Zeria Pharmaceutical Co. Business Model Canvas

Pharma business model canvas: R&D, niche therapies, partnerships driving patient value

Zeria Pharmaceutical Co.’s Business Model Canvas distills how R&D, niche therapeutics, and strategic partnerships drive patient value and revenue growth. This concise snapshot highlights target segments, key activities, and scalable revenue streams. Want the full, editable canvas with financial implications and action steps? Purchase the complete document to benchmark strategy and fast‑track planning.

Partnerships

Academic and clinical research allies

University labs and hospital networks co-develop gastroenterology, hepatology and allergy therapies, pooling translational expertise and IP pathways. They provide access to patient cohorts and clinical insights, leveraging a global registry of over 440,000 studies on ClinicalTrials.gov (2024) to streamline enrollment. Joint studies accelerate proof-of-concept and biomarker validation, while co-authored publications drive scientific credibility and KOL advocacy.

CDMOs and API suppliers

CDMOs and API suppliers enable Zeria to scale manufacturing, perform sterile filling, and manage complex formulations through specialized facilities and expertise. Reliable API partners guarantee quality and continuity across the supply chain, while dual sourcing for key molecules reduces concentration risk and improves procurement resilience. Technical transfers with CDMOs focus on yield optimization and cost-efficiency through process standardization and troubleshooting.

Licensing and co-promotion partners

In-licensing brings de-risked assets into Zeria’s pipeline, shortening time-to-market and enabling focus on core therapeutic areas; typical deal structures in 2024 featured upfronts plus milestones and royalties commonly in the 10–30% range. Out-licensing extends geographic reach and monetizes non-core regions through upfronts, tiered milestones and royalties, preserving cash and unlocking value. Co-promotion agreements boost share-of-voice in priority specialties—industry cases report ~20% uplift in promotional reach—and deal economics align milestones and royalties with lifecycle value to balance risk and reward.

Regulatory and reimbursement stakeholders

Early engagement with PMDA (established 2004) and other agencies streamlines approvals and alignment on clinical endpoints; HTA bodies such as NICE (est. 1999) shape value narratives and pricing expectations. Payer partnerships define real-world evidence requirements and budget impact constraints, while collaborative post-marketing safety plans maintain long-term market access and reimbursement.

- Regulatory alignment — PMDA

- HTA influence — NICE/others

- Payer-driven RWE

- Post-marketing safety collaboration

Retail, wholesale, and e-commerce distributors

National wholesalers secure nationwide coverage, reaching an estimated 98% of pharmacies and hospitals in 2024; retail chains drive visibility for consumer healthcare, accounting for about 65% of OTC sales; e-commerce grew ~30% in 2024, lifting direct-to-consumer share to ~15%; systematic data-sharing cut stockouts ~20% and raised promotional ROI ~25%.

Strategic partnerships accelerate R&D, scale manufacturing and secure market access

Strategic partnerships with university/hospital networks, CDMOs/API suppliers, licensors and payers accelerate R&D, scale manufacturing and secure market access, leveraging ClinicalTrials.gov (440k+ studies, 2024). Dual sourcing and in-/out-licensing reduce risk while payer/HTA engagement optimizes reimbursement and real-world evidence generation.

| Partner | Role | 2024 metric |

|---|---|---|

| Clinical networks | Trials/KOLs | 440k+ studies |

| CDMO/API | Manufacturing | Dual sourcing |

| Payers/HTA | Access | RWE reqs |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Zeria Pharmaceutical Co.—covering customer segments, channels, value propositions, revenue streams, key activities, resources and partnerships—reflecting real operations and R&D-led strategy; ideal for investor pitches, linked SWOT insights, and validation using company data.

High-level view of Zeria Pharmaceutical Co.'s business model with editable cells, highlighting how its R&D focus, regulatory strategy, and distribution network relieve pain points in drug development, compliance, and market access for faster commercialization.

Activities

Targeted R&D in GI, liver, allergy

Discovery targets mechanisms with clear clinical endpoints in GI, liver and allergy to accelerate go/no-go decisions; translational research links preclinical signals to patient outcomes using adaptive designs. Biomarker development sharpens trial enrollment and responder ID, reducing variability and cost. Portfolio reviews reallocate spend toward highest-NPV assets, aligned with global pharma R&D spending of over USD 200 billion in 2024.

Clinical development and medical affairs

Phase I–III execution (median timelines: I 1.5y, II 2y, III 3.5y; Phase III spend typically $50–100M in 2024) ensures speed, quality and compliance. KOL engagement (network >150 investigators) shapes protocols and adoption pathways. Publication plans target 30+ abstracts/yr across congresses and journals. Post-marketing studies capture RWE from cohorts >5,000 patients to prove real-world effectiveness.

Manufacturing and quality assurance

In 2024 Zeria’s in-house and partnered sites produce to cGMP/ICH standards, ensuring regulatory compliance across APIs and finished dosage forms. Process engineering initiatives reduce cost per unit and variability through scale-up optimization and lean manufacturing. Robust QA/QC systems — batch release testing, stability programs and supply-chain audits — safeguard product integrity and reliability. Continuous improvement programs (Kaizen/Six Sigma) target ongoing defect reduction.

Regulatory, market access, pricing

Dossiers for Zeria articulate clinical and economic value tied to payer thresholds (NICE 20,000–30,000 GBP/QALY as of 2024) to support reimbursement dossiers and HTA submissions. Value-based pricing aligns net price to patient outcomes, with outcomes-based agreements used in about 15% of major launches in 2024. Negotiations secure reimbursement and formulary placement while lifecycle strategies anticipate loss of exclusivity and competitive entry, where biosimilar entrants typically reduce prices 30–50% within 2–3 years.

- Clinical + economic dossiers: HTA-ready (NICE 20k–30k GBP/QALY, 2024)

- Value-based pricing: ties net price to outcomes; ~15% OBA adoption (2024)

- Negotiations: reimbursement, formulary placement

- Lifecycle: plan for LOE; expect 30–50% price decline post-biosimilar (2–3 years)

Branding, promotion, and omnichannel sales

Specialty sales teams focus on gastroenterologists, hepatologists, and allergists, combining 1:1 detailing with targeted account plans to drive formulary placement and prescribing.

Digital engagement—tele-detailing, email campaigns, and CRM-triggered content—complements field reps, with omnichannel interactions now representing over 40% of HCP touchpoints in recent industry reports (2024).

Patient education initiatives support adherence (studies show up to 20% improvement), while closed-loop insights from CRM and analytics refine messaging, channel mix, and ROI for ongoing optimization.

- Specialty targeting: gastro/hepato/allergy

- Omnichannel share: >40% of HCP touchpoints (2024)

- Adherence lift from education: up to 20%

- Closed-loop analytics to optimize messaging and ROI

Biomarker-led GI/liver/allergy R&D shortens go/no-go; global R&D spend >USD 200B

Discovery focuses GI/liver/allergy with biomarkers to shorten go/no-go; R&D context: global spend >USD 200B (2024). Phase I–III median timelines I 1.5y II 2y III 3.5y; Phase III spend $50–100M. Manufacturing cGMP; QA/QC and Kaizen cut defects. Commercial: KOL network >150, omnichannel >40% HCP touchpoints, adherence +20%.

| Metric | 2024 |

|---|---|

| Global R&D spend | >USD 200B |

What You See Is What You Get

Business Model Canvas

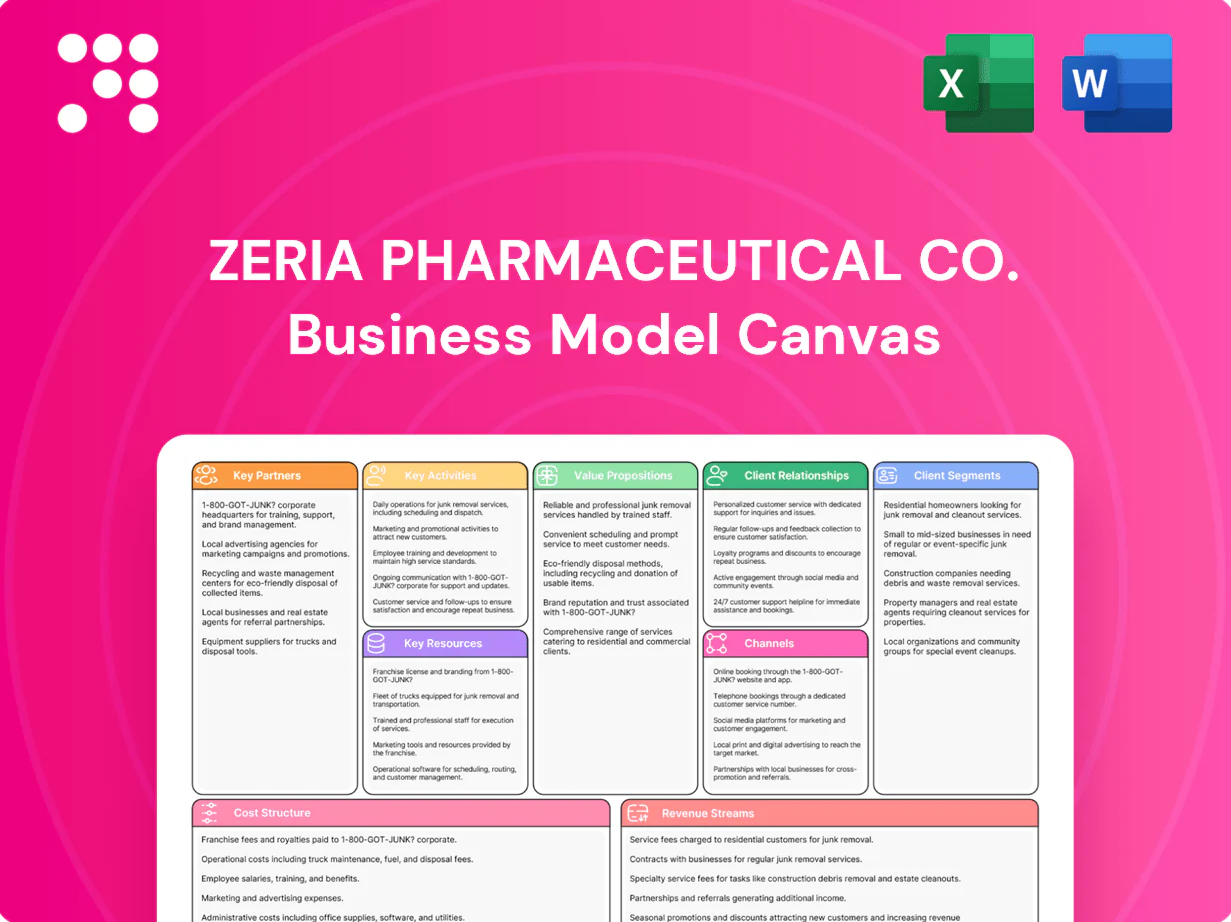

The Zeria Pharmaceutical Co. Business Model Canvas shown here is a live preview of the actual deliverable, not a mockup. When you purchase, you’ll receive this exact document—complete, editable and formatted—as the final file. The same Canvas will be provided for download in Word and Excel formats, ready to use.

Pharma business model canvas: R&D, niche therapies, partnerships driving patient value

Zeria Pharmaceutical Co.’s Business Model Canvas distills how R&D, niche therapeutics, and strategic partnerships drive patient value and revenue growth. This concise snapshot highlights target segments, key activities, and scalable revenue streams. Want the full, editable canvas with financial implications and action steps? Purchase the complete document to benchmark strategy and fast‑track planning.

Partnerships

Academic and clinical research allies

University labs and hospital networks co-develop gastroenterology, hepatology and allergy therapies, pooling translational expertise and IP pathways. They provide access to patient cohorts and clinical insights, leveraging a global registry of over 440,000 studies on ClinicalTrials.gov (2024) to streamline enrollment. Joint studies accelerate proof-of-concept and biomarker validation, while co-authored publications drive scientific credibility and KOL advocacy.

CDMOs and API suppliers

CDMOs and API suppliers enable Zeria to scale manufacturing, perform sterile filling, and manage complex formulations through specialized facilities and expertise. Reliable API partners guarantee quality and continuity across the supply chain, while dual sourcing for key molecules reduces concentration risk and improves procurement resilience. Technical transfers with CDMOs focus on yield optimization and cost-efficiency through process standardization and troubleshooting.

Licensing and co-promotion partners

In-licensing brings de-risked assets into Zeria’s pipeline, shortening time-to-market and enabling focus on core therapeutic areas; typical deal structures in 2024 featured upfronts plus milestones and royalties commonly in the 10–30% range. Out-licensing extends geographic reach and monetizes non-core regions through upfronts, tiered milestones and royalties, preserving cash and unlocking value. Co-promotion agreements boost share-of-voice in priority specialties—industry cases report ~20% uplift in promotional reach—and deal economics align milestones and royalties with lifecycle value to balance risk and reward.

Regulatory and reimbursement stakeholders

Early engagement with PMDA (established 2004) and other agencies streamlines approvals and alignment on clinical endpoints; HTA bodies such as NICE (est. 1999) shape value narratives and pricing expectations. Payer partnerships define real-world evidence requirements and budget impact constraints, while collaborative post-marketing safety plans maintain long-term market access and reimbursement.

- Regulatory alignment — PMDA

- HTA influence — NICE/others

- Payer-driven RWE

- Post-marketing safety collaboration

Retail, wholesale, and e-commerce distributors

National wholesalers secure nationwide coverage, reaching an estimated 98% of pharmacies and hospitals in 2024; retail chains drive visibility for consumer healthcare, accounting for about 65% of OTC sales; e-commerce grew ~30% in 2024, lifting direct-to-consumer share to ~15%; systematic data-sharing cut stockouts ~20% and raised promotional ROI ~25%.

Strategic partnerships accelerate R&D, scale manufacturing and secure market access

Strategic partnerships with university/hospital networks, CDMOs/API suppliers, licensors and payers accelerate R&D, scale manufacturing and secure market access, leveraging ClinicalTrials.gov (440k+ studies, 2024). Dual sourcing and in-/out-licensing reduce risk while payer/HTA engagement optimizes reimbursement and real-world evidence generation.

| Partner | Role | 2024 metric |

|---|---|---|

| Clinical networks | Trials/KOLs | 440k+ studies |

| CDMO/API | Manufacturing | Dual sourcing |

| Payers/HTA | Access | RWE reqs |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Zeria Pharmaceutical Co.—covering customer segments, channels, value propositions, revenue streams, key activities, resources and partnerships—reflecting real operations and R&D-led strategy; ideal for investor pitches, linked SWOT insights, and validation using company data.

High-level view of Zeria Pharmaceutical Co.'s business model with editable cells, highlighting how its R&D focus, regulatory strategy, and distribution network relieve pain points in drug development, compliance, and market access for faster commercialization.

Activities

Targeted R&D in GI, liver, allergy

Discovery targets mechanisms with clear clinical endpoints in GI, liver and allergy to accelerate go/no-go decisions; translational research links preclinical signals to patient outcomes using adaptive designs. Biomarker development sharpens trial enrollment and responder ID, reducing variability and cost. Portfolio reviews reallocate spend toward highest-NPV assets, aligned with global pharma R&D spending of over USD 200 billion in 2024.

Clinical development and medical affairs

Phase I–III execution (median timelines: I 1.5y, II 2y, III 3.5y; Phase III spend typically $50–100M in 2024) ensures speed, quality and compliance. KOL engagement (network >150 investigators) shapes protocols and adoption pathways. Publication plans target 30+ abstracts/yr across congresses and journals. Post-marketing studies capture RWE from cohorts >5,000 patients to prove real-world effectiveness.

Manufacturing and quality assurance

In 2024 Zeria’s in-house and partnered sites produce to cGMP/ICH standards, ensuring regulatory compliance across APIs and finished dosage forms. Process engineering initiatives reduce cost per unit and variability through scale-up optimization and lean manufacturing. Robust QA/QC systems — batch release testing, stability programs and supply-chain audits — safeguard product integrity and reliability. Continuous improvement programs (Kaizen/Six Sigma) target ongoing defect reduction.

Regulatory, market access, pricing

Dossiers for Zeria articulate clinical and economic value tied to payer thresholds (NICE 20,000–30,000 GBP/QALY as of 2024) to support reimbursement dossiers and HTA submissions. Value-based pricing aligns net price to patient outcomes, with outcomes-based agreements used in about 15% of major launches in 2024. Negotiations secure reimbursement and formulary placement while lifecycle strategies anticipate loss of exclusivity and competitive entry, where biosimilar entrants typically reduce prices 30–50% within 2–3 years.

- Clinical + economic dossiers: HTA-ready (NICE 20k–30k GBP/QALY, 2024)

- Value-based pricing: ties net price to outcomes; ~15% OBA adoption (2024)

- Negotiations: reimbursement, formulary placement

- Lifecycle: plan for LOE; expect 30–50% price decline post-biosimilar (2–3 years)

Branding, promotion, and omnichannel sales

Specialty sales teams focus on gastroenterologists, hepatologists, and allergists, combining 1:1 detailing with targeted account plans to drive formulary placement and prescribing.

Digital engagement—tele-detailing, email campaigns, and CRM-triggered content—complements field reps, with omnichannel interactions now representing over 40% of HCP touchpoints in recent industry reports (2024).

Patient education initiatives support adherence (studies show up to 20% improvement), while closed-loop insights from CRM and analytics refine messaging, channel mix, and ROI for ongoing optimization.

- Specialty targeting: gastro/hepato/allergy

- Omnichannel share: >40% of HCP touchpoints (2024)

- Adherence lift from education: up to 20%

- Closed-loop analytics to optimize messaging and ROI

Biomarker-led GI/liver/allergy R&D shortens go/no-go; global R&D spend >USD 200B

Discovery focuses GI/liver/allergy with biomarkers to shorten go/no-go; R&D context: global spend >USD 200B (2024). Phase I–III median timelines I 1.5y II 2y III 3.5y; Phase III spend $50–100M. Manufacturing cGMP; QA/QC and Kaizen cut defects. Commercial: KOL network >150, omnichannel >40% HCP touchpoints, adherence +20%.

| Metric | 2024 |

|---|---|

| Global R&D spend | >USD 200B |

What You See Is What You Get

Business Model Canvas

The Zeria Pharmaceutical Co. Business Model Canvas shown here is a live preview of the actual deliverable, not a mockup. When you purchase, you’ll receive this exact document—complete, editable and formatted—as the final file. The same Canvas will be provided for download in Word and Excel formats, ready to use.

Description

Pharma business model canvas: R&D, niche therapies, partnerships driving patient value

Zeria Pharmaceutical Co.’s Business Model Canvas distills how R&D, niche therapeutics, and strategic partnerships drive patient value and revenue growth. This concise snapshot highlights target segments, key activities, and scalable revenue streams. Want the full, editable canvas with financial implications and action steps? Purchase the complete document to benchmark strategy and fast‑track planning.

Partnerships

Academic and clinical research allies

University labs and hospital networks co-develop gastroenterology, hepatology and allergy therapies, pooling translational expertise and IP pathways. They provide access to patient cohorts and clinical insights, leveraging a global registry of over 440,000 studies on ClinicalTrials.gov (2024) to streamline enrollment. Joint studies accelerate proof-of-concept and biomarker validation, while co-authored publications drive scientific credibility and KOL advocacy.

CDMOs and API suppliers

CDMOs and API suppliers enable Zeria to scale manufacturing, perform sterile filling, and manage complex formulations through specialized facilities and expertise. Reliable API partners guarantee quality and continuity across the supply chain, while dual sourcing for key molecules reduces concentration risk and improves procurement resilience. Technical transfers with CDMOs focus on yield optimization and cost-efficiency through process standardization and troubleshooting.

Licensing and co-promotion partners

In-licensing brings de-risked assets into Zeria’s pipeline, shortening time-to-market and enabling focus on core therapeutic areas; typical deal structures in 2024 featured upfronts plus milestones and royalties commonly in the 10–30% range. Out-licensing extends geographic reach and monetizes non-core regions through upfronts, tiered milestones and royalties, preserving cash and unlocking value. Co-promotion agreements boost share-of-voice in priority specialties—industry cases report ~20% uplift in promotional reach—and deal economics align milestones and royalties with lifecycle value to balance risk and reward.

Regulatory and reimbursement stakeholders

Early engagement with PMDA (established 2004) and other agencies streamlines approvals and alignment on clinical endpoints; HTA bodies such as NICE (est. 1999) shape value narratives and pricing expectations. Payer partnerships define real-world evidence requirements and budget impact constraints, while collaborative post-marketing safety plans maintain long-term market access and reimbursement.

- Regulatory alignment — PMDA

- HTA influence — NICE/others

- Payer-driven RWE

- Post-marketing safety collaboration

Retail, wholesale, and e-commerce distributors

National wholesalers secure nationwide coverage, reaching an estimated 98% of pharmacies and hospitals in 2024; retail chains drive visibility for consumer healthcare, accounting for about 65% of OTC sales; e-commerce grew ~30% in 2024, lifting direct-to-consumer share to ~15%; systematic data-sharing cut stockouts ~20% and raised promotional ROI ~25%.

Strategic partnerships accelerate R&D, scale manufacturing and secure market access

Strategic partnerships with university/hospital networks, CDMOs/API suppliers, licensors and payers accelerate R&D, scale manufacturing and secure market access, leveraging ClinicalTrials.gov (440k+ studies, 2024). Dual sourcing and in-/out-licensing reduce risk while payer/HTA engagement optimizes reimbursement and real-world evidence generation.

| Partner | Role | 2024 metric |

|---|---|---|

| Clinical networks | Trials/KOLs | 440k+ studies |

| CDMO/API | Manufacturing | Dual sourcing |

| Payers/HTA | Access | RWE reqs |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Zeria Pharmaceutical Co.—covering customer segments, channels, value propositions, revenue streams, key activities, resources and partnerships—reflecting real operations and R&D-led strategy; ideal for investor pitches, linked SWOT insights, and validation using company data.

High-level view of Zeria Pharmaceutical Co.'s business model with editable cells, highlighting how its R&D focus, regulatory strategy, and distribution network relieve pain points in drug development, compliance, and market access for faster commercialization.

Activities

Targeted R&D in GI, liver, allergy

Discovery targets mechanisms with clear clinical endpoints in GI, liver and allergy to accelerate go/no-go decisions; translational research links preclinical signals to patient outcomes using adaptive designs. Biomarker development sharpens trial enrollment and responder ID, reducing variability and cost. Portfolio reviews reallocate spend toward highest-NPV assets, aligned with global pharma R&D spending of over USD 200 billion in 2024.

Clinical development and medical affairs

Phase I–III execution (median timelines: I 1.5y, II 2y, III 3.5y; Phase III spend typically $50–100M in 2024) ensures speed, quality and compliance. KOL engagement (network >150 investigators) shapes protocols and adoption pathways. Publication plans target 30+ abstracts/yr across congresses and journals. Post-marketing studies capture RWE from cohorts >5,000 patients to prove real-world effectiveness.

Manufacturing and quality assurance

In 2024 Zeria’s in-house and partnered sites produce to cGMP/ICH standards, ensuring regulatory compliance across APIs and finished dosage forms. Process engineering initiatives reduce cost per unit and variability through scale-up optimization and lean manufacturing. Robust QA/QC systems — batch release testing, stability programs and supply-chain audits — safeguard product integrity and reliability. Continuous improvement programs (Kaizen/Six Sigma) target ongoing defect reduction.

Regulatory, market access, pricing

Dossiers for Zeria articulate clinical and economic value tied to payer thresholds (NICE 20,000–30,000 GBP/QALY as of 2024) to support reimbursement dossiers and HTA submissions. Value-based pricing aligns net price to patient outcomes, with outcomes-based agreements used in about 15% of major launches in 2024. Negotiations secure reimbursement and formulary placement while lifecycle strategies anticipate loss of exclusivity and competitive entry, where biosimilar entrants typically reduce prices 30–50% within 2–3 years.

- Clinical + economic dossiers: HTA-ready (NICE 20k–30k GBP/QALY, 2024)

- Value-based pricing: ties net price to outcomes; ~15% OBA adoption (2024)

- Negotiations: reimbursement, formulary placement

- Lifecycle: plan for LOE; expect 30–50% price decline post-biosimilar (2–3 years)

Branding, promotion, and omnichannel sales

Specialty sales teams focus on gastroenterologists, hepatologists, and allergists, combining 1:1 detailing with targeted account plans to drive formulary placement and prescribing.

Digital engagement—tele-detailing, email campaigns, and CRM-triggered content—complements field reps, with omnichannel interactions now representing over 40% of HCP touchpoints in recent industry reports (2024).

Patient education initiatives support adherence (studies show up to 20% improvement), while closed-loop insights from CRM and analytics refine messaging, channel mix, and ROI for ongoing optimization.

- Specialty targeting: gastro/hepato/allergy

- Omnichannel share: >40% of HCP touchpoints (2024)

- Adherence lift from education: up to 20%

- Closed-loop analytics to optimize messaging and ROI

Biomarker-led GI/liver/allergy R&D shortens go/no-go; global R&D spend >USD 200B

Discovery focuses GI/liver/allergy with biomarkers to shorten go/no-go; R&D context: global spend >USD 200B (2024). Phase I–III median timelines I 1.5y II 2y III 3.5y; Phase III spend $50–100M. Manufacturing cGMP; QA/QC and Kaizen cut defects. Commercial: KOL network >150, omnichannel >40% HCP touchpoints, adherence +20%.

| Metric | 2024 |

|---|---|

| Global R&D spend | >USD 200B |

What You See Is What You Get

Business Model Canvas

The Zeria Pharmaceutical Co. Business Model Canvas shown here is a live preview of the actual deliverable, not a mockup. When you purchase, you’ll receive this exact document—complete, editable and formatted—as the final file. The same Canvas will be provided for download in Word and Excel formats, ready to use.