Zillow Group Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

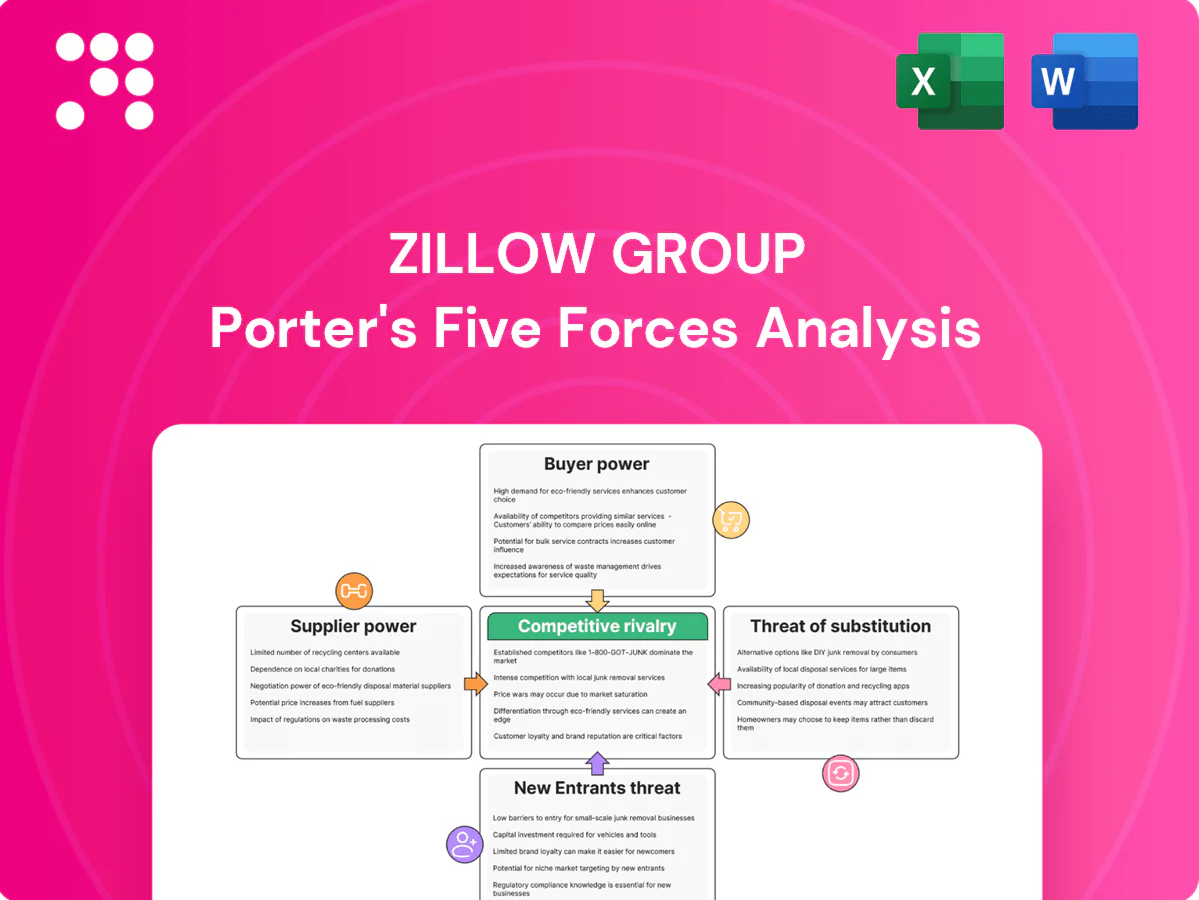

Zillow Group faces intense buyer power and substitute threats from competitors and emerging proptech, while network effects and brand scale limit new entrants; supplier power is moderate and regulatory shifts add external risk. This snapshot highlights key pressures and strategic trade-offs. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights tailored to Zillow.

Suppliers Bargaining Power

MLS and listing data dependence

Zillow depends on MLSs and brokerages for the bulk of U.S. listings, giving those data providers leverage over access and terms; MLSs set reciprocity and licensing rules that can restrict feature sets and coverage. Licensing fees and data reciprocity requirements can force product rollbacks or limit display—any withholding or delays reduce search relevance and degrade user experience, impacting traffic and ad monetization. Zillow reports heavy reliance on MLS feeds for listings and regularly negotiates feed terms to maintain completeness.

Agent and broker partners as content suppliers

Agents supply inventory photos, pricing insights and lead response that directly shape marketplace liquidity, and in 2024 agent engagement remained central to Zillow Group’s listings and lead flow. High-performing brokerages can negotiate preferred placements or pricing through Premier Agent and partnership programs, exerting leverage over visibility. Their willingness to engage determines lead quality and monetization potential for Zillow’s advertising and lead-gen revenue.

Cloud, ad-tech, and mapping infrastructure

Dependence on major clouds, CDNs and mapping APIs concentrates supplier power: AWS, Microsoft Azure and Google Cloud held roughly 31%, 22% and 12% of global cloud market share in 2024, increasing leverage over large platform customers. Pricing changes or API policy shifts (notably past Google Maps repricing) can sharply raise costs or remove features, squeezing margins. Vendor diversification reduces exposure but switching cloud/CDN/mapping providers incurs high migration, integration and downtime costs and risks.

Mortgage, title, and closing service partners

Zillow’s financing and transaction products rely on lender, title, and closing partners for execution; strong national lenders and title insurers can demand better referral fees or data access, raising supplier bargaining power. In 2024 US mortgage originations slowed from pandemic peaks to roughly $1.8 trillion, concentrating volume with large banks and increasing their leverage over platforms like Zillow. Network breadth and strict SLAs materially affect conversion rates and NPS, as limited partner coverage or slow closings reduce completed transactions and customer satisfaction.

- Supplier concentration: large lenders/title firms exert pricing/data leverage

- Market size (2024): ~ $1.8T mortgage originations — higher concentration

- Operational impact: network breadth and SLAs drive conversion and NPS

Public data, regulators, and licensors

Zillow's Zestimate and search filters depend on county records (3,143 US counties), AVM inputs, and multiple third-party data feeds; disruptions in access, pricing, or licensing of those feeds directly degrade estimate quality and product features. Changes in data availability or compliance costs limit product innovation, while privacy and fair-housing regulatory shifts act as supplier-like constraints.

Listings, cloud and lenders hold leverage over real estate portals' access and costs

Zillow depends on MLSs, brokerages and agents for listings and leads, giving them leverage over access, display rules and fees. Cloud/CDN/mapping concentration (AWS 31% Azure 22% Google 12% global cloud share in 2024) raises costs and switching risk. US mortgage originations ~ $1.8T in 2024 concentrated with large lenders, increasing lender/title bargaining power.

| Supplier | 2024 metric | Impact |

|---|---|---|

| MLSs/Brokerages | Listings majority | Access/licensing leverage |

| Cloud/CDN/Maps | AWS 31%/Azure 22%/Google 12% | Cost/API risk |

| Lenders/Title | $1.8T originations | Referral/fee leverage |

What is included in the product

Tailored Porter's Five Forces for Zillow Group assessing competitive rivalry, buyer and supplier bargaining power, threat of substitutes and new entrants, and identifying disruptive technologies, regulatory pressures, and strategic barriers that shape Zillow’s pricing power, profitability, and market positioning.

Concise Porter's Five Forces for Zillow Group that visualizes competitive pressure with a radar chart and lets you tweak inputs to test scenarios—ideal for quick decisions, pitch decks, and non-finance users.

Customers Bargaining Power

Consumers with low switching costs

Home shoppers can instantly compare Zillow with Realtor.com, Redfin, and Homes.com, amplifying price sensitivity for Zillow’s paid features. Minimal switching costs and abundant free tools mean consumers often try alternatives before paying. Retention therefore depends heavily on UI quality, breadth of active listings, and personalization of search and alerts.

Agents’ advertising budget elasticity

Agents and teams can quickly reallocate advertising budgets across platforms based on lead ROI, reducing lock-in to Zillow; transparent performance metrics from portals give agents greater bargaining power to demand lower CPCs and flexible contracts. Aggressive promotional offers from competitors in 2024 intensified negotiation leverage, forcing Zillow to adjust pricing and package terms to retain high-spend teams.

Enterprise brokers and franchises

Large enterprise brokers and franchise groups leverage scale to negotiate software and marketing bundles with Zillow Group (NASDAQ: Z), securing volume discounts and bespoke integrations that can influence product roadmaps and data-sharing terms. Their bargaining power is amplified by the threat of churn, enabling tougher contract terms and concessions on fees and APIs. In 2024 Zillow faced sustained pressure from enterprise retention demands, driving more customized commercial offers.

Rental property managers

Rental property managers wield strong bargaining power: multi-family owners list across ILS to benchmark lead costs and fill times, pressuring Zillow on pricing and product feature parity; large portfolios negotiate lower listing rates and API integrations for direct feeds; 2024 Yardi Matrix shows U.S. multifamily vacancy at about 6.8%, fueling aggressive pricing demands during cycles.

- Multi-listing enables cost/lead benchmarking

- Portfolio scale -> rate negotiation, API feeds

- 2024 vacancy ~6.8% drives price pressure

Mortgage shoppers and rate sensitivity

Bargaining power of customers is high as mortgage shoppers rapidly compare offers across marketplaces; with 30-year fixed rates near 7% in 2024 (Freddie Mac), high rate volatility makes price and speed paramount, compressing Zillow’s take-rates. Frictionless pre-approval flows and transparent pricing are essential to retain borrowers and protect conversion.

- fast comparison: seconds to minutes

- rate pressure: ~7% 30-yr (2024)

- conversion hinges on speed/transparency

Consumers, brokers squeeze ad pricing as 30-yr ~7% and vacancy ~6.8%

Customers hold high bargaining power: consumers face low switching costs and instant comparison across portals, limiting paid-feature uptake. Agents and brokers use transparent ROI metrics to push down CPCs and secure bespoke deals. Large brokers and property managers extract volume discounts and API access; 2024 pressures include ~7% 30-yr rates (Freddie Mac) and ~6.8% multifamily vacancy (Yardi Matrix).

| Segment | Leverage | 2024 metric |

|---|---|---|

| Consumers | Low switching cost, instant compare | — |

| Agents/Brokers | Negotiate CPC/terms | — |

| Property managers | Volume discounts, API feeds | Vacancy ~6.8% |

| Mortgage shoppers | Price/speed sensitivity | 30-yr ~7% |

What You See Is What You Get

Zillow Group Porter's Five Forces Analysis

This preview shows the exact Zillow Group Porter’s Five Forces analysis you’ll receive upon purchase—no placeholders or mockups. The file is fully formatted and ready for immediate download and use, covering competitive rivalry, buyer and supplier power, threat of substitutes and new entrants with actionable insights. What you see is the deliverable you’ll get instantly after payment.

A Must-Have Tool for Decision-Makers

Zillow Group faces intense buyer power and substitute threats from competitors and emerging proptech, while network effects and brand scale limit new entrants; supplier power is moderate and regulatory shifts add external risk. This snapshot highlights key pressures and strategic trade-offs. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights tailored to Zillow.

Suppliers Bargaining Power

MLS and listing data dependence

Zillow depends on MLSs and brokerages for the bulk of U.S. listings, giving those data providers leverage over access and terms; MLSs set reciprocity and licensing rules that can restrict feature sets and coverage. Licensing fees and data reciprocity requirements can force product rollbacks or limit display—any withholding or delays reduce search relevance and degrade user experience, impacting traffic and ad monetization. Zillow reports heavy reliance on MLS feeds for listings and regularly negotiates feed terms to maintain completeness.

Agent and broker partners as content suppliers

Agents supply inventory photos, pricing insights and lead response that directly shape marketplace liquidity, and in 2024 agent engagement remained central to Zillow Group’s listings and lead flow. High-performing brokerages can negotiate preferred placements or pricing through Premier Agent and partnership programs, exerting leverage over visibility. Their willingness to engage determines lead quality and monetization potential for Zillow’s advertising and lead-gen revenue.

Cloud, ad-tech, and mapping infrastructure

Dependence on major clouds, CDNs and mapping APIs concentrates supplier power: AWS, Microsoft Azure and Google Cloud held roughly 31%, 22% and 12% of global cloud market share in 2024, increasing leverage over large platform customers. Pricing changes or API policy shifts (notably past Google Maps repricing) can sharply raise costs or remove features, squeezing margins. Vendor diversification reduces exposure but switching cloud/CDN/mapping providers incurs high migration, integration and downtime costs and risks.

Mortgage, title, and closing service partners

Zillow’s financing and transaction products rely on lender, title, and closing partners for execution; strong national lenders and title insurers can demand better referral fees or data access, raising supplier bargaining power. In 2024 US mortgage originations slowed from pandemic peaks to roughly $1.8 trillion, concentrating volume with large banks and increasing their leverage over platforms like Zillow. Network breadth and strict SLAs materially affect conversion rates and NPS, as limited partner coverage or slow closings reduce completed transactions and customer satisfaction.

- Supplier concentration: large lenders/title firms exert pricing/data leverage

- Market size (2024): ~ $1.8T mortgage originations — higher concentration

- Operational impact: network breadth and SLAs drive conversion and NPS

Public data, regulators, and licensors

Zillow's Zestimate and search filters depend on county records (3,143 US counties), AVM inputs, and multiple third-party data feeds; disruptions in access, pricing, or licensing of those feeds directly degrade estimate quality and product features. Changes in data availability or compliance costs limit product innovation, while privacy and fair-housing regulatory shifts act as supplier-like constraints.

Listings, cloud and lenders hold leverage over real estate portals' access and costs

Zillow depends on MLSs, brokerages and agents for listings and leads, giving them leverage over access, display rules and fees. Cloud/CDN/mapping concentration (AWS 31% Azure 22% Google 12% global cloud share in 2024) raises costs and switching risk. US mortgage originations ~ $1.8T in 2024 concentrated with large lenders, increasing lender/title bargaining power.

| Supplier | 2024 metric | Impact |

|---|---|---|

| MLSs/Brokerages | Listings majority | Access/licensing leverage |

| Cloud/CDN/Maps | AWS 31%/Azure 22%/Google 12% | Cost/API risk |

| Lenders/Title | $1.8T originations | Referral/fee leverage |

What is included in the product

Tailored Porter's Five Forces for Zillow Group assessing competitive rivalry, buyer and supplier bargaining power, threat of substitutes and new entrants, and identifying disruptive technologies, regulatory pressures, and strategic barriers that shape Zillow’s pricing power, profitability, and market positioning.

Concise Porter's Five Forces for Zillow Group that visualizes competitive pressure with a radar chart and lets you tweak inputs to test scenarios—ideal for quick decisions, pitch decks, and non-finance users.

Customers Bargaining Power

Consumers with low switching costs

Home shoppers can instantly compare Zillow with Realtor.com, Redfin, and Homes.com, amplifying price sensitivity for Zillow’s paid features. Minimal switching costs and abundant free tools mean consumers often try alternatives before paying. Retention therefore depends heavily on UI quality, breadth of active listings, and personalization of search and alerts.

Agents’ advertising budget elasticity

Agents and teams can quickly reallocate advertising budgets across platforms based on lead ROI, reducing lock-in to Zillow; transparent performance metrics from portals give agents greater bargaining power to demand lower CPCs and flexible contracts. Aggressive promotional offers from competitors in 2024 intensified negotiation leverage, forcing Zillow to adjust pricing and package terms to retain high-spend teams.

Enterprise brokers and franchises

Large enterprise brokers and franchise groups leverage scale to negotiate software and marketing bundles with Zillow Group (NASDAQ: Z), securing volume discounts and bespoke integrations that can influence product roadmaps and data-sharing terms. Their bargaining power is amplified by the threat of churn, enabling tougher contract terms and concessions on fees and APIs. In 2024 Zillow faced sustained pressure from enterprise retention demands, driving more customized commercial offers.

Rental property managers

Rental property managers wield strong bargaining power: multi-family owners list across ILS to benchmark lead costs and fill times, pressuring Zillow on pricing and product feature parity; large portfolios negotiate lower listing rates and API integrations for direct feeds; 2024 Yardi Matrix shows U.S. multifamily vacancy at about 6.8%, fueling aggressive pricing demands during cycles.

- Multi-listing enables cost/lead benchmarking

- Portfolio scale -> rate negotiation, API feeds

- 2024 vacancy ~6.8% drives price pressure

Mortgage shoppers and rate sensitivity

Bargaining power of customers is high as mortgage shoppers rapidly compare offers across marketplaces; with 30-year fixed rates near 7% in 2024 (Freddie Mac), high rate volatility makes price and speed paramount, compressing Zillow’s take-rates. Frictionless pre-approval flows and transparent pricing are essential to retain borrowers and protect conversion.

- fast comparison: seconds to minutes

- rate pressure: ~7% 30-yr (2024)

- conversion hinges on speed/transparency

Consumers, brokers squeeze ad pricing as 30-yr ~7% and vacancy ~6.8%

Customers hold high bargaining power: consumers face low switching costs and instant comparison across portals, limiting paid-feature uptake. Agents and brokers use transparent ROI metrics to push down CPCs and secure bespoke deals. Large brokers and property managers extract volume discounts and API access; 2024 pressures include ~7% 30-yr rates (Freddie Mac) and ~6.8% multifamily vacancy (Yardi Matrix).

| Segment | Leverage | 2024 metric |

|---|---|---|

| Consumers | Low switching cost, instant compare | — |

| Agents/Brokers | Negotiate CPC/terms | — |

| Property managers | Volume discounts, API feeds | Vacancy ~6.8% |

| Mortgage shoppers | Price/speed sensitivity | 30-yr ~7% |

What You See Is What You Get

Zillow Group Porter's Five Forces Analysis

This preview shows the exact Zillow Group Porter’s Five Forces analysis you’ll receive upon purchase—no placeholders or mockups. The file is fully formatted and ready for immediate download and use, covering competitive rivalry, buyer and supplier power, threat of substitutes and new entrants with actionable insights. What you see is the deliverable you’ll get instantly after payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Zillow Group faces intense buyer power and substitute threats from competitors and emerging proptech, while network effects and brand scale limit new entrants; supplier power is moderate and regulatory shifts add external risk. This snapshot highlights key pressures and strategic trade-offs. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights tailored to Zillow.

Suppliers Bargaining Power

MLS and listing data dependence

Zillow depends on MLSs and brokerages for the bulk of U.S. listings, giving those data providers leverage over access and terms; MLSs set reciprocity and licensing rules that can restrict feature sets and coverage. Licensing fees and data reciprocity requirements can force product rollbacks or limit display—any withholding or delays reduce search relevance and degrade user experience, impacting traffic and ad monetization. Zillow reports heavy reliance on MLS feeds for listings and regularly negotiates feed terms to maintain completeness.

Agent and broker partners as content suppliers

Agents supply inventory photos, pricing insights and lead response that directly shape marketplace liquidity, and in 2024 agent engagement remained central to Zillow Group’s listings and lead flow. High-performing brokerages can negotiate preferred placements or pricing through Premier Agent and partnership programs, exerting leverage over visibility. Their willingness to engage determines lead quality and monetization potential for Zillow’s advertising and lead-gen revenue.

Cloud, ad-tech, and mapping infrastructure

Dependence on major clouds, CDNs and mapping APIs concentrates supplier power: AWS, Microsoft Azure and Google Cloud held roughly 31%, 22% and 12% of global cloud market share in 2024, increasing leverage over large platform customers. Pricing changes or API policy shifts (notably past Google Maps repricing) can sharply raise costs or remove features, squeezing margins. Vendor diversification reduces exposure but switching cloud/CDN/mapping providers incurs high migration, integration and downtime costs and risks.

Mortgage, title, and closing service partners

Zillow’s financing and transaction products rely on lender, title, and closing partners for execution; strong national lenders and title insurers can demand better referral fees or data access, raising supplier bargaining power. In 2024 US mortgage originations slowed from pandemic peaks to roughly $1.8 trillion, concentrating volume with large banks and increasing their leverage over platforms like Zillow. Network breadth and strict SLAs materially affect conversion rates and NPS, as limited partner coverage or slow closings reduce completed transactions and customer satisfaction.

- Supplier concentration: large lenders/title firms exert pricing/data leverage

- Market size (2024): ~ $1.8T mortgage originations — higher concentration

- Operational impact: network breadth and SLAs drive conversion and NPS

Public data, regulators, and licensors

Zillow's Zestimate and search filters depend on county records (3,143 US counties), AVM inputs, and multiple third-party data feeds; disruptions in access, pricing, or licensing of those feeds directly degrade estimate quality and product features. Changes in data availability or compliance costs limit product innovation, while privacy and fair-housing regulatory shifts act as supplier-like constraints.

Listings, cloud and lenders hold leverage over real estate portals' access and costs

Zillow depends on MLSs, brokerages and agents for listings and leads, giving them leverage over access, display rules and fees. Cloud/CDN/mapping concentration (AWS 31% Azure 22% Google 12% global cloud share in 2024) raises costs and switching risk. US mortgage originations ~ $1.8T in 2024 concentrated with large lenders, increasing lender/title bargaining power.

| Supplier | 2024 metric | Impact |

|---|---|---|

| MLSs/Brokerages | Listings majority | Access/licensing leverage |

| Cloud/CDN/Maps | AWS 31%/Azure 22%/Google 12% | Cost/API risk |

| Lenders/Title | $1.8T originations | Referral/fee leverage |

What is included in the product

Tailored Porter's Five Forces for Zillow Group assessing competitive rivalry, buyer and supplier bargaining power, threat of substitutes and new entrants, and identifying disruptive technologies, regulatory pressures, and strategic barriers that shape Zillow’s pricing power, profitability, and market positioning.

Concise Porter's Five Forces for Zillow Group that visualizes competitive pressure with a radar chart and lets you tweak inputs to test scenarios—ideal for quick decisions, pitch decks, and non-finance users.

Customers Bargaining Power

Consumers with low switching costs

Home shoppers can instantly compare Zillow with Realtor.com, Redfin, and Homes.com, amplifying price sensitivity for Zillow’s paid features. Minimal switching costs and abundant free tools mean consumers often try alternatives before paying. Retention therefore depends heavily on UI quality, breadth of active listings, and personalization of search and alerts.

Agents’ advertising budget elasticity

Agents and teams can quickly reallocate advertising budgets across platforms based on lead ROI, reducing lock-in to Zillow; transparent performance metrics from portals give agents greater bargaining power to demand lower CPCs and flexible contracts. Aggressive promotional offers from competitors in 2024 intensified negotiation leverage, forcing Zillow to adjust pricing and package terms to retain high-spend teams.

Enterprise brokers and franchises

Large enterprise brokers and franchise groups leverage scale to negotiate software and marketing bundles with Zillow Group (NASDAQ: Z), securing volume discounts and bespoke integrations that can influence product roadmaps and data-sharing terms. Their bargaining power is amplified by the threat of churn, enabling tougher contract terms and concessions on fees and APIs. In 2024 Zillow faced sustained pressure from enterprise retention demands, driving more customized commercial offers.

Rental property managers

Rental property managers wield strong bargaining power: multi-family owners list across ILS to benchmark lead costs and fill times, pressuring Zillow on pricing and product feature parity; large portfolios negotiate lower listing rates and API integrations for direct feeds; 2024 Yardi Matrix shows U.S. multifamily vacancy at about 6.8%, fueling aggressive pricing demands during cycles.

- Multi-listing enables cost/lead benchmarking

- Portfolio scale -> rate negotiation, API feeds

- 2024 vacancy ~6.8% drives price pressure

Mortgage shoppers and rate sensitivity

Bargaining power of customers is high as mortgage shoppers rapidly compare offers across marketplaces; with 30-year fixed rates near 7% in 2024 (Freddie Mac), high rate volatility makes price and speed paramount, compressing Zillow’s take-rates. Frictionless pre-approval flows and transparent pricing are essential to retain borrowers and protect conversion.

- fast comparison: seconds to minutes

- rate pressure: ~7% 30-yr (2024)

- conversion hinges on speed/transparency

Consumers, brokers squeeze ad pricing as 30-yr ~7% and vacancy ~6.8%

Customers hold high bargaining power: consumers face low switching costs and instant comparison across portals, limiting paid-feature uptake. Agents and brokers use transparent ROI metrics to push down CPCs and secure bespoke deals. Large brokers and property managers extract volume discounts and API access; 2024 pressures include ~7% 30-yr rates (Freddie Mac) and ~6.8% multifamily vacancy (Yardi Matrix).

| Segment | Leverage | 2024 metric |

|---|---|---|

| Consumers | Low switching cost, instant compare | — |

| Agents/Brokers | Negotiate CPC/terms | — |

| Property managers | Volume discounts, API feeds | Vacancy ~6.8% |

| Mortgage shoppers | Price/speed sensitivity | 30-yr ~7% |

What You See Is What You Get

Zillow Group Porter's Five Forces Analysis

This preview shows the exact Zillow Group Porter’s Five Forces analysis you’ll receive upon purchase—no placeholders or mockups. The file is fully formatted and ready for immediate download and use, covering competitive rivalry, buyer and supplier power, threat of substitutes and new entrants with actionable insights. What you see is the deliverable you’ll get instantly after payment.