Wuchan Zhongda Group Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Wuchan Zhongda Group faces intense rivalry and moderate supplier leverage amid capital-heavy port operations, while buyer switching costs and substitute logistics channels gradually shape pricing power. Regulatory and infrastructure barriers temper new entrants but technological shifts raise strategic risk. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Wuchan Zhongda Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated upstream resources

Wuchan sources energy, metals and chemicals from a relatively concentrated set of global and domestic producers, with OPEC+ and a handful of mining majors controlling roughly 40% of oil output and a large share of key base metals in 2024. Resource owners — oil majors, mining giants, petrochemical complexes and state entities — can exert pricing and allocation power, raising switching costs in tight markets. Wuchan mitigates exposure through portfolio sourcing and long-term offtake contracts covering multi-year volumes.

Commodity cyclicality drives leverage

Commodity cyclicality drives supplier leverage: in bull phases suppliers tighten commercial terms and shorten payment windows while in downturns their bargaining power falls as they chase volume and liquidity. China remained the world’s largest steel producer in 2024, accounting for over half of global crude steel, reinforcing suppliers’ cyclical influence. Wuchan’s counter‑cyclical buying and inventory financing smooths cash flow, and its scale supports take‑or‑pay and prepay contracts that secure priority supply.

Logistics chokepoints and port capacity

Bulk commodities rely on constrained rail links, port berths and storage where capacity owners can dictate throughput and fees; seasonal congestion and intensified regulatory inspections further amplify supplier leverage. Wuchan Zhongda’s integrated logistics network and long-term contracted capacities reduce its exposure to spot constraints. Multiple diversified corridors provide resilient back-up routing, lowering single-node dependency.

Spec quality and certification constraints

Industrial buyers demand specific grades and certifications (eg national GB, ISO, API), restricting acceptable upstream sources and narrowing supplier pools for niche chemicals and specialty metals; Wuchan manages this through vetted vendor rosters to preserve procurement optionality. Technical teams evaluate and enable qualified substitutions where standards and safety allow, reducing single-source risks.

State linkages and policy priorities

As a large SOE, Wuchan Zhongda benefits from alignment with domestic producers and policy-driven allocations, which reduce supply disruption risk but can raise supplier leverage when export controls, quotas or price floors are imposed. Strong government relationships allow the group to negotiate volumes and allocations during regulatory shifts, while improved policy visibility in 2024 aided planning and hedging across procurement cycles.

- State alignment reduces short-term disruption

- Export controls and quotas elevate supplier power

- Government ties enable negotiated volumes

- 2024 policy visibility improved hedging

Energy and metals concentrated: ≈40% OPEC+ oil, >50% China steel

Supplier power is high for energy and key metals: OPEC+ controlled roughly 40% of oil output in 2024 and China accounted for >50% of global crude steel, concentrating pricing and allocation leverage. Wuchan offsets this via portfolio sourcing, long‑term offtake and integrated logistics that lower spot exposure and routing risk. Certification requirements and state alignment further constrain supplier pools but provide preferential allocations.

| Metric | 2024 value | Implication |

|---|---|---|

| OPEC+ oil share | ≈40% | High price/allocation leverage |

| China crude steel | >50% | Strong cyclical supplier influence |

| Wuchan mitigation | Long‑term contracts + logistics | Reduced spot risk |

What is included in the product

Tailored Porter’s Five Forces analysis for Wuchan Zhongda Group uncovering competitive intensity, supplier and buyer bargaining power, threat of new entrants and substitutes, and industry-specific barriers that shape pricing, margins, and strategic positioning.

A concise, one-sheet Porter's Five Forces summary for Wuchan Zhongda Group—clarifies competitive pressures and supplier/buyer dynamics for fast strategic decisions. Customizable pressure levels and an instant radar chart let you model scenarios and soothe stakeholder concerns.

Customers Bargaining Power

Large industrial buyers with scale

Downstream customers in energy, manufacturing and agriculture purchase in bulk and run competitive tenders, reflecting China’s 2023 crude steel production of 1,018 million tonnes and the sector’s scale-driven procurement practices. Their purchasing scale pressures margins and service levels. Wuchan Zhongda raises switching costs by bundling trade, logistics and finance. Performance SLAs and reliability premiums help defend price.

Price transparency in commodities

In 2024 LME, ICE and S&P Global Platts continued 24/7 benchmark dissemination, compressing intra-day commodity spreads to low single-digit percent and driving buyers toward index-linked contracts with real-time adjustments; Wuchan counters by managing basis risk, offering timing optionality and guaranteed inventory availability, allowing the firm to charge justified basis and handling fees for value-add services.

Working capital demands and terms

Buyers push for extended payment terms to optimize cash cycles, increasing leverage over traders lacking strong balance sheets; ICC estimated a global trade finance gap of about 1.7 trillion USD in 2023, underscoring demand for credit support.

Wuchan Zhongda’s trade finance offerings—letters of credit, factoring and pre‑shipment finance—turn extended terms into sticky customer relationships by shouldering liquidity needs.

Disciplined credit underwriting lets Wuchan balance default risk against growth, preserving margins while supporting buyers who demand longer payment cycles.

Supply assurance and ESG requirements

Customers now prioritize continuity, traceability and ESG compliance, shifting leverage toward suppliers who can certify chain-of-custody and emissions; regulatory focus tightened in 2024 on supply-chain traceability in China, increasing compliance premiums. Wuchan Zhongda’s 2024 supplier audits and digital tracking systems meet these demands, turning compliance services into value-added offerings that temper pure price pressure.

- Traceability: mandatory supplier certification

- Compliance: audits + digital tracking as service

- Impact: shifts bargaining from price to certification

Disintermediation risk

Larger industrial buyers can bypass intermediaries and source directly from producers, especially when markets are stable and logistics are simple, increasing disintermediation risk for Wuchan Zhongda. Wuchan defends share through integrated multi-commodity programs and proprietary last-mile logistics, making direct sourcing less attractive. Its aggregation, hedging and financing capabilities create a tangible moat by offering bundled value producers and buyers cannot easily replicate.

- Direct-sourcing pressure: higher in stable, low-friction markets

- Defense: multi-commodity programs + last-mile logistics

- Moat: aggregation, hedging, trade finance

Bundled trade, logistics and finance plus traceability capture premiums as buyers compress spreads

Large industrial buyers exert strong price and payment leverage via bulk tenders and extended terms, but Wuchan Zhongda offsets pressure by bundling trade, logistics, hedging and trade finance with SLAs that justify basis/handling fees. Real‑time benchmarks in 2024 compressed spreads, raising demand for index-linked contracts; traceability and ESG compliance shifted bargaining toward certified suppliers, where Wuchan’s audits and digital tracking capture premiums.

| Metric | 2023/24 |

|---|---|

| China crude steel | 1,018 Mt (2023) |

| Global trade finance gap | 1.7 T USD (2023) |

| Intra-day spreads | ~2–5% (2024) |

Preview the Actual Deliverable

Wuchan Zhongda Group Porter's Five Forces Analysis

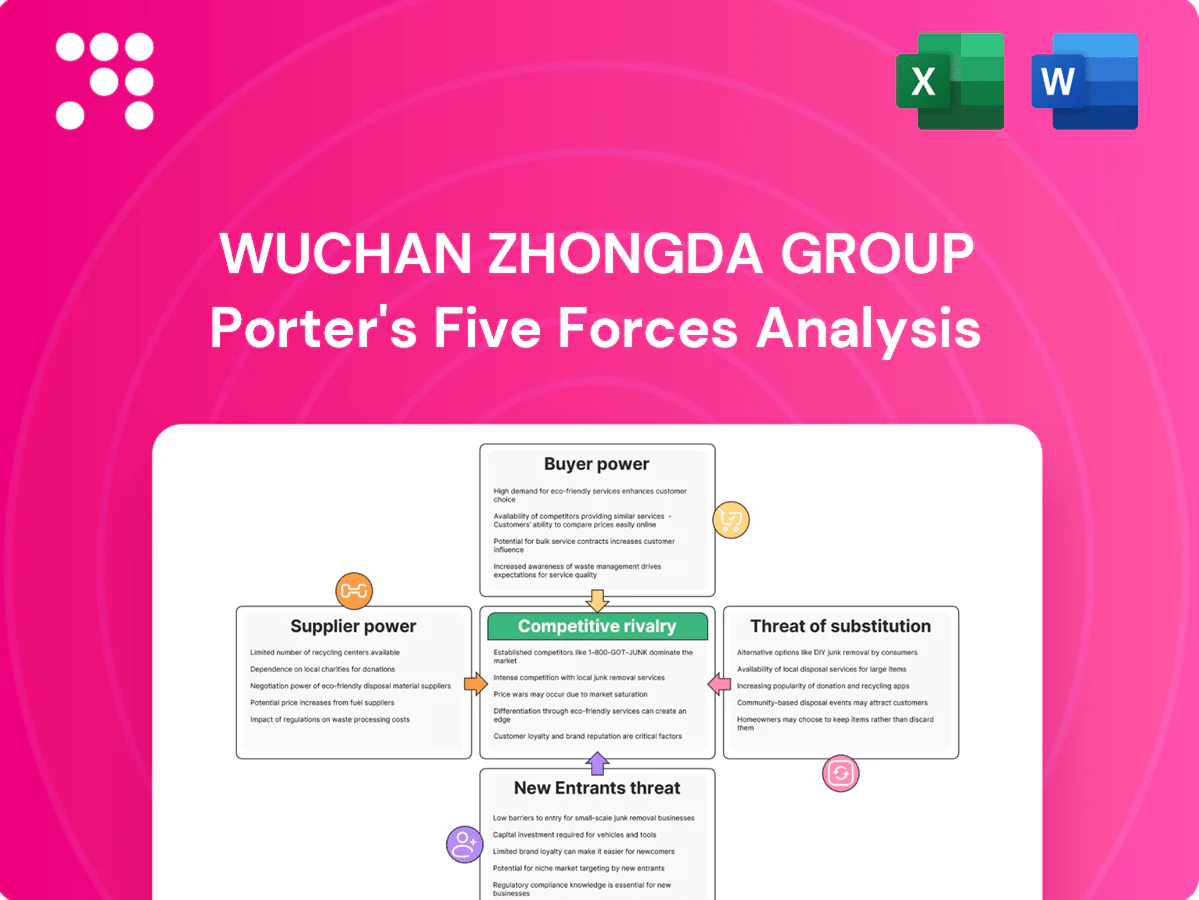

This preview is the exact Porter's Five Forces analysis of Wuchan Zhongda Group you'll receive—fully formatted, comprehensive, and ready to download immediately after purchase. It covers supplier and buyer power, competitive rivalry, threat of substitutes, and barriers to entry with actionable insights. No samples or placeholders—this is the final deliverable.

A Must-Have Tool for Decision-Makers

Wuchan Zhongda Group faces intense rivalry and moderate supplier leverage amid capital-heavy port operations, while buyer switching costs and substitute logistics channels gradually shape pricing power. Regulatory and infrastructure barriers temper new entrants but technological shifts raise strategic risk. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Wuchan Zhongda Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated upstream resources

Wuchan sources energy, metals and chemicals from a relatively concentrated set of global and domestic producers, with OPEC+ and a handful of mining majors controlling roughly 40% of oil output and a large share of key base metals in 2024. Resource owners — oil majors, mining giants, petrochemical complexes and state entities — can exert pricing and allocation power, raising switching costs in tight markets. Wuchan mitigates exposure through portfolio sourcing and long-term offtake contracts covering multi-year volumes.

Commodity cyclicality drives leverage

Commodity cyclicality drives supplier leverage: in bull phases suppliers tighten commercial terms and shorten payment windows while in downturns their bargaining power falls as they chase volume and liquidity. China remained the world’s largest steel producer in 2024, accounting for over half of global crude steel, reinforcing suppliers’ cyclical influence. Wuchan’s counter‑cyclical buying and inventory financing smooths cash flow, and its scale supports take‑or‑pay and prepay contracts that secure priority supply.

Logistics chokepoints and port capacity

Bulk commodities rely on constrained rail links, port berths and storage where capacity owners can dictate throughput and fees; seasonal congestion and intensified regulatory inspections further amplify supplier leverage. Wuchan Zhongda’s integrated logistics network and long-term contracted capacities reduce its exposure to spot constraints. Multiple diversified corridors provide resilient back-up routing, lowering single-node dependency.

Spec quality and certification constraints

Industrial buyers demand specific grades and certifications (eg national GB, ISO, API), restricting acceptable upstream sources and narrowing supplier pools for niche chemicals and specialty metals; Wuchan manages this through vetted vendor rosters to preserve procurement optionality. Technical teams evaluate and enable qualified substitutions where standards and safety allow, reducing single-source risks.

State linkages and policy priorities

As a large SOE, Wuchan Zhongda benefits from alignment with domestic producers and policy-driven allocations, which reduce supply disruption risk but can raise supplier leverage when export controls, quotas or price floors are imposed. Strong government relationships allow the group to negotiate volumes and allocations during regulatory shifts, while improved policy visibility in 2024 aided planning and hedging across procurement cycles.

- State alignment reduces short-term disruption

- Export controls and quotas elevate supplier power

- Government ties enable negotiated volumes

- 2024 policy visibility improved hedging

Energy and metals concentrated: ≈40% OPEC+ oil, >50% China steel

Supplier power is high for energy and key metals: OPEC+ controlled roughly 40% of oil output in 2024 and China accounted for >50% of global crude steel, concentrating pricing and allocation leverage. Wuchan offsets this via portfolio sourcing, long‑term offtake and integrated logistics that lower spot exposure and routing risk. Certification requirements and state alignment further constrain supplier pools but provide preferential allocations.

| Metric | 2024 value | Implication |

|---|---|---|

| OPEC+ oil share | ≈40% | High price/allocation leverage |

| China crude steel | >50% | Strong cyclical supplier influence |

| Wuchan mitigation | Long‑term contracts + logistics | Reduced spot risk |

What is included in the product

Tailored Porter’s Five Forces analysis for Wuchan Zhongda Group uncovering competitive intensity, supplier and buyer bargaining power, threat of new entrants and substitutes, and industry-specific barriers that shape pricing, margins, and strategic positioning.

A concise, one-sheet Porter's Five Forces summary for Wuchan Zhongda Group—clarifies competitive pressures and supplier/buyer dynamics for fast strategic decisions. Customizable pressure levels and an instant radar chart let you model scenarios and soothe stakeholder concerns.

Customers Bargaining Power

Large industrial buyers with scale

Downstream customers in energy, manufacturing and agriculture purchase in bulk and run competitive tenders, reflecting China’s 2023 crude steel production of 1,018 million tonnes and the sector’s scale-driven procurement practices. Their purchasing scale pressures margins and service levels. Wuchan Zhongda raises switching costs by bundling trade, logistics and finance. Performance SLAs and reliability premiums help defend price.

Price transparency in commodities

In 2024 LME, ICE and S&P Global Platts continued 24/7 benchmark dissemination, compressing intra-day commodity spreads to low single-digit percent and driving buyers toward index-linked contracts with real-time adjustments; Wuchan counters by managing basis risk, offering timing optionality and guaranteed inventory availability, allowing the firm to charge justified basis and handling fees for value-add services.

Working capital demands and terms

Buyers push for extended payment terms to optimize cash cycles, increasing leverage over traders lacking strong balance sheets; ICC estimated a global trade finance gap of about 1.7 trillion USD in 2023, underscoring demand for credit support.

Wuchan Zhongda’s trade finance offerings—letters of credit, factoring and pre‑shipment finance—turn extended terms into sticky customer relationships by shouldering liquidity needs.

Disciplined credit underwriting lets Wuchan balance default risk against growth, preserving margins while supporting buyers who demand longer payment cycles.

Supply assurance and ESG requirements

Customers now prioritize continuity, traceability and ESG compliance, shifting leverage toward suppliers who can certify chain-of-custody and emissions; regulatory focus tightened in 2024 on supply-chain traceability in China, increasing compliance premiums. Wuchan Zhongda’s 2024 supplier audits and digital tracking systems meet these demands, turning compliance services into value-added offerings that temper pure price pressure.

- Traceability: mandatory supplier certification

- Compliance: audits + digital tracking as service

- Impact: shifts bargaining from price to certification

Disintermediation risk

Larger industrial buyers can bypass intermediaries and source directly from producers, especially when markets are stable and logistics are simple, increasing disintermediation risk for Wuchan Zhongda. Wuchan defends share through integrated multi-commodity programs and proprietary last-mile logistics, making direct sourcing less attractive. Its aggregation, hedging and financing capabilities create a tangible moat by offering bundled value producers and buyers cannot easily replicate.

- Direct-sourcing pressure: higher in stable, low-friction markets

- Defense: multi-commodity programs + last-mile logistics

- Moat: aggregation, hedging, trade finance

Bundled trade, logistics and finance plus traceability capture premiums as buyers compress spreads

Large industrial buyers exert strong price and payment leverage via bulk tenders and extended terms, but Wuchan Zhongda offsets pressure by bundling trade, logistics, hedging and trade finance with SLAs that justify basis/handling fees. Real‑time benchmarks in 2024 compressed spreads, raising demand for index-linked contracts; traceability and ESG compliance shifted bargaining toward certified suppliers, where Wuchan’s audits and digital tracking capture premiums.

| Metric | 2023/24 |

|---|---|

| China crude steel | 1,018 Mt (2023) |

| Global trade finance gap | 1.7 T USD (2023) |

| Intra-day spreads | ~2–5% (2024) |

Preview the Actual Deliverable

Wuchan Zhongda Group Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis of Wuchan Zhongda Group you'll receive—fully formatted, comprehensive, and ready to download immediately after purchase. It covers supplier and buyer power, competitive rivalry, threat of substitutes, and barriers to entry with actionable insights. No samples or placeholders—this is the final deliverable.

Description

A Must-Have Tool for Decision-Makers

Wuchan Zhongda Group faces intense rivalry and moderate supplier leverage amid capital-heavy port operations, while buyer switching costs and substitute logistics channels gradually shape pricing power. Regulatory and infrastructure barriers temper new entrants but technological shifts raise strategic risk. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Wuchan Zhongda Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated upstream resources

Wuchan sources energy, metals and chemicals from a relatively concentrated set of global and domestic producers, with OPEC+ and a handful of mining majors controlling roughly 40% of oil output and a large share of key base metals in 2024. Resource owners — oil majors, mining giants, petrochemical complexes and state entities — can exert pricing and allocation power, raising switching costs in tight markets. Wuchan mitigates exposure through portfolio sourcing and long-term offtake contracts covering multi-year volumes.

Commodity cyclicality drives leverage

Commodity cyclicality drives supplier leverage: in bull phases suppliers tighten commercial terms and shorten payment windows while in downturns their bargaining power falls as they chase volume and liquidity. China remained the world’s largest steel producer in 2024, accounting for over half of global crude steel, reinforcing suppliers’ cyclical influence. Wuchan’s counter‑cyclical buying and inventory financing smooths cash flow, and its scale supports take‑or‑pay and prepay contracts that secure priority supply.

Logistics chokepoints and port capacity

Bulk commodities rely on constrained rail links, port berths and storage where capacity owners can dictate throughput and fees; seasonal congestion and intensified regulatory inspections further amplify supplier leverage. Wuchan Zhongda’s integrated logistics network and long-term contracted capacities reduce its exposure to spot constraints. Multiple diversified corridors provide resilient back-up routing, lowering single-node dependency.

Spec quality and certification constraints

Industrial buyers demand specific grades and certifications (eg national GB, ISO, API), restricting acceptable upstream sources and narrowing supplier pools for niche chemicals and specialty metals; Wuchan manages this through vetted vendor rosters to preserve procurement optionality. Technical teams evaluate and enable qualified substitutions where standards and safety allow, reducing single-source risks.

State linkages and policy priorities

As a large SOE, Wuchan Zhongda benefits from alignment with domestic producers and policy-driven allocations, which reduce supply disruption risk but can raise supplier leverage when export controls, quotas or price floors are imposed. Strong government relationships allow the group to negotiate volumes and allocations during regulatory shifts, while improved policy visibility in 2024 aided planning and hedging across procurement cycles.

- State alignment reduces short-term disruption

- Export controls and quotas elevate supplier power

- Government ties enable negotiated volumes

- 2024 policy visibility improved hedging

Energy and metals concentrated: ≈40% OPEC+ oil, >50% China steel

Supplier power is high for energy and key metals: OPEC+ controlled roughly 40% of oil output in 2024 and China accounted for >50% of global crude steel, concentrating pricing and allocation leverage. Wuchan offsets this via portfolio sourcing, long‑term offtake and integrated logistics that lower spot exposure and routing risk. Certification requirements and state alignment further constrain supplier pools but provide preferential allocations.

| Metric | 2024 value | Implication |

|---|---|---|

| OPEC+ oil share | ≈40% | High price/allocation leverage |

| China crude steel | >50% | Strong cyclical supplier influence |

| Wuchan mitigation | Long‑term contracts + logistics | Reduced spot risk |

What is included in the product

Tailored Porter’s Five Forces analysis for Wuchan Zhongda Group uncovering competitive intensity, supplier and buyer bargaining power, threat of new entrants and substitutes, and industry-specific barriers that shape pricing, margins, and strategic positioning.

A concise, one-sheet Porter's Five Forces summary for Wuchan Zhongda Group—clarifies competitive pressures and supplier/buyer dynamics for fast strategic decisions. Customizable pressure levels and an instant radar chart let you model scenarios and soothe stakeholder concerns.

Customers Bargaining Power

Large industrial buyers with scale

Downstream customers in energy, manufacturing and agriculture purchase in bulk and run competitive tenders, reflecting China’s 2023 crude steel production of 1,018 million tonnes and the sector’s scale-driven procurement practices. Their purchasing scale pressures margins and service levels. Wuchan Zhongda raises switching costs by bundling trade, logistics and finance. Performance SLAs and reliability premiums help defend price.

Price transparency in commodities

In 2024 LME, ICE and S&P Global Platts continued 24/7 benchmark dissemination, compressing intra-day commodity spreads to low single-digit percent and driving buyers toward index-linked contracts with real-time adjustments; Wuchan counters by managing basis risk, offering timing optionality and guaranteed inventory availability, allowing the firm to charge justified basis and handling fees for value-add services.

Working capital demands and terms

Buyers push for extended payment terms to optimize cash cycles, increasing leverage over traders lacking strong balance sheets; ICC estimated a global trade finance gap of about 1.7 trillion USD in 2023, underscoring demand for credit support.

Wuchan Zhongda’s trade finance offerings—letters of credit, factoring and pre‑shipment finance—turn extended terms into sticky customer relationships by shouldering liquidity needs.

Disciplined credit underwriting lets Wuchan balance default risk against growth, preserving margins while supporting buyers who demand longer payment cycles.

Supply assurance and ESG requirements

Customers now prioritize continuity, traceability and ESG compliance, shifting leverage toward suppliers who can certify chain-of-custody and emissions; regulatory focus tightened in 2024 on supply-chain traceability in China, increasing compliance premiums. Wuchan Zhongda’s 2024 supplier audits and digital tracking systems meet these demands, turning compliance services into value-added offerings that temper pure price pressure.

- Traceability: mandatory supplier certification

- Compliance: audits + digital tracking as service

- Impact: shifts bargaining from price to certification

Disintermediation risk

Larger industrial buyers can bypass intermediaries and source directly from producers, especially when markets are stable and logistics are simple, increasing disintermediation risk for Wuchan Zhongda. Wuchan defends share through integrated multi-commodity programs and proprietary last-mile logistics, making direct sourcing less attractive. Its aggregation, hedging and financing capabilities create a tangible moat by offering bundled value producers and buyers cannot easily replicate.

- Direct-sourcing pressure: higher in stable, low-friction markets

- Defense: multi-commodity programs + last-mile logistics

- Moat: aggregation, hedging, trade finance

Bundled trade, logistics and finance plus traceability capture premiums as buyers compress spreads

Large industrial buyers exert strong price and payment leverage via bulk tenders and extended terms, but Wuchan Zhongda offsets pressure by bundling trade, logistics, hedging and trade finance with SLAs that justify basis/handling fees. Real‑time benchmarks in 2024 compressed spreads, raising demand for index-linked contracts; traceability and ESG compliance shifted bargaining toward certified suppliers, where Wuchan’s audits and digital tracking capture premiums.

| Metric | 2023/24 |

|---|---|

| China crude steel | 1,018 Mt (2023) |

| Global trade finance gap | 1.7 T USD (2023) |

| Intra-day spreads | ~2–5% (2024) |

Preview the Actual Deliverable

Wuchan Zhongda Group Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis of Wuchan Zhongda Group you'll receive—fully formatted, comprehensive, and ready to download immediately after purchase. It covers supplier and buyer power, competitive rivalry, threat of substitutes, and barriers to entry with actionable insights. No samples or placeholders—this is the final deliverable.