Zimmer Biomet PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE analysis of Zimmer Biomet reveals how political, regulatory, economic, and technological trends are reshaping its market position. Actionable insights pinpoint risks and growth levers for investors and strategists. Ready-made and editable, it saves you hours of research. Purchase the full report to access the complete, downloadable analysis now.

Political factors

Healthcare policy priorities

National agendas on surgical backlogs, aging care and innovation funding drive orthopedic demand: UK elective waiting list ~7.3 million (2024) and global orthopedic market ~USD58B (2023). Policy pushes for local manufacturing and resilience—about 30% of governments offered reshoring incentives in 2024—can alter plant siting and sourcing. Post-election budget shifts have forced 5–10% cuts to hospital capital spending in some markets in 2024.

Government reimbursement influence

Public payers set pricing signals for implants and robotics, with OECD countries averaging about 72% public financing of health spending in 2022, concentrating purchasing power. Centralized procurement in markets like the UK and parts of Europe tightens margins and narrows vendor selection. CMS bundled-payment programs (CJR/BPCI) have produced low-single-digit reductions in episode costs, rewarding total-care outcomes over device unit sales.

Trade and geopolitical risk

Tariffs, export controls and rising geopolitical tensions raise component costs and extend lead times for Zimmer Biomet, a company that reported roughly $8.4 billion in revenue in FY2024, increasing input-cost sensitivity. Diversifying suppliers across North America, Europe and Asia helps mitigate disruption risk and shortened single-region dependence. Sanctions and market-access restrictions can curtail sales in affected jurisdictions and force regulatory rerouting.

Public health preparedness

Government pandemic responses that paused elective surgeries compressed Zimmer Biomet's joint and spine volumes; COVIDSurg estimated 28.4 million elective operations canceled in 2020 and US orthopedic volume fell ~80% in April 2020. Stimulus (CARES Act $2.2T; HHS Provider Relief $175B) aided catch-up recovery, while preparedness stockpiles often prioritize trauma and essential implants.

- 28.4M canceled (COVIDSurg 2020)

- US ortho ~-80% Apr 2020

- CARES $2.2T; HHS relief $175B

- Stockpiles prioritize trauma/essential implants

Procurement transparency and anti-corruption

Public-hospital tenders demand strict compliance and full disclosure of pricing, relationships and sourcing; political scrutiny of vendor relationships can trigger reviews, delays or contract cancellations that materially affect revenue recognition and backlog. Strong governance, documented audit trails and third-party due-diligence are competitive differentiators for maintaining and winning public-sector work.

- Compliance-led bidding

- Audit readiness reduces contract risk

- Vendor transparency influences public trust

Policy shifts and public payers reshape orthopedics; 7.3M waits and supplier diversification vital

National policies on elective backlogs, aging care and innovation subsidize orthopedics (UK waiting list 7.3M 2024; global market USD58B 2023) and reshape siting as ~30% of governments offered reshoring incentives in 2024. Public payers concentrate demand (OECD public financing ~72% 2022); centralized procurement and CMS bundles cut episode costs low-single-digit. Tariffs/export controls raise input costs for Zimmer Biomet (revenue ~USD8.4B FY2024), so supplier diversification reduces access risk.

| Indicator | Value |

|---|---|

| UK elective wait | 7.3M (2024) |

| Global ortho market | USD58B (2023) |

| Zimmer Biomet revenue | ~USD8.4B (FY2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect Zimmer Biomet across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed subpoints and forward-looking implications. Designed for executives and investors, it reflects current market and regulatory dynamics and is ready for reports or decks.

Concise, visually segmented PESTLE summary tailored to Zimmer Biomet that highlights external risks and opportunities for quick reference in meetings, easily editable for regional or product-specific notes and instantly sharable across teams or presentations.

Economic factors

Elective procedure cyclicality

Orthopedic volumes track consumer confidence and employment; US primary hip and knee arthroplasty ran about 1.2 million procedures annually pre-COVID. Elective procedures fell sharply in 2020—COVIDSurg Collaborative estimated ~48% reduction and a global backlog of ~28.4 million cancelled operations—showing downturns delay discretionary replacements. Recoveries have produced pent-up demand surges as systems clear backlogs and employment/consumer confidence recover.

Reimbursement and price pressure

Insurers and group purchasing organizations, which serve over 80% of US hospitals, increasingly negotiate lower implant prices, pressuring Zimmer Biomet's ASPs. Value-based payment models such as bundled payments and BPCI incentivize fewer complications and readmissions, shifting focus to outcomes. Typical total knee arthroplasty episode costs run around $30,000, so margin protection hinges on demonstrating measurable episode savings.

FX and global footprint

Zimmer Biomet generates roughly 40% of revenue from international markets and operates manufacturing and distribution in more than 25 countries, creating translation and transaction risk across multiple currencies. The company uses hedging programs and natural offsets but cannot eliminate volatility, and currency swings have produced mid-single-digit revenue impacts in recent reporting periods. Localization of production and sourcing can reduce currency and logistics exposure.

Input cost inflation

Input-cost inflation from titanium, cobalt-chrome and higher sterilization expenses materially raises Zimmer Biomet’s COGS; 2024 supply-chain pressures kept metal and sterilization service rates elevated, compressing margins. Wage inflation for skilled manufacturing and sales teams increased operating expenses in 2024–2025. Productivity gains and automation investments are critical to offset margin pressure and sustain operating leverage.

- COGS pressure: metals and sterilization elevated in 2024

- Wage inflation: skilled labor costs up in 2024–2025

- Mitigation: productivity and automation key to margin recovery

Capital spending by providers

Hospital capex cycles are key drivers of robotics and digital OR adoption; the global surgical robotics market was roughly $9.5B in 2024 with ~18–20% CAGR, concentrating purchases during upgrade cycles. Higher interest rates—US fed funds near 5.25–5.50% in 2024–25—have delayed system purchases and OR upgrades. Leasing and outcome-based contracts have expanded, sustaining uptake despite capex pressure.

Policy shifts and public payers reshape orthopedics; 7.3M waits and supplier diversification vital

Orthopedic volumes tied to consumer confidence; US primary hip/knee ~1.2M yearly pre-COVID with large 2020 backlog and strong post‑pandemic rebound. Payers and GPOs (>80% US hospitals) press ASPs while value-based bundles (~$30k TKA episode) shift focus to outcomes. Metals and sterilization cost inflation in 2024 and wage inflation 2024–25 compressed margins; hedging, automation and localization mitigate currency/COGS risks.

| Metric | 2024/25 data |

|---|---|

| US annual hips/knees | ~1.2M |

| Robotics market | $9.5B, CAGR 18–20% |

| Fed funds | ~5.25–5.50% |

Same Document Delivered

Zimmer Biomet PESTLE Analysis

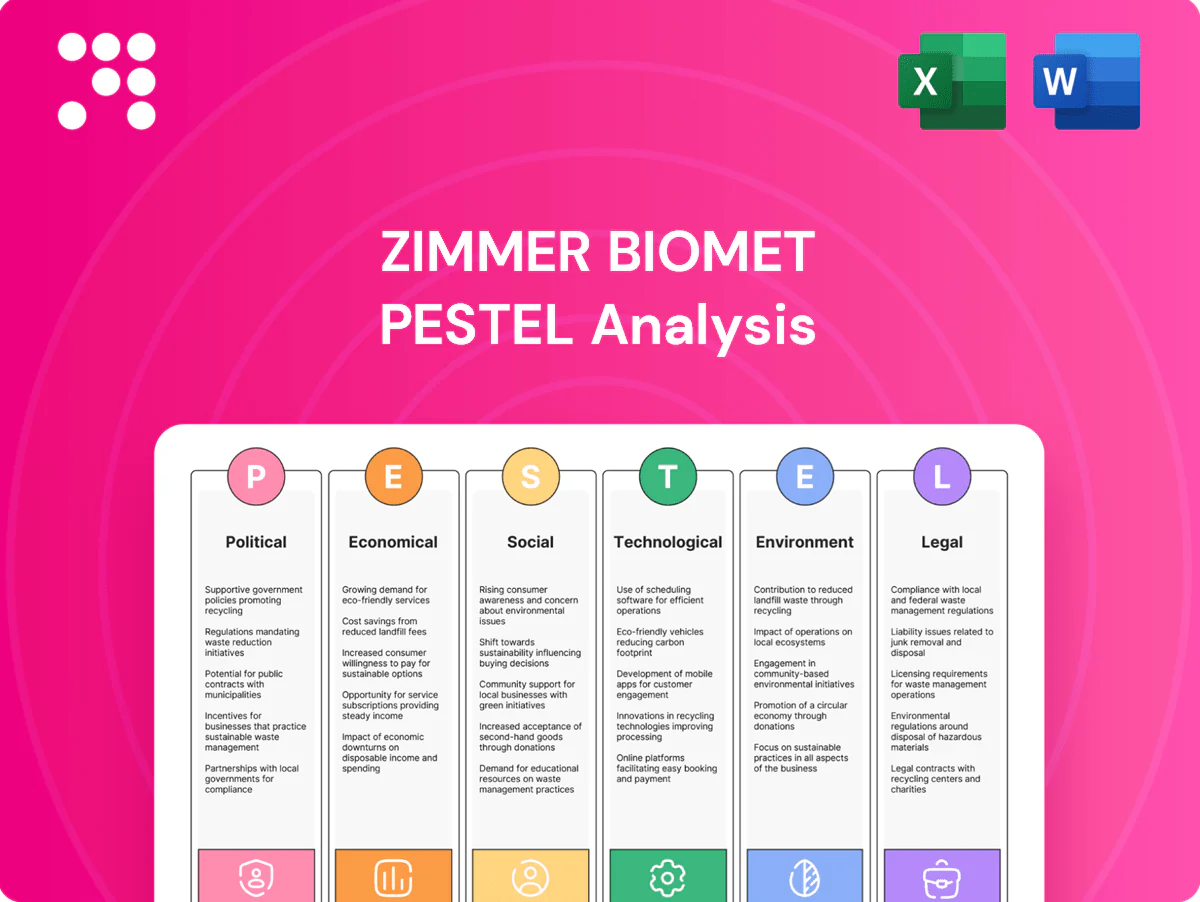

The Zimmer Biomet PESTLE Analysis provides a concise, professionally structured overview of political, economic, social, technological, legal, and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; the layout and content visible are the final file you can download immediately after checkout.

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE analysis of Zimmer Biomet reveals how political, regulatory, economic, and technological trends are reshaping its market position. Actionable insights pinpoint risks and growth levers for investors and strategists. Ready-made and editable, it saves you hours of research. Purchase the full report to access the complete, downloadable analysis now.

Political factors

Healthcare policy priorities

National agendas on surgical backlogs, aging care and innovation funding drive orthopedic demand: UK elective waiting list ~7.3 million (2024) and global orthopedic market ~USD58B (2023). Policy pushes for local manufacturing and resilience—about 30% of governments offered reshoring incentives in 2024—can alter plant siting and sourcing. Post-election budget shifts have forced 5–10% cuts to hospital capital spending in some markets in 2024.

Government reimbursement influence

Public payers set pricing signals for implants and robotics, with OECD countries averaging about 72% public financing of health spending in 2022, concentrating purchasing power. Centralized procurement in markets like the UK and parts of Europe tightens margins and narrows vendor selection. CMS bundled-payment programs (CJR/BPCI) have produced low-single-digit reductions in episode costs, rewarding total-care outcomes over device unit sales.

Trade and geopolitical risk

Tariffs, export controls and rising geopolitical tensions raise component costs and extend lead times for Zimmer Biomet, a company that reported roughly $8.4 billion in revenue in FY2024, increasing input-cost sensitivity. Diversifying suppliers across North America, Europe and Asia helps mitigate disruption risk and shortened single-region dependence. Sanctions and market-access restrictions can curtail sales in affected jurisdictions and force regulatory rerouting.

Public health preparedness

Government pandemic responses that paused elective surgeries compressed Zimmer Biomet's joint and spine volumes; COVIDSurg estimated 28.4 million elective operations canceled in 2020 and US orthopedic volume fell ~80% in April 2020. Stimulus (CARES Act $2.2T; HHS Provider Relief $175B) aided catch-up recovery, while preparedness stockpiles often prioritize trauma and essential implants.

- 28.4M canceled (COVIDSurg 2020)

- US ortho ~-80% Apr 2020

- CARES $2.2T; HHS relief $175B

- Stockpiles prioritize trauma/essential implants

Procurement transparency and anti-corruption

Public-hospital tenders demand strict compliance and full disclosure of pricing, relationships and sourcing; political scrutiny of vendor relationships can trigger reviews, delays or contract cancellations that materially affect revenue recognition and backlog. Strong governance, documented audit trails and third-party due-diligence are competitive differentiators for maintaining and winning public-sector work.

- Compliance-led bidding

- Audit readiness reduces contract risk

- Vendor transparency influences public trust

Policy shifts and public payers reshape orthopedics; 7.3M waits and supplier diversification vital

National policies on elective backlogs, aging care and innovation subsidize orthopedics (UK waiting list 7.3M 2024; global market USD58B 2023) and reshape siting as ~30% of governments offered reshoring incentives in 2024. Public payers concentrate demand (OECD public financing ~72% 2022); centralized procurement and CMS bundles cut episode costs low-single-digit. Tariffs/export controls raise input costs for Zimmer Biomet (revenue ~USD8.4B FY2024), so supplier diversification reduces access risk.

| Indicator | Value |

|---|---|

| UK elective wait | 7.3M (2024) |

| Global ortho market | USD58B (2023) |

| Zimmer Biomet revenue | ~USD8.4B (FY2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect Zimmer Biomet across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed subpoints and forward-looking implications. Designed for executives and investors, it reflects current market and regulatory dynamics and is ready for reports or decks.

Concise, visually segmented PESTLE summary tailored to Zimmer Biomet that highlights external risks and opportunities for quick reference in meetings, easily editable for regional or product-specific notes and instantly sharable across teams or presentations.

Economic factors

Elective procedure cyclicality

Orthopedic volumes track consumer confidence and employment; US primary hip and knee arthroplasty ran about 1.2 million procedures annually pre-COVID. Elective procedures fell sharply in 2020—COVIDSurg Collaborative estimated ~48% reduction and a global backlog of ~28.4 million cancelled operations—showing downturns delay discretionary replacements. Recoveries have produced pent-up demand surges as systems clear backlogs and employment/consumer confidence recover.

Reimbursement and price pressure

Insurers and group purchasing organizations, which serve over 80% of US hospitals, increasingly negotiate lower implant prices, pressuring Zimmer Biomet's ASPs. Value-based payment models such as bundled payments and BPCI incentivize fewer complications and readmissions, shifting focus to outcomes. Typical total knee arthroplasty episode costs run around $30,000, so margin protection hinges on demonstrating measurable episode savings.

FX and global footprint

Zimmer Biomet generates roughly 40% of revenue from international markets and operates manufacturing and distribution in more than 25 countries, creating translation and transaction risk across multiple currencies. The company uses hedging programs and natural offsets but cannot eliminate volatility, and currency swings have produced mid-single-digit revenue impacts in recent reporting periods. Localization of production and sourcing can reduce currency and logistics exposure.

Input cost inflation

Input-cost inflation from titanium, cobalt-chrome and higher sterilization expenses materially raises Zimmer Biomet’s COGS; 2024 supply-chain pressures kept metal and sterilization service rates elevated, compressing margins. Wage inflation for skilled manufacturing and sales teams increased operating expenses in 2024–2025. Productivity gains and automation investments are critical to offset margin pressure and sustain operating leverage.

- COGS pressure: metals and sterilization elevated in 2024

- Wage inflation: skilled labor costs up in 2024–2025

- Mitigation: productivity and automation key to margin recovery

Capital spending by providers

Hospital capex cycles are key drivers of robotics and digital OR adoption; the global surgical robotics market was roughly $9.5B in 2024 with ~18–20% CAGR, concentrating purchases during upgrade cycles. Higher interest rates—US fed funds near 5.25–5.50% in 2024–25—have delayed system purchases and OR upgrades. Leasing and outcome-based contracts have expanded, sustaining uptake despite capex pressure.

Policy shifts and public payers reshape orthopedics; 7.3M waits and supplier diversification vital

Orthopedic volumes tied to consumer confidence; US primary hip/knee ~1.2M yearly pre-COVID with large 2020 backlog and strong post‑pandemic rebound. Payers and GPOs (>80% US hospitals) press ASPs while value-based bundles (~$30k TKA episode) shift focus to outcomes. Metals and sterilization cost inflation in 2024 and wage inflation 2024–25 compressed margins; hedging, automation and localization mitigate currency/COGS risks.

| Metric | 2024/25 data |

|---|---|

| US annual hips/knees | ~1.2M |

| Robotics market | $9.5B, CAGR 18–20% |

| Fed funds | ~5.25–5.50% |

Same Document Delivered

Zimmer Biomet PESTLE Analysis

The Zimmer Biomet PESTLE Analysis provides a concise, professionally structured overview of political, economic, social, technological, legal, and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; the layout and content visible are the final file you can download immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE analysis of Zimmer Biomet reveals how political, regulatory, economic, and technological trends are reshaping its market position. Actionable insights pinpoint risks and growth levers for investors and strategists. Ready-made and editable, it saves you hours of research. Purchase the full report to access the complete, downloadable analysis now.

Political factors

Healthcare policy priorities

National agendas on surgical backlogs, aging care and innovation funding drive orthopedic demand: UK elective waiting list ~7.3 million (2024) and global orthopedic market ~USD58B (2023). Policy pushes for local manufacturing and resilience—about 30% of governments offered reshoring incentives in 2024—can alter plant siting and sourcing. Post-election budget shifts have forced 5–10% cuts to hospital capital spending in some markets in 2024.

Government reimbursement influence

Public payers set pricing signals for implants and robotics, with OECD countries averaging about 72% public financing of health spending in 2022, concentrating purchasing power. Centralized procurement in markets like the UK and parts of Europe tightens margins and narrows vendor selection. CMS bundled-payment programs (CJR/BPCI) have produced low-single-digit reductions in episode costs, rewarding total-care outcomes over device unit sales.

Trade and geopolitical risk

Tariffs, export controls and rising geopolitical tensions raise component costs and extend lead times for Zimmer Biomet, a company that reported roughly $8.4 billion in revenue in FY2024, increasing input-cost sensitivity. Diversifying suppliers across North America, Europe and Asia helps mitigate disruption risk and shortened single-region dependence. Sanctions and market-access restrictions can curtail sales in affected jurisdictions and force regulatory rerouting.

Public health preparedness

Government pandemic responses that paused elective surgeries compressed Zimmer Biomet's joint and spine volumes; COVIDSurg estimated 28.4 million elective operations canceled in 2020 and US orthopedic volume fell ~80% in April 2020. Stimulus (CARES Act $2.2T; HHS Provider Relief $175B) aided catch-up recovery, while preparedness stockpiles often prioritize trauma and essential implants.

- 28.4M canceled (COVIDSurg 2020)

- US ortho ~-80% Apr 2020

- CARES $2.2T; HHS relief $175B

- Stockpiles prioritize trauma/essential implants

Procurement transparency and anti-corruption

Public-hospital tenders demand strict compliance and full disclosure of pricing, relationships and sourcing; political scrutiny of vendor relationships can trigger reviews, delays or contract cancellations that materially affect revenue recognition and backlog. Strong governance, documented audit trails and third-party due-diligence are competitive differentiators for maintaining and winning public-sector work.

- Compliance-led bidding

- Audit readiness reduces contract risk

- Vendor transparency influences public trust

Policy shifts and public payers reshape orthopedics; 7.3M waits and supplier diversification vital

National policies on elective backlogs, aging care and innovation subsidize orthopedics (UK waiting list 7.3M 2024; global market USD58B 2023) and reshape siting as ~30% of governments offered reshoring incentives in 2024. Public payers concentrate demand (OECD public financing ~72% 2022); centralized procurement and CMS bundles cut episode costs low-single-digit. Tariffs/export controls raise input costs for Zimmer Biomet (revenue ~USD8.4B FY2024), so supplier diversification reduces access risk.

| Indicator | Value |

|---|---|

| UK elective wait | 7.3M (2024) |

| Global ortho market | USD58B (2023) |

| Zimmer Biomet revenue | ~USD8.4B (FY2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect Zimmer Biomet across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed subpoints and forward-looking implications. Designed for executives and investors, it reflects current market and regulatory dynamics and is ready for reports or decks.

Concise, visually segmented PESTLE summary tailored to Zimmer Biomet that highlights external risks and opportunities for quick reference in meetings, easily editable for regional or product-specific notes and instantly sharable across teams or presentations.

Economic factors

Elective procedure cyclicality

Orthopedic volumes track consumer confidence and employment; US primary hip and knee arthroplasty ran about 1.2 million procedures annually pre-COVID. Elective procedures fell sharply in 2020—COVIDSurg Collaborative estimated ~48% reduction and a global backlog of ~28.4 million cancelled operations—showing downturns delay discretionary replacements. Recoveries have produced pent-up demand surges as systems clear backlogs and employment/consumer confidence recover.

Reimbursement and price pressure

Insurers and group purchasing organizations, which serve over 80% of US hospitals, increasingly negotiate lower implant prices, pressuring Zimmer Biomet's ASPs. Value-based payment models such as bundled payments and BPCI incentivize fewer complications and readmissions, shifting focus to outcomes. Typical total knee arthroplasty episode costs run around $30,000, so margin protection hinges on demonstrating measurable episode savings.

FX and global footprint

Zimmer Biomet generates roughly 40% of revenue from international markets and operates manufacturing and distribution in more than 25 countries, creating translation and transaction risk across multiple currencies. The company uses hedging programs and natural offsets but cannot eliminate volatility, and currency swings have produced mid-single-digit revenue impacts in recent reporting periods. Localization of production and sourcing can reduce currency and logistics exposure.

Input cost inflation

Input-cost inflation from titanium, cobalt-chrome and higher sterilization expenses materially raises Zimmer Biomet’s COGS; 2024 supply-chain pressures kept metal and sterilization service rates elevated, compressing margins. Wage inflation for skilled manufacturing and sales teams increased operating expenses in 2024–2025. Productivity gains and automation investments are critical to offset margin pressure and sustain operating leverage.

- COGS pressure: metals and sterilization elevated in 2024

- Wage inflation: skilled labor costs up in 2024–2025

- Mitigation: productivity and automation key to margin recovery

Capital spending by providers

Hospital capex cycles are key drivers of robotics and digital OR adoption; the global surgical robotics market was roughly $9.5B in 2024 with ~18–20% CAGR, concentrating purchases during upgrade cycles. Higher interest rates—US fed funds near 5.25–5.50% in 2024–25—have delayed system purchases and OR upgrades. Leasing and outcome-based contracts have expanded, sustaining uptake despite capex pressure.

Policy shifts and public payers reshape orthopedics; 7.3M waits and supplier diversification vital

Orthopedic volumes tied to consumer confidence; US primary hip/knee ~1.2M yearly pre-COVID with large 2020 backlog and strong post‑pandemic rebound. Payers and GPOs (>80% US hospitals) press ASPs while value-based bundles (~$30k TKA episode) shift focus to outcomes. Metals and sterilization cost inflation in 2024 and wage inflation 2024–25 compressed margins; hedging, automation and localization mitigate currency/COGS risks.

| Metric | 2024/25 data |

|---|---|

| US annual hips/knees | ~1.2M |

| Robotics market | $9.5B, CAGR 18–20% |

| Fed funds | ~5.25–5.50% |

Same Document Delivered

Zimmer Biomet PESTLE Analysis

The Zimmer Biomet PESTLE Analysis provides a concise, professionally structured overview of political, economic, social, technological, legal, and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; the layout and content visible are the final file you can download immediately after checkout.