Zip Business Model Canvas

3-Page Business Model Canvas: Strategic Blueprint for Founders and Investors

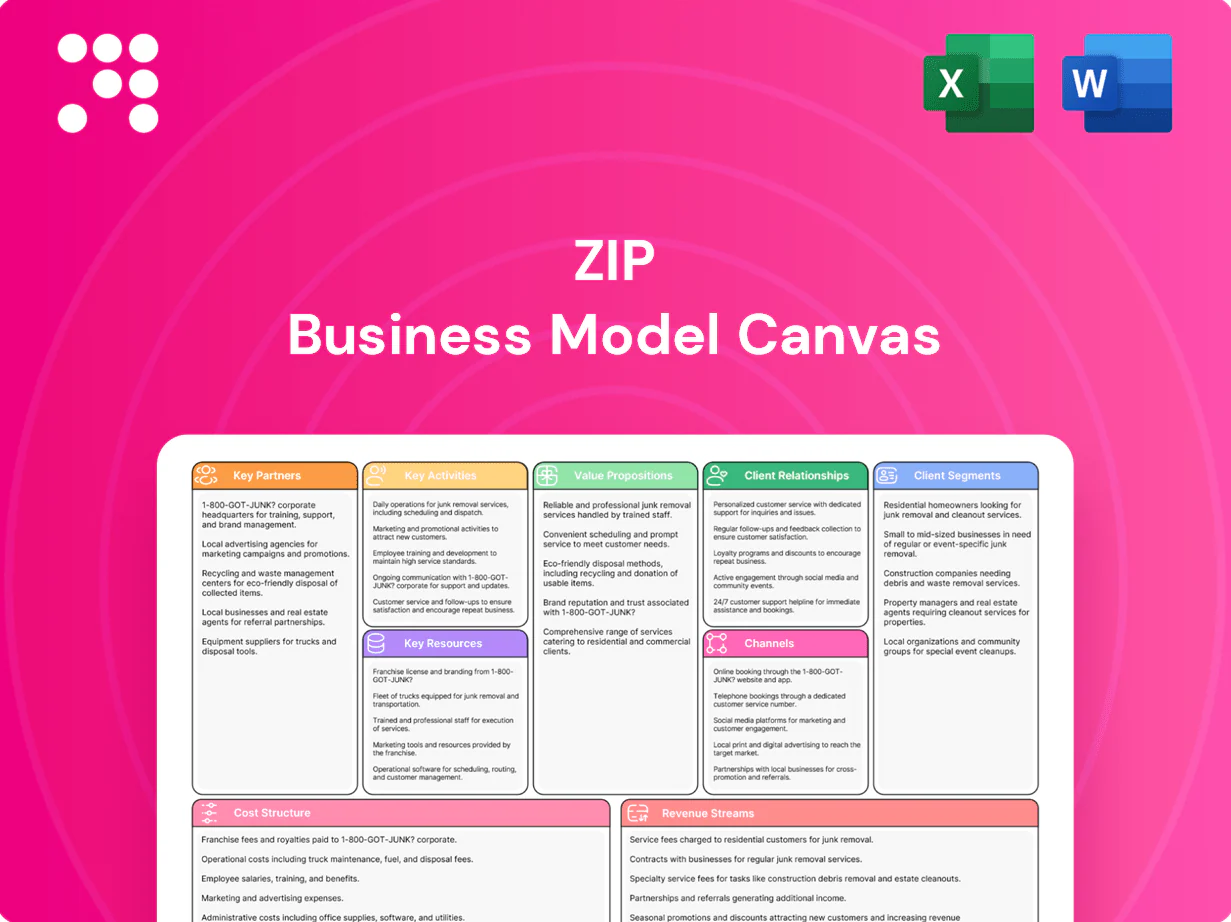

Unlock the full strategic blueprint behind Zip’s business model with our complete Business Model Canvas—three concise pages that reveal value propositions, customer segments, revenue streams and scaling levers. Perfect for entrepreneurs, investors, and strategists, this editable Word and Excel pack accelerates benchmarking and planning. Download the full canvas to turn insights into fast, actionable decisions.

Partnerships

Retail merchant alliances

Zip partners with online and brick-and-mortar retailers to embed BNPL at checkout, driving higher conversion rates (up to 25%) and average order value (AOV +30%) in industry studies. Co-marketing campaigns and exclusive merchant offers deepen engagement and repeat purchases. Contract terms define merchant fees, settlement timing and reserves, and dispute/chargeback handling to manage risk and cash flow.

Payment networks and gateways

Collaborations with processors, acquirers and gateways enable secure authorization and settlement, leveraging networks such as Visa which advertises capacity above 65,000 transactions per second to absorb peak loads. Network partnerships expand merchant acceptance and reduce friction across channels, while technical certification (PCI DSS, EMV) enforces uptime and latency targets typically aimed at 99.99% availability and sub-200ms auth latency. Cost optimization arises from volume-based pricing and intelligent routing, delivering double-digit per-transaction fee reductions for high-volume flows.

Banks and lending capital providers

Warehouse lines and facility partners fund receivables and enable rapid scaling, a core enabler for Zip's merchant and consumer growth in 2024. Banking partners deliver custodial, settlement and treasury services that underpin daily liquidity management. Covenants set risk limits and performance triggers to protect lenders. Diversified funding reduces cost of capital and concentration risk.

Fraud, data, and credit bureaus

Ties with major credit bureaus and alternative data providers (covering >300 million U.S. consumer records in 2024) enhance identity, income and risk assessments for Zip, while fraud vendors deliver device intelligence and behavioral analytics to detect account takeover and synthetic ID fraud. These inputs refine underwriting, reduce charge-offs, and ongoing feedback loops improve model precision.

- Data coverage: >300M U.S. records (2024)

- Fraud reduction: device intelligence, behavioral signals

- Outcome: tighter underwriting, lower charge-offs

- Loop: continuous feedback improves model accuracy

Regulatory and compliance advisors

Partnerships with legal, compliance and audit firms support Zip’s licensing and oversight needs and provide expert interpretation of evolving BNPL rules across Australia, the UK and the US as regulators intensified scrutiny in 2024.

Regular third-party reviews close gaps, align disclosures and collections with updated guidance, and have demonstrably reduced regulatory risk and penalties for major BNPL firms in 2024.

- Regulatory coverage: Australia, UK, US

- 2024: intensified regulatory scrutiny

- Outcomes: tighter disclosures, reduced penalty exposure

Merchant integrations: +25% conversion, +30% AOV; 99.99% uptime and >300M records

Zip leverages merchant integrations to boost checkout conversion (up to 25%) and AOV (+30%), while co-marketing and merchant fees structure drive repeat sales and revenue. Infrastructure partners (Visa, processors) support >99.99% uptime and sub-200ms auth targets to minimize friction. Data, fraud and funding partners (>300M US consumer records in 2024) tighten underwriting, lower charge-offs and support scaling.

| Partnership | 2024 metric | Impact |

|---|---|---|

| Merchants | Conversion +25% / AOV +30% | Revenue lift |

| Data/Fraud | >300M US records | Lower charge-offs |

| Processors | 99.99% uptime | Low latency |

What is included in the product

A polished, ready-to-use Business Model Canvas for Zip that maps nine BMC blocks into detailed customer segments, channels, value propositions, revenue streams and cost structure, reflects real-world operations, highlights competitive advantages and linked SWOT analysis, and is ideal for investor presentations, funding discussions, and strategic decision-making.

Streamlines mapping Zip's value proposition, revenue streams, and key partners into an editable one-page canvas, saving hours and clarifying strategic gaps for faster decision-making and team alignment.

Activities

Merchant integration and onboarding

Zip deploys APIs, plugins and SDKs to activate merchants quickly via its developer portal and ready-made ecommerce integrations. It runs end-to-end tests of checkout flows and settlement processes before go-live to ensure reconciliation accuracy. Training, operator playbooks and onboarding cohorts equip merchant teams for day-one operations. Continuous performance monitoring tracks conversion and settlement KPIs to hit commercial targets.

Risk underwriting and decisioning

Real-time scoring (sub-second) determines approval, limit assignment and terms, using transactional, device and bureau data in Zip's risk stack in 2024. Models ingest behavioral and payment-history signals to tailor limits and pricing. Champion-challenger testing continuously optimizes approval rates versus loss outcomes. Underwriting policies are adjusted dynamically to macro and portfolio trends.

Collections and receivables management

Automated reminders and tiered dunning schedules drive timely repayments, supporting Zip’s collections on total receivables of A$1.4 billion in FY2024 while limiting recoveries costs. Customer support teams handle hardship and disputes, resolving a growing share of cases via digital channels to preserve lifetime value. Loss mitigation balances recovery with brand reputation, with provisioning and capital needs informed by daily data feeds and a 3.2% impairment coverage metric.

Product development and UX optimization

Product development and UX optimization at Zip focuses on continuous improvement of checkout, app and wallet flows to reduce friction and lift conversion; Zip reported AUD 553m revenue and ~6.3m active customers in FY2024, underscoring scale benefits. Rigorous A/B testing refines messaging, repayment nudges and rewards, typically delivering double-digit uplift. Accessibility, localization and strong security/privacy controls expand reach and build trust.

Compliance, reporting, and partner management

Zip maintains AML, KYC and consumer protection frameworks across its Australia, UK, NZ and US operations, and in 2024 files quarterly regulatory and investor reports on performance and risk. Merchant success teams manage SLAs and bespoke growth plans; incident response, audits and remediation ensure adherence.

- AML/KYC scope: cross-border

- Reporting cadence: quarterly & annual (2024)

- Merchant SLAs & growth plans

- Incident response & audits

Embedded payments enable instant merchant onboarding; A$1.4bn receivables, 3.2% impairment

Zip accelerates merchant activation via APIs/SDKs and ecommerce plugins, with end-to-end testing and onboarding cohorts for day-one ops. Sub-second risk scoring and dynamic underwriting use behavioral, device and bureau data to tailor limits and pricing. Automated collections, digital support and provisioning manage A$1.4bn receivables and 3.2% impairment cover (FY2024).

| Metric | Value (FY2024) |

|---|---|

| Revenue | AUD 553m |

| Active customers | 6.3m |

| Receivables | A$1.4bn |

| Impairment cover | 3.2% |

Full Version Awaits

Business Model Canvas

The document previewed here is the exact Zip Business Model Canvas you’ll receive—no mockups or samples. After purchase you’ll download this same complete file, fully formatted and ready to edit in Word and Excel. No surprises, just the real deliverable.

3-Page Business Model Canvas: Strategic Blueprint for Founders and Investors

Unlock the full strategic blueprint behind Zip’s business model with our complete Business Model Canvas—three concise pages that reveal value propositions, customer segments, revenue streams and scaling levers. Perfect for entrepreneurs, investors, and strategists, this editable Word and Excel pack accelerates benchmarking and planning. Download the full canvas to turn insights into fast, actionable decisions.

Partnerships

Retail merchant alliances

Zip partners with online and brick-and-mortar retailers to embed BNPL at checkout, driving higher conversion rates (up to 25%) and average order value (AOV +30%) in industry studies. Co-marketing campaigns and exclusive merchant offers deepen engagement and repeat purchases. Contract terms define merchant fees, settlement timing and reserves, and dispute/chargeback handling to manage risk and cash flow.

Payment networks and gateways

Collaborations with processors, acquirers and gateways enable secure authorization and settlement, leveraging networks such as Visa which advertises capacity above 65,000 transactions per second to absorb peak loads. Network partnerships expand merchant acceptance and reduce friction across channels, while technical certification (PCI DSS, EMV) enforces uptime and latency targets typically aimed at 99.99% availability and sub-200ms auth latency. Cost optimization arises from volume-based pricing and intelligent routing, delivering double-digit per-transaction fee reductions for high-volume flows.

Banks and lending capital providers

Warehouse lines and facility partners fund receivables and enable rapid scaling, a core enabler for Zip's merchant and consumer growth in 2024. Banking partners deliver custodial, settlement and treasury services that underpin daily liquidity management. Covenants set risk limits and performance triggers to protect lenders. Diversified funding reduces cost of capital and concentration risk.

Fraud, data, and credit bureaus

Ties with major credit bureaus and alternative data providers (covering >300 million U.S. consumer records in 2024) enhance identity, income and risk assessments for Zip, while fraud vendors deliver device intelligence and behavioral analytics to detect account takeover and synthetic ID fraud. These inputs refine underwriting, reduce charge-offs, and ongoing feedback loops improve model precision.

- Data coverage: >300M U.S. records (2024)

- Fraud reduction: device intelligence, behavioral signals

- Outcome: tighter underwriting, lower charge-offs

- Loop: continuous feedback improves model accuracy

Regulatory and compliance advisors

Partnerships with legal, compliance and audit firms support Zip’s licensing and oversight needs and provide expert interpretation of evolving BNPL rules across Australia, the UK and the US as regulators intensified scrutiny in 2024.

Regular third-party reviews close gaps, align disclosures and collections with updated guidance, and have demonstrably reduced regulatory risk and penalties for major BNPL firms in 2024.

- Regulatory coverage: Australia, UK, US

- 2024: intensified regulatory scrutiny

- Outcomes: tighter disclosures, reduced penalty exposure

Merchant integrations: +25% conversion, +30% AOV; 99.99% uptime and >300M records

Zip leverages merchant integrations to boost checkout conversion (up to 25%) and AOV (+30%), while co-marketing and merchant fees structure drive repeat sales and revenue. Infrastructure partners (Visa, processors) support >99.99% uptime and sub-200ms auth targets to minimize friction. Data, fraud and funding partners (>300M US consumer records in 2024) tighten underwriting, lower charge-offs and support scaling.

| Partnership | 2024 metric | Impact |

|---|---|---|

| Merchants | Conversion +25% / AOV +30% | Revenue lift |

| Data/Fraud | >300M US records | Lower charge-offs |

| Processors | 99.99% uptime | Low latency |

What is included in the product

A polished, ready-to-use Business Model Canvas for Zip that maps nine BMC blocks into detailed customer segments, channels, value propositions, revenue streams and cost structure, reflects real-world operations, highlights competitive advantages and linked SWOT analysis, and is ideal for investor presentations, funding discussions, and strategic decision-making.

Streamlines mapping Zip's value proposition, revenue streams, and key partners into an editable one-page canvas, saving hours and clarifying strategic gaps for faster decision-making and team alignment.

Activities

Merchant integration and onboarding

Zip deploys APIs, plugins and SDKs to activate merchants quickly via its developer portal and ready-made ecommerce integrations. It runs end-to-end tests of checkout flows and settlement processes before go-live to ensure reconciliation accuracy. Training, operator playbooks and onboarding cohorts equip merchant teams for day-one operations. Continuous performance monitoring tracks conversion and settlement KPIs to hit commercial targets.

Risk underwriting and decisioning

Real-time scoring (sub-second) determines approval, limit assignment and terms, using transactional, device and bureau data in Zip's risk stack in 2024. Models ingest behavioral and payment-history signals to tailor limits and pricing. Champion-challenger testing continuously optimizes approval rates versus loss outcomes. Underwriting policies are adjusted dynamically to macro and portfolio trends.

Collections and receivables management

Automated reminders and tiered dunning schedules drive timely repayments, supporting Zip’s collections on total receivables of A$1.4 billion in FY2024 while limiting recoveries costs. Customer support teams handle hardship and disputes, resolving a growing share of cases via digital channels to preserve lifetime value. Loss mitigation balances recovery with brand reputation, with provisioning and capital needs informed by daily data feeds and a 3.2% impairment coverage metric.

Product development and UX optimization

Product development and UX optimization at Zip focuses on continuous improvement of checkout, app and wallet flows to reduce friction and lift conversion; Zip reported AUD 553m revenue and ~6.3m active customers in FY2024, underscoring scale benefits. Rigorous A/B testing refines messaging, repayment nudges and rewards, typically delivering double-digit uplift. Accessibility, localization and strong security/privacy controls expand reach and build trust.

Compliance, reporting, and partner management

Zip maintains AML, KYC and consumer protection frameworks across its Australia, UK, NZ and US operations, and in 2024 files quarterly regulatory and investor reports on performance and risk. Merchant success teams manage SLAs and bespoke growth plans; incident response, audits and remediation ensure adherence.

- AML/KYC scope: cross-border

- Reporting cadence: quarterly & annual (2024)

- Merchant SLAs & growth plans

- Incident response & audits

Embedded payments enable instant merchant onboarding; A$1.4bn receivables, 3.2% impairment

Zip accelerates merchant activation via APIs/SDKs and ecommerce plugins, with end-to-end testing and onboarding cohorts for day-one ops. Sub-second risk scoring and dynamic underwriting use behavioral, device and bureau data to tailor limits and pricing. Automated collections, digital support and provisioning manage A$1.4bn receivables and 3.2% impairment cover (FY2024).

| Metric | Value (FY2024) |

|---|---|

| Revenue | AUD 553m |

| Active customers | 6.3m |

| Receivables | A$1.4bn |

| Impairment cover | 3.2% |

Full Version Awaits

Business Model Canvas

The document previewed here is the exact Zip Business Model Canvas you’ll receive—no mockups or samples. After purchase you’ll download this same complete file, fully formatted and ready to edit in Word and Excel. No surprises, just the real deliverable.

Description

3-Page Business Model Canvas: Strategic Blueprint for Founders and Investors

Unlock the full strategic blueprint behind Zip’s business model with our complete Business Model Canvas—three concise pages that reveal value propositions, customer segments, revenue streams and scaling levers. Perfect for entrepreneurs, investors, and strategists, this editable Word and Excel pack accelerates benchmarking and planning. Download the full canvas to turn insights into fast, actionable decisions.

Partnerships

Retail merchant alliances

Zip partners with online and brick-and-mortar retailers to embed BNPL at checkout, driving higher conversion rates (up to 25%) and average order value (AOV +30%) in industry studies. Co-marketing campaigns and exclusive merchant offers deepen engagement and repeat purchases. Contract terms define merchant fees, settlement timing and reserves, and dispute/chargeback handling to manage risk and cash flow.

Payment networks and gateways

Collaborations with processors, acquirers and gateways enable secure authorization and settlement, leveraging networks such as Visa which advertises capacity above 65,000 transactions per second to absorb peak loads. Network partnerships expand merchant acceptance and reduce friction across channels, while technical certification (PCI DSS, EMV) enforces uptime and latency targets typically aimed at 99.99% availability and sub-200ms auth latency. Cost optimization arises from volume-based pricing and intelligent routing, delivering double-digit per-transaction fee reductions for high-volume flows.

Banks and lending capital providers

Warehouse lines and facility partners fund receivables and enable rapid scaling, a core enabler for Zip's merchant and consumer growth in 2024. Banking partners deliver custodial, settlement and treasury services that underpin daily liquidity management. Covenants set risk limits and performance triggers to protect lenders. Diversified funding reduces cost of capital and concentration risk.

Fraud, data, and credit bureaus

Ties with major credit bureaus and alternative data providers (covering >300 million U.S. consumer records in 2024) enhance identity, income and risk assessments for Zip, while fraud vendors deliver device intelligence and behavioral analytics to detect account takeover and synthetic ID fraud. These inputs refine underwriting, reduce charge-offs, and ongoing feedback loops improve model precision.

- Data coverage: >300M U.S. records (2024)

- Fraud reduction: device intelligence, behavioral signals

- Outcome: tighter underwriting, lower charge-offs

- Loop: continuous feedback improves model accuracy

Regulatory and compliance advisors

Partnerships with legal, compliance and audit firms support Zip’s licensing and oversight needs and provide expert interpretation of evolving BNPL rules across Australia, the UK and the US as regulators intensified scrutiny in 2024.

Regular third-party reviews close gaps, align disclosures and collections with updated guidance, and have demonstrably reduced regulatory risk and penalties for major BNPL firms in 2024.

- Regulatory coverage: Australia, UK, US

- 2024: intensified regulatory scrutiny

- Outcomes: tighter disclosures, reduced penalty exposure

Merchant integrations: +25% conversion, +30% AOV; 99.99% uptime and >300M records

Zip leverages merchant integrations to boost checkout conversion (up to 25%) and AOV (+30%), while co-marketing and merchant fees structure drive repeat sales and revenue. Infrastructure partners (Visa, processors) support >99.99% uptime and sub-200ms auth targets to minimize friction. Data, fraud and funding partners (>300M US consumer records in 2024) tighten underwriting, lower charge-offs and support scaling.

| Partnership | 2024 metric | Impact |

|---|---|---|

| Merchants | Conversion +25% / AOV +30% | Revenue lift |

| Data/Fraud | >300M US records | Lower charge-offs |

| Processors | 99.99% uptime | Low latency |

What is included in the product

A polished, ready-to-use Business Model Canvas for Zip that maps nine BMC blocks into detailed customer segments, channels, value propositions, revenue streams and cost structure, reflects real-world operations, highlights competitive advantages and linked SWOT analysis, and is ideal for investor presentations, funding discussions, and strategic decision-making.

Streamlines mapping Zip's value proposition, revenue streams, and key partners into an editable one-page canvas, saving hours and clarifying strategic gaps for faster decision-making and team alignment.

Activities

Merchant integration and onboarding

Zip deploys APIs, plugins and SDKs to activate merchants quickly via its developer portal and ready-made ecommerce integrations. It runs end-to-end tests of checkout flows and settlement processes before go-live to ensure reconciliation accuracy. Training, operator playbooks and onboarding cohorts equip merchant teams for day-one operations. Continuous performance monitoring tracks conversion and settlement KPIs to hit commercial targets.

Risk underwriting and decisioning

Real-time scoring (sub-second) determines approval, limit assignment and terms, using transactional, device and bureau data in Zip's risk stack in 2024. Models ingest behavioral and payment-history signals to tailor limits and pricing. Champion-challenger testing continuously optimizes approval rates versus loss outcomes. Underwriting policies are adjusted dynamically to macro and portfolio trends.

Collections and receivables management

Automated reminders and tiered dunning schedules drive timely repayments, supporting Zip’s collections on total receivables of A$1.4 billion in FY2024 while limiting recoveries costs. Customer support teams handle hardship and disputes, resolving a growing share of cases via digital channels to preserve lifetime value. Loss mitigation balances recovery with brand reputation, with provisioning and capital needs informed by daily data feeds and a 3.2% impairment coverage metric.

Product development and UX optimization

Product development and UX optimization at Zip focuses on continuous improvement of checkout, app and wallet flows to reduce friction and lift conversion; Zip reported AUD 553m revenue and ~6.3m active customers in FY2024, underscoring scale benefits. Rigorous A/B testing refines messaging, repayment nudges and rewards, typically delivering double-digit uplift. Accessibility, localization and strong security/privacy controls expand reach and build trust.

Compliance, reporting, and partner management

Zip maintains AML, KYC and consumer protection frameworks across its Australia, UK, NZ and US operations, and in 2024 files quarterly regulatory and investor reports on performance and risk. Merchant success teams manage SLAs and bespoke growth plans; incident response, audits and remediation ensure adherence.

- AML/KYC scope: cross-border

- Reporting cadence: quarterly & annual (2024)

- Merchant SLAs & growth plans

- Incident response & audits

Embedded payments enable instant merchant onboarding; A$1.4bn receivables, 3.2% impairment

Zip accelerates merchant activation via APIs/SDKs and ecommerce plugins, with end-to-end testing and onboarding cohorts for day-one ops. Sub-second risk scoring and dynamic underwriting use behavioral, device and bureau data to tailor limits and pricing. Automated collections, digital support and provisioning manage A$1.4bn receivables and 3.2% impairment cover (FY2024).

| Metric | Value (FY2024) |

|---|---|

| Revenue | AUD 553m |

| Active customers | 6.3m |

| Receivables | A$1.4bn |

| Impairment cover | 3.2% |

Full Version Awaits

Business Model Canvas

The document previewed here is the exact Zip Business Model Canvas you’ll receive—no mockups or samples. After purchase you’ll download this same complete file, fully formatted and ready to edit in Word and Excel. No surprises, just the real deliverable.