

Project-based price sensitivity

Capex-heavy projects force aggressive bidding and compress contractor margins—industry operating margins fell to about 3% in 2024, making razor-thin bids common. Owners increasingly require schedule guarantees, liquidated damages often 0.1–0.25% per day and performance bonds typically 1–3% of contract value. Lump-sum contracts shift substantial risk downstream, and value engineering can protect price but often cannot restore lost margin.

Switching costs moderate

While mobilization and learning curves create inertia, many owners keep multi-EPC panels, making cross-project switches common though mid-project changes are rarer due to disruption risk. Strong performance by Zachry secures repeat work and blunts buyer power. Conversely, poor execution rapidly eliminates future scope as owners reallocate packages to other panel contractors.

Safety and compliance leverage

Owners now treat TRIR, compliance and quality metrics as bid gates, with many setting TRIR targets below 1.0 in 2024; deviations lead to penalties, rework or removal from preferred vendor lists, giving buyers leverage through performance scorecards and holdbacks. Continuous improvement programs and transparent reporting platforms are essential defenses to retain eligibility and pricing power.

- TRIR target: commonly <1.0 in 2024

- Consequences: penalties, rework, disqualification

- Defense: CI programs + transparent reporting

Term contracts vs spot awards

Long-term maintenance and turnaround MSAs stabilize volumes and pricing for Zachry by locking recurring work flows and margins, but 2024 industry sourcing benchmarks show frequent re-bids and KPI-linked renewals keep pricing pressure high; spot EPC awards maximize buyer bargaining power and can cut procurement costs by up to 15% in competitive cycles. Relationship capital helps but rarely offsets clear price-performance gaps.

- MSAs: stabilize recurring revenue, reduce volatility

- Re-bids/KPIs: maintain margin compression

- Spot EPC: up to 15% procurement advantage (2024 benchmarks)

- Relationships: tiebreaker, not margin saver

Buyers' leverage compresses EPC margins to ~3% as >80% of projects go to competitive tenders

Buyers hold strong leverage: >80% of major projects ran competitive tenders in 2024, compressing EPC margins to ~3% industry-wide.

Contract terms shift risk downstream: lump-sum, LDs 0.1–0.25%/day, performance bonds 1–3%, and TRIR gates commonly <1.0 in 2024.

MSAs stabilize revenue but frequent re-bids/KPI renewals and spot EPCs (up to 15% buyer savings) keep pricing pressure high.

| Metric | 2024 Value |

|---|---|

| Competitive tenders | 80%+ |

| Industry margin | ~3% |

| Spot procurement savings | Up to 15% |

Full Version Awaits

Zachry Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Zachry Group you'll receive—no mockups or placeholders. The full document is professionally formatted, comprehensive, and ready for immediate download and use upon purchase. What you see here is precisely the deliverable you’ll get, instantly accessible after payment.

A Must-Have Tool for Decision-Makers

Zachry Group operates in a capital-intensive, project-driven market where supplier leverage, client concentration, and regulatory barriers shape profitability; competitive rivalry is high but long-term contracts and specialized capabilities offer advantage. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Concentrated critical inputs

Zachry depends on concentrated suppliers for steel, specialty alloys, heavy equipment and industrial OEM packages, with three primary large-turbine OEMs (GE, Siemens Energy, Mitsubishi Heavy Industries) dominating critical equipment supply. Limited alternatives for turbines, compressors, valves and controls increase supplier leverage. Long lead times of 12–24 months amplify price and schedule risk. Strict qualification and compliance further shrink the vendor pool.

Skilled craft labor and unions

Access to certified welders, pipefitters, electricians and specialty supervisors is a bottleneck in hot markets: in 2024 certified welders averaged roughly $24/hr and trade premiums commonly rose 20–50% during peak demand. Regional labor tightness and unionization (construction unionization stayed above 10% in 2024) elevate wages and restrict scheduling flexibility. Retention and training investments reduce vacancies but do not remove supplier leverage, and turnarounds/outages can briefly double day rates.

Logistics and heavy-lift dependencies

Oversized modules require scarce heavy-haul, rail, and crane capacity, with industry reports in 2024 noting up to 30% premiums for specialized lifts and heavy-haul escorts. Port congestion, permitting and escort rules add timing leverage to logistics providers—U.S. gate delays in 2024 averaged double-digit percentage increases versus 2020. Seasonal and regional constraints further compress options; contingency planning reduces but cannot fully eliminate these dependencies.

Specialty subcontractors and NDE services

Highly specialized testing, coatings, refractory and NDE services have few interchangeable providers, with qualification, safety records and owner-approved lists tightly constraining substitution; in 2024 industry commentary highlighted continued crew scarcity during peak outages. Peak outage windows amplify supplier leverage while framework agreements stabilize rates but not availability, which remains the primary constraint on Zachry’s scheduling and margins.

- Few interchangeable providers

- Owner-approved lists limit substitutes

- Peak outages boost supplier leverage

- Frameworks fix price, not availability

Input price volatility exposure

Commodity metals, fuel, and OEM equipment pricing swung materially during long project cycles, with 2024 metal and fuel volatility commonly in the 15–25% range, driving frequent supplier escalation clauses that shift cost risk to EPC contractors like Zachry.

Hedging and early procurement reduce exposure but tie up working capital and can raise financing costs; owners often resist full pass-throughs, leaving Zachry squeezed between supplier claims and client budgets.

- Supply cost volatility: 15–25% (2024)

- Escalation clauses: commonly invoked

- Mitigation trade-off: hedging vs working capital

Concentrated OEMs, scarce trades, 12–24 month lead times drive cost and schedule risk

Zachry faces high supplier leverage from concentrated OEMs and scarce specialist trades; turbine/compressor markets offer few substitutes and 12–24 month lead times. Certified welder average wage ~$24/hr in 2024 with trade premiums up 20–50% at peaks, and logistics/heavy-lift premiums reached ~30%. Commodity volatility (metals/fuel) ran 15–25% in 2024, forcing escalation clauses and hedging that tie working capital.

| Metric | 2024 Value |

|---|---|

| Lead times (critical OEM) | 12–24 months |

| Certified welder avg wage | $24/hr |

| Trade premiums (peak) | 20–50% |

| Logistics/heavy-lift premium | ~30% |

| Metals/fuel volatility | 15–25% |

What is included in the product

Tailored exclusively for Zachry Group, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, and market entry risks, while identifying disruptive substitutes and emerging threats to market share. Fully editable for use in investor materials, strategy decks, or academic projects.

A single-sheet Porter's Five Forces summary for Zachry Group that clarifies competitive pressures and eases strategic decisions—editable force levels, instant radar visualization, and clean layout ready for pitch decks or dashboards.

Customers Bargaining Power

Large, sophisticated owners

Large, sophisticated owners in energy, chemicals and power centralize procurement and in 2024 ran competitive tenders in over 80% of major capital projects, benchmarking bids against global EPCs and enforcing strict commercial terms.

Prequalification filters awards to incumbents with proven safety and quality records, shrinking the bidder pool and raising barriers for newcomers.

Negotiating leverage typically sits with buyers at award, compressing EPC margins and shifting risk onto contractors.

Project-based price sensitivity

Capex-heavy projects force aggressive bidding and compress contractor margins—industry operating margins fell to about 3% in 2024, making razor-thin bids common. Owners increasingly require schedule guarantees, liquidated damages often 0.1–0.25% per day and performance bonds typically 1–3% of contract value. Lump-sum contracts shift substantial risk downstream, and value engineering can protect price but often cannot restore lost margin.

Switching costs moderate

While mobilization and learning curves create inertia, many owners keep multi-EPC panels, making cross-project switches common though mid-project changes are rarer due to disruption risk. Strong performance by Zachry secures repeat work and blunts buyer power. Conversely, poor execution rapidly eliminates future scope as owners reallocate packages to other panel contractors.

Safety and compliance leverage

Owners now treat TRIR, compliance and quality metrics as bid gates, with many setting TRIR targets below 1.0 in 2024; deviations lead to penalties, rework or removal from preferred vendor lists, giving buyers leverage through performance scorecards and holdbacks. Continuous improvement programs and transparent reporting platforms are essential defenses to retain eligibility and pricing power.

- TRIR target: commonly <1.0 in 2024

- Consequences: penalties, rework, disqualification

- Defense: CI programs + transparent reporting

Term contracts vs spot awards

Long-term maintenance and turnaround MSAs stabilize volumes and pricing for Zachry by locking recurring work flows and margins, but 2024 industry sourcing benchmarks show frequent re-bids and KPI-linked renewals keep pricing pressure high; spot EPC awards maximize buyer bargaining power and can cut procurement costs by up to 15% in competitive cycles. Relationship capital helps but rarely offsets clear price-performance gaps.

- MSAs: stabilize recurring revenue, reduce volatility

- Re-bids/KPIs: maintain margin compression

- Spot EPC: up to 15% procurement advantage (2024 benchmarks)

- Relationships: tiebreaker, not margin saver

Buyers' leverage compresses EPC margins to ~3% as >80% of projects go to competitive tenders

Buyers hold strong leverage: >80% of major projects ran competitive tenders in 2024, compressing EPC margins to ~3% industry-wide.

Contract terms shift risk downstream: lump-sum, LDs 0.1–0.25%/day, performance bonds 1–3%, and TRIR gates commonly <1.0 in 2024.

MSAs stabilize revenue but frequent re-bids/KPI renewals and spot EPCs (up to 15% buyer savings) keep pricing pressure high.

| Metric | 2024 Value |

|---|---|

| Competitive tenders | 80%+ |

| Industry margin | ~3% |

| Spot procurement savings | Up to 15% |

Full Version Awaits

Zachry Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Zachry Group you'll receive—no mockups or placeholders. The full document is professionally formatted, comprehensive, and ready for immediate download and use upon purchase. What you see here is precisely the deliverable you’ll get, instantly accessible after payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Zachry Group operates in a capital-intensive, project-driven market where supplier leverage, client concentration, and regulatory barriers shape profitability; competitive rivalry is high but long-term contracts and specialized capabilities offer advantage. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Concentrated critical inputs

Zachry depends on concentrated suppliers for steel, specialty alloys, heavy equipment and industrial OEM packages, with three primary large-turbine OEMs (GE, Siemens Energy, Mitsubishi Heavy Industries) dominating critical equipment supply. Limited alternatives for turbines, compressors, valves and controls increase supplier leverage. Long lead times of 12–24 months amplify price and schedule risk. Strict qualification and compliance further shrink the vendor pool.

Skilled craft labor and unions

Access to certified welders, pipefitters, electricians and specialty supervisors is a bottleneck in hot markets: in 2024 certified welders averaged roughly $24/hr and trade premiums commonly rose 20–50% during peak demand. Regional labor tightness and unionization (construction unionization stayed above 10% in 2024) elevate wages and restrict scheduling flexibility. Retention and training investments reduce vacancies but do not remove supplier leverage, and turnarounds/outages can briefly double day rates.

Logistics and heavy-lift dependencies

Oversized modules require scarce heavy-haul, rail, and crane capacity, with industry reports in 2024 noting up to 30% premiums for specialized lifts and heavy-haul escorts. Port congestion, permitting and escort rules add timing leverage to logistics providers—U.S. gate delays in 2024 averaged double-digit percentage increases versus 2020. Seasonal and regional constraints further compress options; contingency planning reduces but cannot fully eliminate these dependencies.

Specialty subcontractors and NDE services

Highly specialized testing, coatings, refractory and NDE services have few interchangeable providers, with qualification, safety records and owner-approved lists tightly constraining substitution; in 2024 industry commentary highlighted continued crew scarcity during peak outages. Peak outage windows amplify supplier leverage while framework agreements stabilize rates but not availability, which remains the primary constraint on Zachry’s scheduling and margins.

- Few interchangeable providers

- Owner-approved lists limit substitutes

- Peak outages boost supplier leverage

- Frameworks fix price, not availability

Input price volatility exposure

Commodity metals, fuel, and OEM equipment pricing swung materially during long project cycles, with 2024 metal and fuel volatility commonly in the 15–25% range, driving frequent supplier escalation clauses that shift cost risk to EPC contractors like Zachry.

Hedging and early procurement reduce exposure but tie up working capital and can raise financing costs; owners often resist full pass-throughs, leaving Zachry squeezed between supplier claims and client budgets.

- Supply cost volatility: 15–25% (2024)

- Escalation clauses: commonly invoked

- Mitigation trade-off: hedging vs working capital

Concentrated OEMs, scarce trades, 12–24 month lead times drive cost and schedule risk

Zachry faces high supplier leverage from concentrated OEMs and scarce specialist trades; turbine/compressor markets offer few substitutes and 12–24 month lead times. Certified welder average wage ~$24/hr in 2024 with trade premiums up 20–50% at peaks, and logistics/heavy-lift premiums reached ~30%. Commodity volatility (metals/fuel) ran 15–25% in 2024, forcing escalation clauses and hedging that tie working capital.

| Metric | 2024 Value |

|---|---|

| Lead times (critical OEM) | 12–24 months |

| Certified welder avg wage | $24/hr |

| Trade premiums (peak) | 20–50% |

| Logistics/heavy-lift premium | ~30% |

| Metals/fuel volatility | 15–25% |

What is included in the product

Tailored exclusively for Zachry Group, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, and market entry risks, while identifying disruptive substitutes and emerging threats to market share. Fully editable for use in investor materials, strategy decks, or academic projects.

A single-sheet Porter's Five Forces summary for Zachry Group that clarifies competitive pressures and eases strategic decisions—editable force levels, instant radar visualization, and clean layout ready for pitch decks or dashboards.

Customers Bargaining Power

Large, sophisticated owners

Large, sophisticated owners in energy, chemicals and power centralize procurement and in 2024 ran competitive tenders in over 80% of major capital projects, benchmarking bids against global EPCs and enforcing strict commercial terms.

Prequalification filters awards to incumbents with proven safety and quality records, shrinking the bidder pool and raising barriers for newcomers.

Negotiating leverage typically sits with buyers at award, compressing EPC margins and shifting risk onto contractors.

Project-based price sensitivity

Capex-heavy projects force aggressive bidding and compress contractor margins—industry operating margins fell to about 3% in 2024, making razor-thin bids common. Owners increasingly require schedule guarantees, liquidated damages often 0.1–0.25% per day and performance bonds typically 1–3% of contract value. Lump-sum contracts shift substantial risk downstream, and value engineering can protect price but often cannot restore lost margin.

Switching costs moderate

While mobilization and learning curves create inertia, many owners keep multi-EPC panels, making cross-project switches common though mid-project changes are rarer due to disruption risk. Strong performance by Zachry secures repeat work and blunts buyer power. Conversely, poor execution rapidly eliminates future scope as owners reallocate packages to other panel contractors.

Safety and compliance leverage

Owners now treat TRIR, compliance and quality metrics as bid gates, with many setting TRIR targets below 1.0 in 2024; deviations lead to penalties, rework or removal from preferred vendor lists, giving buyers leverage through performance scorecards and holdbacks. Continuous improvement programs and transparent reporting platforms are essential defenses to retain eligibility and pricing power.

- TRIR target: commonly <1.0 in 2024

- Consequences: penalties, rework, disqualification

- Defense: CI programs + transparent reporting

Term contracts vs spot awards

Long-term maintenance and turnaround MSAs stabilize volumes and pricing for Zachry by locking recurring work flows and margins, but 2024 industry sourcing benchmarks show frequent re-bids and KPI-linked renewals keep pricing pressure high; spot EPC awards maximize buyer bargaining power and can cut procurement costs by up to 15% in competitive cycles. Relationship capital helps but rarely offsets clear price-performance gaps.

- MSAs: stabilize recurring revenue, reduce volatility

- Re-bids/KPIs: maintain margin compression

- Spot EPC: up to 15% procurement advantage (2024 benchmarks)

- Relationships: tiebreaker, not margin saver

Buyers' leverage compresses EPC margins to ~3% as >80% of projects go to competitive tenders

Buyers hold strong leverage: >80% of major projects ran competitive tenders in 2024, compressing EPC margins to ~3% industry-wide.

Contract terms shift risk downstream: lump-sum, LDs 0.1–0.25%/day, performance bonds 1–3%, and TRIR gates commonly <1.0 in 2024.

MSAs stabilize revenue but frequent re-bids/KPI renewals and spot EPCs (up to 15% buyer savings) keep pricing pressure high.

| Metric | 2024 Value |

|---|---|

| Competitive tenders | 80%+ |

| Industry margin | ~3% |

| Spot procurement savings | Up to 15% |

Full Version Awaits

Zachry Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Zachry Group you'll receive—no mockups or placeholders. The full document is professionally formatted, comprehensive, and ready for immediate download and use upon purchase. What you see here is precisely the deliverable you’ll get, instantly accessible after payment.