Wuchan Zhongda Group PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unlock how political shifts, economic cycles, and environmental pressures shape Wuchan Zhongda Group’s prospects with our targeted PESTLE analysis; actionable insights help you anticipate risks and spot growth levers. Ideal for investors, strategists, and advisors seeking edge, this concise brief steers smarter decisions. Purchase the full report to access the complete, downloadable breakdown and implement findings immediately.

Political factors

SOE policy alignment

As a state-owned enterprise, Wuchan Zhongda must align strategy with central and provincial development plans such as the 14th Five-Year Plan (2021–2025) and relevant industrial policies; priority areas like energy security, food security and advanced manufacturing attract policy financing and project access. Rapid policy shifts can reallocate resources or change performance metrics, so close government liaison and strict compliance with SASAC and provincial authorities is mission-critical.

Geopolitical trade frictions

Export controls and sanctions directly reshape metals, energy and chemicals flows—China's Oct 2023 export-control list added 31 items including gallium and germanium, while US tariffs still target roughly $360 billion of Chinese goods. Route diversification and enhanced counterparty vetting are needed to mitigate sudden restrictions. Cross-border settlements face greater AML and sanctions scrutiny, extending lead times and raising costs. Risk premiums widen sharply during geopolitical flare-ups.

Belt and Road opportunities

Belt and Road opens sourcing and sales across 150+ partner countries with over $1 trillion of infrastructure finance mobilized since 2013, expanding Wuchan Zhongda’s addressable emerging-market demand. Port, rail and logistics projects reduce transport friction and improve connectivity; a World Bank study projects BRI could raise participating countries’ GDP by up to 2.9% by 2040. Political stability and governance quality vary widely across partners, so sovereign guarantees and project risk-sharing are critical to mitigate exposure.

Energy and commodity security

- Crude import dependence ~72% (2023)

- LNG ~30% of gas supply (2023)

- China >60% rare‑earth processing (2024)

- Estimated SPR crude capacity >400M barrels

Regional regulatory heterogeneity

Regional regulatory heterogeneity across China's 31 provincial-level divisions causes differing incentives, inspections and local content rules that affect Wuchan Zhongda's site economics. Approvals for warehousing, hazmat handling and land use are granted locally, producing variable permit timelines and conditions. Consistent operating standards across units reduce compliance drift and rework. Strong local government relations materially impact project timelines.

- 31 provincial-level divisions: varied incentives and inspections

- Local approvals: warehousing, hazmat, land use differ by jurisdiction

- Standardized ops: lowers compliance drift

- Local govt relations: key determinant of timeline

State control, export controls and US tariffs reshape energy trade; BRI >$1T, 31 items

State ownership forces alignment with 14th Five‑Year Plan and SASAC oversight, giving policy access but requiring strict compliance. Export controls (Oct 2023: 31 items) and US tariffs on ~360B USD of goods raise trade risk and sanctions scrutiny. Strategic stockpiling and BRI finance (>$1T since 2013) shape flows; provincial heterogeneity (31 divisions) alters permit timelines.

| Metric | Value |

|---|---|

| Crude import dependence (2023) | ~72% |

| LNG share (2023) | ~30% |

| Rare‑earth processing (2024) | >60% |

| Estimated SPR capacity | >400M barrels |

| BRI finance since 2013 | >$1T |

| Export‑control items (Oct 2023) | 31 |

| Provincial units | 31 |

What is included in the product

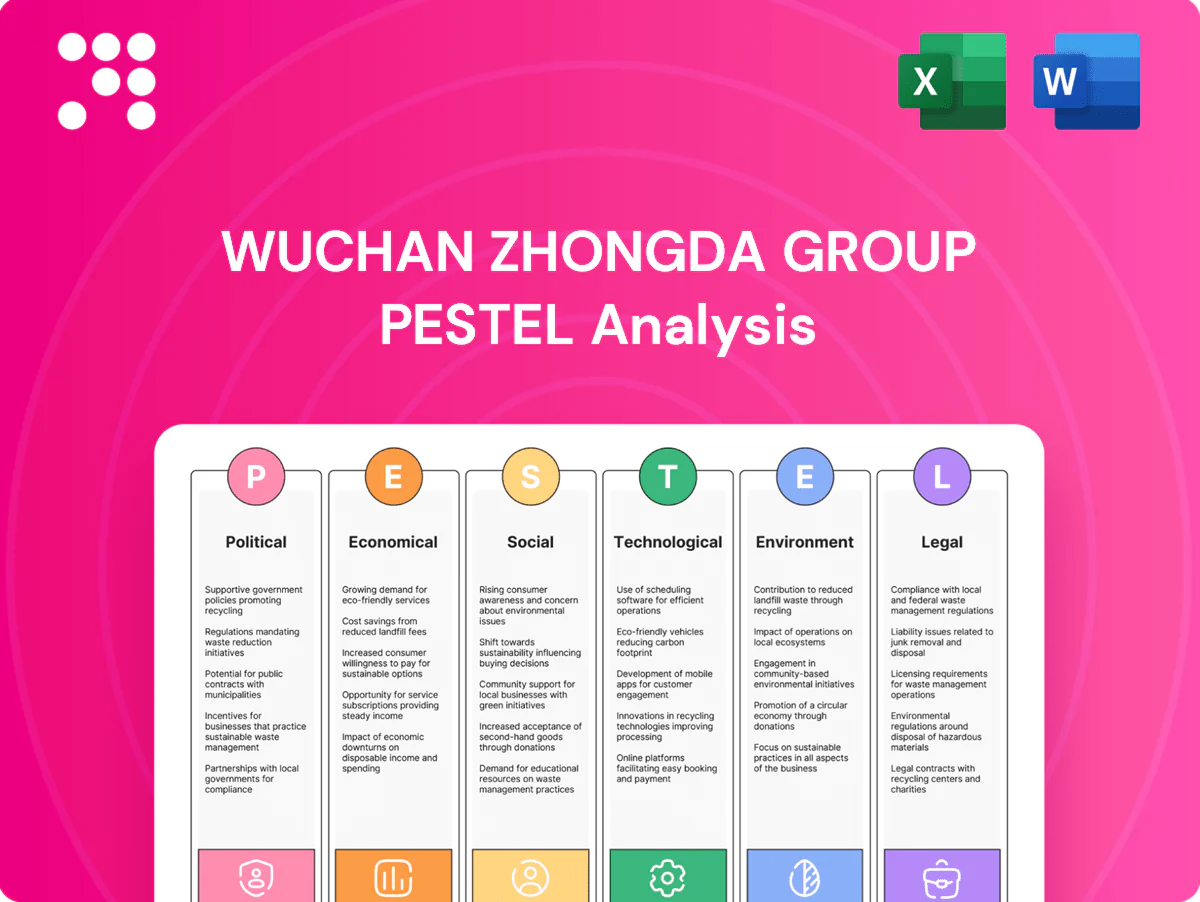

Explores how Political, Economic, Social, Technological, Environmental and Legal forces specifically affect Wuchan Zhongda Group, combining data-driven trends and region-specific examples to identify risks, opportunities and forward-looking implications for strategy, financing and operational planning.

A compact, PESTLE-segmented summary of Wuchan Zhongda Group that simplifies external risk assessment and market positioning for rapid use in meetings, presentations, and shared planning — editable for local context and client reports.

Economic factors

Commodity price cycles

Volatility in oil (Brent ranged roughly $70–$110/bbl in 2024), metals and agri-commodities drives margin variability for Wuchan Zhongda, making hedging, inventory timing and diversified commodity books essential; backwardation or contango in futures markets alters financing and storage economics, and counterparty credit risk increases sharply during downturns.

China growth and rebalancing

Slower real estate and infrastructure activity — property investment contracted about 10% in 2023 — reduces bulk steel, cement and logistics demand, while consumption and high-tech (ICT investment up ~6% in 2024) support higher‑margin products. Dual‑circulation drives import substitution and onshoring, reshaping domestic supply chains. Mix shifts change product portfolios and logistics lanes, and working capital needs pivot with sector exposure.

FX and interest rate dynamics

RMB swings have raised import and offshore-settlement costs after USD/CNY moved from ~6.9 to ~7.3 between 2021–2024, widening invoice FX exposure for Wuchan Zhongda.

Divergent rates — US Fed funds ~5.25–5.50% vs China 1yr LPR ~3.45% — raise carry, trade-finance and hedging costs for cross-border flows.

Access to low-cost onshore credit remains a competitive lever; active treasury use of FX swaps and short-term lines preserves margins.

Global supply chain reconfiguration

Nearshoring and friend-shoring are redirecting Wuchan Zhongda Group sourcing toward regional hubs, with multinationals pushing multi-origin contracts; by 2024 about 60% of global manufacturers reported active supplier diversification programs, lead times rose an estimated 12–18% and safety stocks increased, lifting inventory carrying costs roughly 15%.

- Resilience focus

- Multi-origin sourcing

- Intermodal capex gains

- Higher lead times/safety stock

Financing and liquidity conditions

- Credit: slower TSF growth in 2024

- Receivables: higher valuation scrutiny

- Liquidity: trade finance, inventory monetization

- Risk: mandatory stress tests

State control, export controls and US tariffs reshape energy trade; BRI >$1T, 31 items

Commodity price swings (Brent $70–$110/bbl in 2024) and metals/agri volatility raise margin and hedging costs for Wuchan Zhongda.

Property investment down ~10% in 2023 and slower infrastructure cut bulk-material demand while ICT capex +6% in 2024 shifts mix toward higher‑margin goods.

FX moved ~6.9→7.3 (2021–24), Fed 5.25–5.50% vs China 1yr LPR ~3.45%, lifting financing and receivables stress.

| Metric | 2024/25 |

|---|---|

| Brent | $70–$110/bbl |

| Property inv. | -10% (2023) |

| ICT capex | +6% (2024) |

| FX USD/CNY | ~7.3 (2024) |

What You See Is What You Get

Wuchan Zhongda Group PESTLE Analysis

The PESTLE analysis of Wuchan Zhongda Group outlines the political, economic, social, technological, legal and environmental factors impacting its steel, logistics and property businesses to inform strategic decisions. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use.

Your Competitive Advantage Starts with This Report

Unlock how political shifts, economic cycles, and environmental pressures shape Wuchan Zhongda Group’s prospects with our targeted PESTLE analysis; actionable insights help you anticipate risks and spot growth levers. Ideal for investors, strategists, and advisors seeking edge, this concise brief steers smarter decisions. Purchase the full report to access the complete, downloadable breakdown and implement findings immediately.

Political factors

SOE policy alignment

As a state-owned enterprise, Wuchan Zhongda must align strategy with central and provincial development plans such as the 14th Five-Year Plan (2021–2025) and relevant industrial policies; priority areas like energy security, food security and advanced manufacturing attract policy financing and project access. Rapid policy shifts can reallocate resources or change performance metrics, so close government liaison and strict compliance with SASAC and provincial authorities is mission-critical.

Geopolitical trade frictions

Export controls and sanctions directly reshape metals, energy and chemicals flows—China's Oct 2023 export-control list added 31 items including gallium and germanium, while US tariffs still target roughly $360 billion of Chinese goods. Route diversification and enhanced counterparty vetting are needed to mitigate sudden restrictions. Cross-border settlements face greater AML and sanctions scrutiny, extending lead times and raising costs. Risk premiums widen sharply during geopolitical flare-ups.

Belt and Road opportunities

Belt and Road opens sourcing and sales across 150+ partner countries with over $1 trillion of infrastructure finance mobilized since 2013, expanding Wuchan Zhongda’s addressable emerging-market demand. Port, rail and logistics projects reduce transport friction and improve connectivity; a World Bank study projects BRI could raise participating countries’ GDP by up to 2.9% by 2040. Political stability and governance quality vary widely across partners, so sovereign guarantees and project risk-sharing are critical to mitigate exposure.

Energy and commodity security

- Crude import dependence ~72% (2023)

- LNG ~30% of gas supply (2023)

- China >60% rare‑earth processing (2024)

- Estimated SPR crude capacity >400M barrels

Regional regulatory heterogeneity

Regional regulatory heterogeneity across China's 31 provincial-level divisions causes differing incentives, inspections and local content rules that affect Wuchan Zhongda's site economics. Approvals for warehousing, hazmat handling and land use are granted locally, producing variable permit timelines and conditions. Consistent operating standards across units reduce compliance drift and rework. Strong local government relations materially impact project timelines.

- 31 provincial-level divisions: varied incentives and inspections

- Local approvals: warehousing, hazmat, land use differ by jurisdiction

- Standardized ops: lowers compliance drift

- Local govt relations: key determinant of timeline

State control, export controls and US tariffs reshape energy trade; BRI >$1T, 31 items

State ownership forces alignment with 14th Five‑Year Plan and SASAC oversight, giving policy access but requiring strict compliance. Export controls (Oct 2023: 31 items) and US tariffs on ~360B USD of goods raise trade risk and sanctions scrutiny. Strategic stockpiling and BRI finance (>$1T since 2013) shape flows; provincial heterogeneity (31 divisions) alters permit timelines.

| Metric | Value |

|---|---|

| Crude import dependence (2023) | ~72% |

| LNG share (2023) | ~30% |

| Rare‑earth processing (2024) | >60% |

| Estimated SPR capacity | >400M barrels |

| BRI finance since 2013 | >$1T |

| Export‑control items (Oct 2023) | 31 |

| Provincial units | 31 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces specifically affect Wuchan Zhongda Group, combining data-driven trends and region-specific examples to identify risks, opportunities and forward-looking implications for strategy, financing and operational planning.

A compact, PESTLE-segmented summary of Wuchan Zhongda Group that simplifies external risk assessment and market positioning for rapid use in meetings, presentations, and shared planning — editable for local context and client reports.

Economic factors

Commodity price cycles

Volatility in oil (Brent ranged roughly $70–$110/bbl in 2024), metals and agri-commodities drives margin variability for Wuchan Zhongda, making hedging, inventory timing and diversified commodity books essential; backwardation or contango in futures markets alters financing and storage economics, and counterparty credit risk increases sharply during downturns.

China growth and rebalancing

Slower real estate and infrastructure activity — property investment contracted about 10% in 2023 — reduces bulk steel, cement and logistics demand, while consumption and high-tech (ICT investment up ~6% in 2024) support higher‑margin products. Dual‑circulation drives import substitution and onshoring, reshaping domestic supply chains. Mix shifts change product portfolios and logistics lanes, and working capital needs pivot with sector exposure.

FX and interest rate dynamics

RMB swings have raised import and offshore-settlement costs after USD/CNY moved from ~6.9 to ~7.3 between 2021–2024, widening invoice FX exposure for Wuchan Zhongda.

Divergent rates — US Fed funds ~5.25–5.50% vs China 1yr LPR ~3.45% — raise carry, trade-finance and hedging costs for cross-border flows.

Access to low-cost onshore credit remains a competitive lever; active treasury use of FX swaps and short-term lines preserves margins.

Global supply chain reconfiguration

Nearshoring and friend-shoring are redirecting Wuchan Zhongda Group sourcing toward regional hubs, with multinationals pushing multi-origin contracts; by 2024 about 60% of global manufacturers reported active supplier diversification programs, lead times rose an estimated 12–18% and safety stocks increased, lifting inventory carrying costs roughly 15%.

- Resilience focus

- Multi-origin sourcing

- Intermodal capex gains

- Higher lead times/safety stock

Financing and liquidity conditions

- Credit: slower TSF growth in 2024

- Receivables: higher valuation scrutiny

- Liquidity: trade finance, inventory monetization

- Risk: mandatory stress tests

State control, export controls and US tariffs reshape energy trade; BRI >$1T, 31 items

Commodity price swings (Brent $70–$110/bbl in 2024) and metals/agri volatility raise margin and hedging costs for Wuchan Zhongda.

Property investment down ~10% in 2023 and slower infrastructure cut bulk-material demand while ICT capex +6% in 2024 shifts mix toward higher‑margin goods.

FX moved ~6.9→7.3 (2021–24), Fed 5.25–5.50% vs China 1yr LPR ~3.45%, lifting financing and receivables stress.

| Metric | 2024/25 |

|---|---|

| Brent | $70–$110/bbl |

| Property inv. | -10% (2023) |

| ICT capex | +6% (2024) |

| FX USD/CNY | ~7.3 (2024) |

What You See Is What You Get

Wuchan Zhongda Group PESTLE Analysis

The PESTLE analysis of Wuchan Zhongda Group outlines the political, economic, social, technological, legal and environmental factors impacting its steel, logistics and property businesses to inform strategic decisions. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Unlock how political shifts, economic cycles, and environmental pressures shape Wuchan Zhongda Group’s prospects with our targeted PESTLE analysis; actionable insights help you anticipate risks and spot growth levers. Ideal for investors, strategists, and advisors seeking edge, this concise brief steers smarter decisions. Purchase the full report to access the complete, downloadable breakdown and implement findings immediately.

Political factors

SOE policy alignment

As a state-owned enterprise, Wuchan Zhongda must align strategy with central and provincial development plans such as the 14th Five-Year Plan (2021–2025) and relevant industrial policies; priority areas like energy security, food security and advanced manufacturing attract policy financing and project access. Rapid policy shifts can reallocate resources or change performance metrics, so close government liaison and strict compliance with SASAC and provincial authorities is mission-critical.

Geopolitical trade frictions

Export controls and sanctions directly reshape metals, energy and chemicals flows—China's Oct 2023 export-control list added 31 items including gallium and germanium, while US tariffs still target roughly $360 billion of Chinese goods. Route diversification and enhanced counterparty vetting are needed to mitigate sudden restrictions. Cross-border settlements face greater AML and sanctions scrutiny, extending lead times and raising costs. Risk premiums widen sharply during geopolitical flare-ups.

Belt and Road opportunities

Belt and Road opens sourcing and sales across 150+ partner countries with over $1 trillion of infrastructure finance mobilized since 2013, expanding Wuchan Zhongda’s addressable emerging-market demand. Port, rail and logistics projects reduce transport friction and improve connectivity; a World Bank study projects BRI could raise participating countries’ GDP by up to 2.9% by 2040. Political stability and governance quality vary widely across partners, so sovereign guarantees and project risk-sharing are critical to mitigate exposure.

Energy and commodity security

- Crude import dependence ~72% (2023)

- LNG ~30% of gas supply (2023)

- China >60% rare‑earth processing (2024)

- Estimated SPR crude capacity >400M barrels

Regional regulatory heterogeneity

Regional regulatory heterogeneity across China's 31 provincial-level divisions causes differing incentives, inspections and local content rules that affect Wuchan Zhongda's site economics. Approvals for warehousing, hazmat handling and land use are granted locally, producing variable permit timelines and conditions. Consistent operating standards across units reduce compliance drift and rework. Strong local government relations materially impact project timelines.

- 31 provincial-level divisions: varied incentives and inspections

- Local approvals: warehousing, hazmat, land use differ by jurisdiction

- Standardized ops: lowers compliance drift

- Local govt relations: key determinant of timeline

State control, export controls and US tariffs reshape energy trade; BRI >$1T, 31 items

State ownership forces alignment with 14th Five‑Year Plan and SASAC oversight, giving policy access but requiring strict compliance. Export controls (Oct 2023: 31 items) and US tariffs on ~360B USD of goods raise trade risk and sanctions scrutiny. Strategic stockpiling and BRI finance (>$1T since 2013) shape flows; provincial heterogeneity (31 divisions) alters permit timelines.

| Metric | Value |

|---|---|

| Crude import dependence (2023) | ~72% |

| LNG share (2023) | ~30% |

| Rare‑earth processing (2024) | >60% |

| Estimated SPR capacity | >400M barrels |

| BRI finance since 2013 | >$1T |

| Export‑control items (Oct 2023) | 31 |

| Provincial units | 31 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces specifically affect Wuchan Zhongda Group, combining data-driven trends and region-specific examples to identify risks, opportunities and forward-looking implications for strategy, financing and operational planning.

A compact, PESTLE-segmented summary of Wuchan Zhongda Group that simplifies external risk assessment and market positioning for rapid use in meetings, presentations, and shared planning — editable for local context and client reports.

Economic factors

Commodity price cycles

Volatility in oil (Brent ranged roughly $70–$110/bbl in 2024), metals and agri-commodities drives margin variability for Wuchan Zhongda, making hedging, inventory timing and diversified commodity books essential; backwardation or contango in futures markets alters financing and storage economics, and counterparty credit risk increases sharply during downturns.

China growth and rebalancing

Slower real estate and infrastructure activity — property investment contracted about 10% in 2023 — reduces bulk steel, cement and logistics demand, while consumption and high-tech (ICT investment up ~6% in 2024) support higher‑margin products. Dual‑circulation drives import substitution and onshoring, reshaping domestic supply chains. Mix shifts change product portfolios and logistics lanes, and working capital needs pivot with sector exposure.

FX and interest rate dynamics

RMB swings have raised import and offshore-settlement costs after USD/CNY moved from ~6.9 to ~7.3 between 2021–2024, widening invoice FX exposure for Wuchan Zhongda.

Divergent rates — US Fed funds ~5.25–5.50% vs China 1yr LPR ~3.45% — raise carry, trade-finance and hedging costs for cross-border flows.

Access to low-cost onshore credit remains a competitive lever; active treasury use of FX swaps and short-term lines preserves margins.

Global supply chain reconfiguration

Nearshoring and friend-shoring are redirecting Wuchan Zhongda Group sourcing toward regional hubs, with multinationals pushing multi-origin contracts; by 2024 about 60% of global manufacturers reported active supplier diversification programs, lead times rose an estimated 12–18% and safety stocks increased, lifting inventory carrying costs roughly 15%.

- Resilience focus

- Multi-origin sourcing

- Intermodal capex gains

- Higher lead times/safety stock

Financing and liquidity conditions

- Credit: slower TSF growth in 2024

- Receivables: higher valuation scrutiny

- Liquidity: trade finance, inventory monetization

- Risk: mandatory stress tests

State control, export controls and US tariffs reshape energy trade; BRI >$1T, 31 items

Commodity price swings (Brent $70–$110/bbl in 2024) and metals/agri volatility raise margin and hedging costs for Wuchan Zhongda.

Property investment down ~10% in 2023 and slower infrastructure cut bulk-material demand while ICT capex +6% in 2024 shifts mix toward higher‑margin goods.

FX moved ~6.9→7.3 (2021–24), Fed 5.25–5.50% vs China 1yr LPR ~3.45%, lifting financing and receivables stress.

| Metric | 2024/25 |

|---|---|

| Brent | $70–$110/bbl |

| Property inv. | -10% (2023) |

| ICT capex | +6% (2024) |

| FX USD/CNY | ~7.3 (2024) |

What You See Is What You Get

Wuchan Zhongda Group PESTLE Analysis

The PESTLE analysis of Wuchan Zhongda Group outlines the political, economic, social, technological, legal and environmental factors impacting its steel, logistics and property businesses to inform strategic decisions. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use.