Zevia SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Zevia combines strong brand positioning in zero-calorie natural sodas and expanding RTD categories, but faces margin pressure from premium pricing and supply-chain sensitivity; growing health trends and international expansion offer upside while intense competition and ingredient cost swings remain threats. Purchase the full SWOT analysis for a research-backed, editable Word and Excel report to strategize, pitch, or invest with confidence.

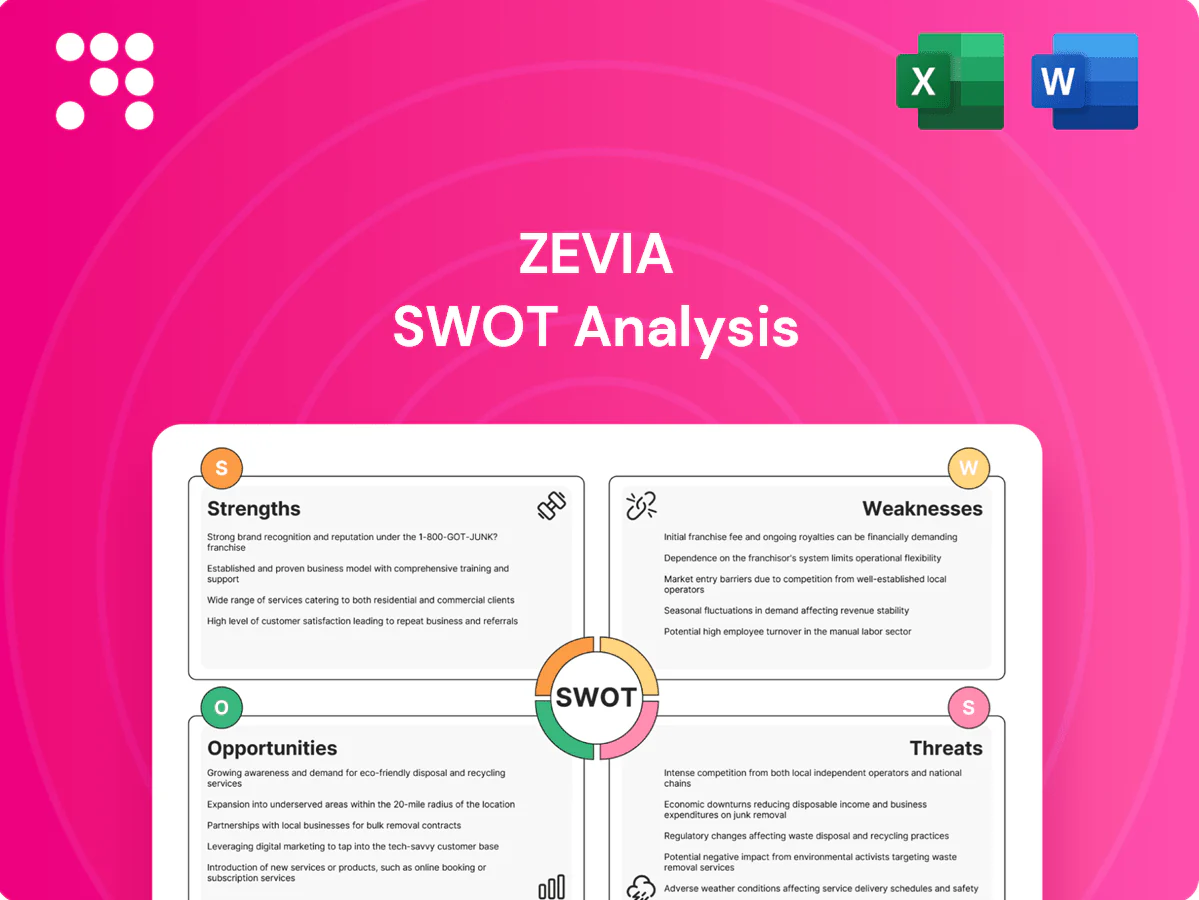

Strengths

Clean-label, zero-calorie positioning

Zevia’s formulation eliminates sugar and artificial sweeteners, aligning with health-conscious consumers and label-scrutinizers. The zero-calorie claim directly targets obesity and diabetes concerns—US adult obesity 41.9% and diabetes affects 37.3 million (11.3%) per CDC. This clarity simplifies marketing, differentiates in crowded aisles and supports premium shelf placement in natural and conventional channels.

Stevia sweetening expertise

Zevia's deep stevia leaf extract know-how improves taste profiles and batch-to-batch consistency, enabling zero-sugar beverages with mainstream appeal. Proprietary blends and formulation experience materially reduce the common stevia aftertaste seen in generic products. This technical moat is hard for newcomers to replicate quickly and supports product extensions across categories without adding sugar, helping Zevia reach 70,000+ retail locations.

Diverse portfolio across occasions

Zevia’s range across soda, energy, tea, mixers and sparkling water captures multiple use-cases and dayparts, strengthening its retailer negotiations and shelf breadth. Cross-category presence encourages basket-building and trial within the brand family, boosting per-trip purchase rates. Diversification reduces reliance on any single subcategory cycle, lowering revenue volatility.

Strong resonance with health-focused consumers

Zevia's plant-based, non-GMO, simple-ingredient messaging builds strong trust and loyalty among health-focused consumers, driving organic advocacy in wellness communities; this word-of-mouth support amplifies acquisition without heavy media spend. That audience is typically less price-sensitive when benefits are clear, and vocal advocacy converts to repeat purchases and higher lifetime value for the brand.

- plant-based / non-GMO / simple-ingredient focus

- strong word-of-mouth in wellness communities

- lower price sensitivity when benefits clear

- advocacy → repeat purchase & higher LTV

Omnichannel availability

Omnichannel availability spans natural/specialty, mainstream grocers and e-commerce, widening Zevia’s reach and reducing reliance on any single channel. Direct-to-consumer and online marketplaces enhance discovery and enable variety-pack promotions, supporting customer acquisition and repeat purchase. Channel data feeds assortment and dynamic pricing decisions and cushions demand during channel-specific disruptions.

- Channels: natural, mainstream, e-commerce

- DTC + marketplaces: discovery, variety packs

- Data-driven: assortment & pricing refinement

- Resilience: cushions channel disruptions

Stevia soda rides health trend: 41.9%, 70k+ stores

Zevia’s zero-calorie, no-sugar/no-artificial-sweeteners positioning matches health trends (US adult obesity 41.9%, diabetes 37.3M), enabling premium shelf placement. Proprietary stevia formulations improve taste consistency, supporting mainstream appeal and 70,000+ retail doors. Omnichannel DTC and e-commerce drive discovery, variety-pack upsell and data-led assortment.

| Metric | Value |

|---|---|

| US adult obesity | 41.9% |

| US diabetes | 37.3M (11.3%) |

| Retail distribution | 70,000+ locations |

What is included in the product

Provides a concise strategic assessment of Zevia’s internal strengths and weaknesses alongside external opportunities and threats, highlighting growth drivers, competitive positioning, and key risks shaping its trajectory in the beverage market.

Delivers a clear, visual SWOT matrix tailored to Zevia for rapid strategy alignment and stakeholder-ready summaries, easing cross-team planning and decision-making.

Weaknesses

Stevia taste can be polarizing

Some consumers perceive a lingering or bitter aftertaste with stevia, which reduces conversion from full-sugar and aspartame-sweetened drinkers.

Taste barriers cause higher trial drop-off and escalate marketing and sampling costs to overcome initial rejection.

This constrains velocity and distribution growth versus leading zero-sugar colas that more closely match traditional sugar taste profiles.

Price premium versus mass competitors

Zevia's clean-label ingredients and smaller scale force a retail price premium versus mass cola brands, making the brand vulnerable when budget-conscious shoppers trade down to private-label or promotional big-brand packs. Premium positioning shrinks the addressable market in economic downturns and reduces velocity in channels where promotional activity is limited, pressuring topline growth and shelf turnover.

Reliance on a single sweetener system

Zevia’s heavy reliance on stevia leaf extract as its primary sweetener concentrates supply, quality and regulatory risk despite steviol glycosides holding FDA GRAS status since 2008. Limited sweetener flexibility reduces its ability to fine-tune taste for distinct segments versus multi-sweetener rivals. Any stevia-focused negative publicity could disproportionately hurt sales and constrains innovation levers such as texture or mouthfeel formulations.

Scale disadvantages in procurement and marketing

Larger incumbents secure better terms on cans, logistics and media, with Coca-Cola and PepsiCo maintaining advertising budgets in the billions annually, while Zevia operates with a much smaller absolute ad spend. Zevia must spend more per incremental unit of awareness and lower absolute budgets limit reach in mainstream audiences. This slows share gains in core soda sets despite premium positioning.

- Incumbents: ad budgets >$2B

- Higher CPMs for small brands

- Slower share growth in mainstream soda sets

International footprint still developing

Zevia's international footprint remains modest; as of FY2023 the company reported roughly $223 million in revenue with under 10% derived from markets outside North America, limiting scale versus global peers. Regulatory, labeling and distribution differences raise per-market costs and complicate shelf entry, while a shortage of local manufacturing and retail partners slows rollout. This caps near-term revenue growth relative to multinational competitors.

- International sales <10% (FY2023)

- Higher per-market compliance & distribution costs

- Limited local partnerships slow entry

- Near-term growth capped vs global peers

Stevia aftertaste curbs trial; price premium and small scale undermine growth resilience

Stevia aftertaste limits conversion from full-sugar drinkers, raising trial drop-off and marketing/sampling costs.

Price premium versus mass brands and limited scale reduce velocity and make Zevia vulnerable in downturns.

Concentrated reliance on stevia and modest international presence constrain formulation flexibility and near-term growth.

| Metric | Value |

|---|---|

| FY2023 Revenue | $223M |

| Intl Sales | <10% |

| Incumbent Ad Budgets | >$2B |

Full Version Awaits

Zevia SWOT Analysis

This is the actual Zevia SWOT analysis document you'll receive upon purchase—no surprises, just professional, structured content. The preview below is taken directly from the full report and reflects the same editable file included with your download. Buy now to unlock the complete, detailed version and use it immediately in your workflow.

Go Beyond the Preview—Access the Full Strategic Report

Zevia combines strong brand positioning in zero-calorie natural sodas and expanding RTD categories, but faces margin pressure from premium pricing and supply-chain sensitivity; growing health trends and international expansion offer upside while intense competition and ingredient cost swings remain threats. Purchase the full SWOT analysis for a research-backed, editable Word and Excel report to strategize, pitch, or invest with confidence.

Strengths

Clean-label, zero-calorie positioning

Zevia’s formulation eliminates sugar and artificial sweeteners, aligning with health-conscious consumers and label-scrutinizers. The zero-calorie claim directly targets obesity and diabetes concerns—US adult obesity 41.9% and diabetes affects 37.3 million (11.3%) per CDC. This clarity simplifies marketing, differentiates in crowded aisles and supports premium shelf placement in natural and conventional channels.

Stevia sweetening expertise

Zevia's deep stevia leaf extract know-how improves taste profiles and batch-to-batch consistency, enabling zero-sugar beverages with mainstream appeal. Proprietary blends and formulation experience materially reduce the common stevia aftertaste seen in generic products. This technical moat is hard for newcomers to replicate quickly and supports product extensions across categories without adding sugar, helping Zevia reach 70,000+ retail locations.

Diverse portfolio across occasions

Zevia’s range across soda, energy, tea, mixers and sparkling water captures multiple use-cases and dayparts, strengthening its retailer negotiations and shelf breadth. Cross-category presence encourages basket-building and trial within the brand family, boosting per-trip purchase rates. Diversification reduces reliance on any single subcategory cycle, lowering revenue volatility.

Strong resonance with health-focused consumers

Zevia's plant-based, non-GMO, simple-ingredient messaging builds strong trust and loyalty among health-focused consumers, driving organic advocacy in wellness communities; this word-of-mouth support amplifies acquisition without heavy media spend. That audience is typically less price-sensitive when benefits are clear, and vocal advocacy converts to repeat purchases and higher lifetime value for the brand.

- plant-based / non-GMO / simple-ingredient focus

- strong word-of-mouth in wellness communities

- lower price sensitivity when benefits clear

- advocacy → repeat purchase & higher LTV

Omnichannel availability

Omnichannel availability spans natural/specialty, mainstream grocers and e-commerce, widening Zevia’s reach and reducing reliance on any single channel. Direct-to-consumer and online marketplaces enhance discovery and enable variety-pack promotions, supporting customer acquisition and repeat purchase. Channel data feeds assortment and dynamic pricing decisions and cushions demand during channel-specific disruptions.

- Channels: natural, mainstream, e-commerce

- DTC + marketplaces: discovery, variety packs

- Data-driven: assortment & pricing refinement

- Resilience: cushions channel disruptions

Stevia soda rides health trend: 41.9%, 70k+ stores

Zevia’s zero-calorie, no-sugar/no-artificial-sweeteners positioning matches health trends (US adult obesity 41.9%, diabetes 37.3M), enabling premium shelf placement. Proprietary stevia formulations improve taste consistency, supporting mainstream appeal and 70,000+ retail doors. Omnichannel DTC and e-commerce drive discovery, variety-pack upsell and data-led assortment.

| Metric | Value |

|---|---|

| US adult obesity | 41.9% |

| US diabetes | 37.3M (11.3%) |

| Retail distribution | 70,000+ locations |

What is included in the product

Provides a concise strategic assessment of Zevia’s internal strengths and weaknesses alongside external opportunities and threats, highlighting growth drivers, competitive positioning, and key risks shaping its trajectory in the beverage market.

Delivers a clear, visual SWOT matrix tailored to Zevia for rapid strategy alignment and stakeholder-ready summaries, easing cross-team planning and decision-making.

Weaknesses

Stevia taste can be polarizing

Some consumers perceive a lingering or bitter aftertaste with stevia, which reduces conversion from full-sugar and aspartame-sweetened drinkers.

Taste barriers cause higher trial drop-off and escalate marketing and sampling costs to overcome initial rejection.

This constrains velocity and distribution growth versus leading zero-sugar colas that more closely match traditional sugar taste profiles.

Price premium versus mass competitors

Zevia's clean-label ingredients and smaller scale force a retail price premium versus mass cola brands, making the brand vulnerable when budget-conscious shoppers trade down to private-label or promotional big-brand packs. Premium positioning shrinks the addressable market in economic downturns and reduces velocity in channels where promotional activity is limited, pressuring topline growth and shelf turnover.

Reliance on a single sweetener system

Zevia’s heavy reliance on stevia leaf extract as its primary sweetener concentrates supply, quality and regulatory risk despite steviol glycosides holding FDA GRAS status since 2008. Limited sweetener flexibility reduces its ability to fine-tune taste for distinct segments versus multi-sweetener rivals. Any stevia-focused negative publicity could disproportionately hurt sales and constrains innovation levers such as texture or mouthfeel formulations.

Scale disadvantages in procurement and marketing

Larger incumbents secure better terms on cans, logistics and media, with Coca-Cola and PepsiCo maintaining advertising budgets in the billions annually, while Zevia operates with a much smaller absolute ad spend. Zevia must spend more per incremental unit of awareness and lower absolute budgets limit reach in mainstream audiences. This slows share gains in core soda sets despite premium positioning.

- Incumbents: ad budgets >$2B

- Higher CPMs for small brands

- Slower share growth in mainstream soda sets

International footprint still developing

Zevia's international footprint remains modest; as of FY2023 the company reported roughly $223 million in revenue with under 10% derived from markets outside North America, limiting scale versus global peers. Regulatory, labeling and distribution differences raise per-market costs and complicate shelf entry, while a shortage of local manufacturing and retail partners slows rollout. This caps near-term revenue growth relative to multinational competitors.

- International sales <10% (FY2023)

- Higher per-market compliance & distribution costs

- Limited local partnerships slow entry

- Near-term growth capped vs global peers

Stevia aftertaste curbs trial; price premium and small scale undermine growth resilience

Stevia aftertaste limits conversion from full-sugar drinkers, raising trial drop-off and marketing/sampling costs.

Price premium versus mass brands and limited scale reduce velocity and make Zevia vulnerable in downturns.

Concentrated reliance on stevia and modest international presence constrain formulation flexibility and near-term growth.

| Metric | Value |

|---|---|

| FY2023 Revenue | $223M |

| Intl Sales | <10% |

| Incumbent Ad Budgets | >$2B |

Full Version Awaits

Zevia SWOT Analysis

This is the actual Zevia SWOT analysis document you'll receive upon purchase—no surprises, just professional, structured content. The preview below is taken directly from the full report and reflects the same editable file included with your download. Buy now to unlock the complete, detailed version and use it immediately in your workflow.

Description

Go Beyond the Preview—Access the Full Strategic Report

Zevia combines strong brand positioning in zero-calorie natural sodas and expanding RTD categories, but faces margin pressure from premium pricing and supply-chain sensitivity; growing health trends and international expansion offer upside while intense competition and ingredient cost swings remain threats. Purchase the full SWOT analysis for a research-backed, editable Word and Excel report to strategize, pitch, or invest with confidence.

Strengths

Clean-label, zero-calorie positioning

Zevia’s formulation eliminates sugar and artificial sweeteners, aligning with health-conscious consumers and label-scrutinizers. The zero-calorie claim directly targets obesity and diabetes concerns—US adult obesity 41.9% and diabetes affects 37.3 million (11.3%) per CDC. This clarity simplifies marketing, differentiates in crowded aisles and supports premium shelf placement in natural and conventional channels.

Stevia sweetening expertise

Zevia's deep stevia leaf extract know-how improves taste profiles and batch-to-batch consistency, enabling zero-sugar beverages with mainstream appeal. Proprietary blends and formulation experience materially reduce the common stevia aftertaste seen in generic products. This technical moat is hard for newcomers to replicate quickly and supports product extensions across categories without adding sugar, helping Zevia reach 70,000+ retail locations.

Diverse portfolio across occasions

Zevia’s range across soda, energy, tea, mixers and sparkling water captures multiple use-cases and dayparts, strengthening its retailer negotiations and shelf breadth. Cross-category presence encourages basket-building and trial within the brand family, boosting per-trip purchase rates. Diversification reduces reliance on any single subcategory cycle, lowering revenue volatility.

Strong resonance with health-focused consumers

Zevia's plant-based, non-GMO, simple-ingredient messaging builds strong trust and loyalty among health-focused consumers, driving organic advocacy in wellness communities; this word-of-mouth support amplifies acquisition without heavy media spend. That audience is typically less price-sensitive when benefits are clear, and vocal advocacy converts to repeat purchases and higher lifetime value for the brand.

- plant-based / non-GMO / simple-ingredient focus

- strong word-of-mouth in wellness communities

- lower price sensitivity when benefits clear

- advocacy → repeat purchase & higher LTV

Omnichannel availability

Omnichannel availability spans natural/specialty, mainstream grocers and e-commerce, widening Zevia’s reach and reducing reliance on any single channel. Direct-to-consumer and online marketplaces enhance discovery and enable variety-pack promotions, supporting customer acquisition and repeat purchase. Channel data feeds assortment and dynamic pricing decisions and cushions demand during channel-specific disruptions.

- Channels: natural, mainstream, e-commerce

- DTC + marketplaces: discovery, variety packs

- Data-driven: assortment & pricing refinement

- Resilience: cushions channel disruptions

Stevia soda rides health trend: 41.9%, 70k+ stores

Zevia’s zero-calorie, no-sugar/no-artificial-sweeteners positioning matches health trends (US adult obesity 41.9%, diabetes 37.3M), enabling premium shelf placement. Proprietary stevia formulations improve taste consistency, supporting mainstream appeal and 70,000+ retail doors. Omnichannel DTC and e-commerce drive discovery, variety-pack upsell and data-led assortment.

| Metric | Value |

|---|---|

| US adult obesity | 41.9% |

| US diabetes | 37.3M (11.3%) |

| Retail distribution | 70,000+ locations |

What is included in the product

Provides a concise strategic assessment of Zevia’s internal strengths and weaknesses alongside external opportunities and threats, highlighting growth drivers, competitive positioning, and key risks shaping its trajectory in the beverage market.

Delivers a clear, visual SWOT matrix tailored to Zevia for rapid strategy alignment and stakeholder-ready summaries, easing cross-team planning and decision-making.

Weaknesses

Stevia taste can be polarizing

Some consumers perceive a lingering or bitter aftertaste with stevia, which reduces conversion from full-sugar and aspartame-sweetened drinkers.

Taste barriers cause higher trial drop-off and escalate marketing and sampling costs to overcome initial rejection.

This constrains velocity and distribution growth versus leading zero-sugar colas that more closely match traditional sugar taste profiles.

Price premium versus mass competitors

Zevia's clean-label ingredients and smaller scale force a retail price premium versus mass cola brands, making the brand vulnerable when budget-conscious shoppers trade down to private-label or promotional big-brand packs. Premium positioning shrinks the addressable market in economic downturns and reduces velocity in channels where promotional activity is limited, pressuring topline growth and shelf turnover.

Reliance on a single sweetener system

Zevia’s heavy reliance on stevia leaf extract as its primary sweetener concentrates supply, quality and regulatory risk despite steviol glycosides holding FDA GRAS status since 2008. Limited sweetener flexibility reduces its ability to fine-tune taste for distinct segments versus multi-sweetener rivals. Any stevia-focused negative publicity could disproportionately hurt sales and constrains innovation levers such as texture or mouthfeel formulations.

Scale disadvantages in procurement and marketing

Larger incumbents secure better terms on cans, logistics and media, with Coca-Cola and PepsiCo maintaining advertising budgets in the billions annually, while Zevia operates with a much smaller absolute ad spend. Zevia must spend more per incremental unit of awareness and lower absolute budgets limit reach in mainstream audiences. This slows share gains in core soda sets despite premium positioning.

- Incumbents: ad budgets >$2B

- Higher CPMs for small brands

- Slower share growth in mainstream soda sets

International footprint still developing

Zevia's international footprint remains modest; as of FY2023 the company reported roughly $223 million in revenue with under 10% derived from markets outside North America, limiting scale versus global peers. Regulatory, labeling and distribution differences raise per-market costs and complicate shelf entry, while a shortage of local manufacturing and retail partners slows rollout. This caps near-term revenue growth relative to multinational competitors.

- International sales <10% (FY2023)

- Higher per-market compliance & distribution costs

- Limited local partnerships slow entry

- Near-term growth capped vs global peers

Stevia aftertaste curbs trial; price premium and small scale undermine growth resilience

Stevia aftertaste limits conversion from full-sugar drinkers, raising trial drop-off and marketing/sampling costs.

Price premium versus mass brands and limited scale reduce velocity and make Zevia vulnerable in downturns.

Concentrated reliance on stevia and modest international presence constrain formulation flexibility and near-term growth.

| Metric | Value |

|---|---|

| FY2023 Revenue | $223M |

| Intl Sales | <10% |

| Incumbent Ad Budgets | >$2B |

Full Version Awaits

Zevia SWOT Analysis

This is the actual Zevia SWOT analysis document you'll receive upon purchase—no surprises, just professional, structured content. The preview below is taken directly from the full report and reflects the same editable file included with your download. Buy now to unlock the complete, detailed version and use it immediately in your workflow.