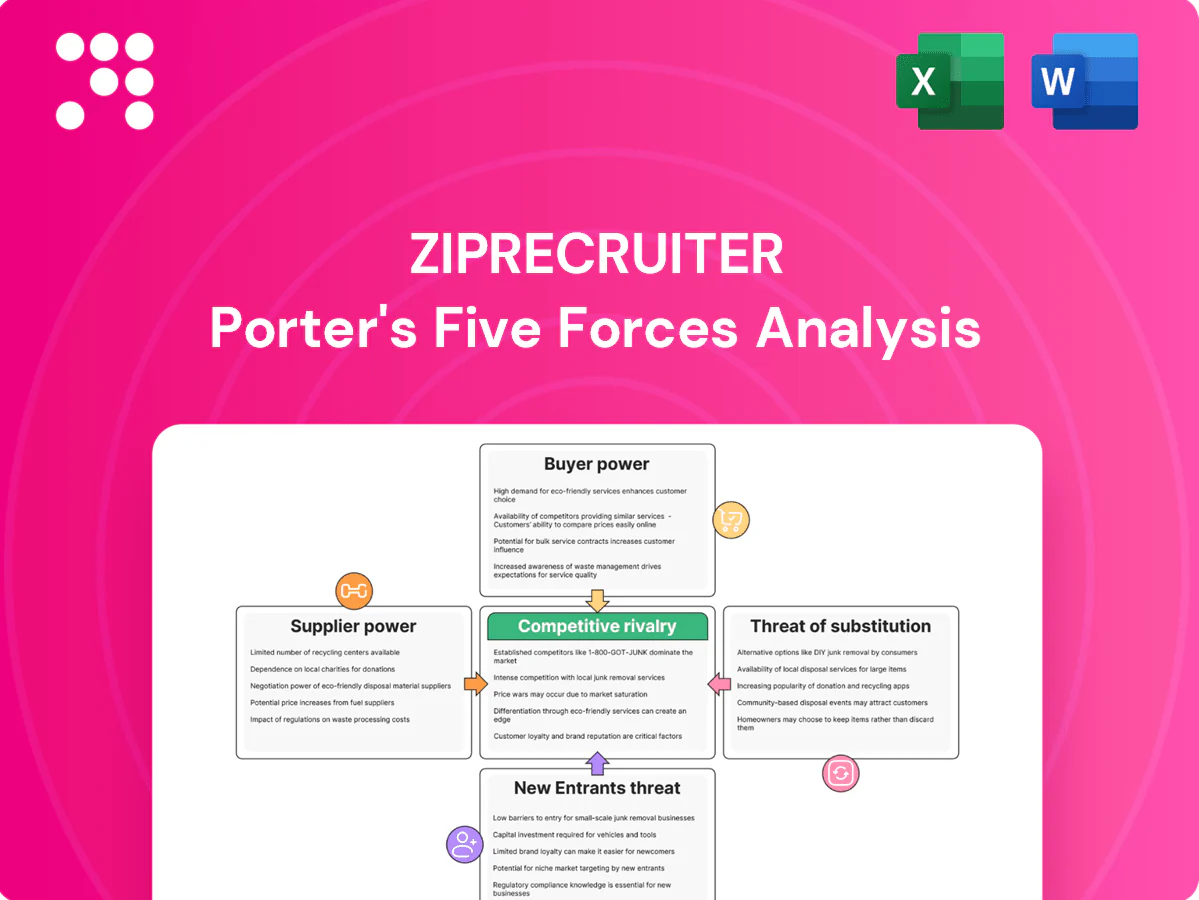

ZipRecruiter Porter's Five Forces Analysis

Don't Miss the Bigger Picture

ZipRecruiter faces intense buyer power, moderate supplier leverage, notable threats from substitutes and new entrants, and competitive rivalry shaped by network effects and pricing pressure. This snapshot highlights key dynamics but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications tailored to ZipRecruiter.

Suppliers Bargaining Power

Concentrated traffic partners

ZipRecruiter depends on major job boards and aggregators for distribution, creating pockets of supplier leverage over candidate reach. Dominant partners such as Indeed and Google—Indeed commands roughly 50% of US job-search traffic—can press for favorable rev-share, placement, or data terms. Renegotiations or delistings can spike acquisition costs and lower fill rates; diversifying channels and building proprietary audiences reduce but do not eliminate this risk.

Search engine dependence

ZipRecruiter depends heavily on search, with Google holding roughly 92% of global search market share in 2024 (StatCounter); Google for Jobs and SEM/SEO controls core lead channels, so algorithm or policy shifts can sharply reduce lead flow and worsen unit economics. Intense bidding on job keywords pushes CPCs among classifieds highest in search, and brand/direct traffic mitigates but cannot fully replace this dependency.

Cloud and AI infrastructure

Hosting, compute and AI tooling vendors (hyperscalers and model providers) materially affect ZipRecruiter’s cost and performance; AWS, Azure and GCP held about 32%, 23% and 11% cloud market share in 2024, concentrating leverage. Usage-based pricing makes margins sensitive to volume spikes. Switching is costly due to architecture lock-in and tuning, while long-term contracts and multi-vendor strategies can reduce supplier power.

Data and identity providers

Data and identity providers for background checks, enrichment, and verification are specialized and not easily substitutable; as of 2024 Checkr and Sterling remain dominant in the US market. Quality and coverage directly affect match accuracy and employer satisfaction, and vendors can raise prices or restrict data rights, limiting feature rollouts. Contractual data rights and building internal datasets reduce dependency and preserve product control.

- Dependency: high

- Key vendors: Checkr, Sterling (2024)

- Risk: price/data restrictions

- Mitigation: contracts + internal data

Payment and communication rails

Payment processors and messaging/email providers set fees (card rates ~1.5–3.5% plus $0.10–$0.30 per tx) and compliance rules that shape ZipRecruiter conversion; email deliverability runs ~85–95% with open rates ~20–25% and SMS deliverability >95%, while fraud controls directly reduce engagement and hires. Vendor outages or policy shifts can halt workflows; negotiated volume discounts can cut costs up to ~30% but do not eliminate supplier leverage.

- fees: card 1.5–3.5% + $0.10–$0.30 per tx

- email deliverability: 85–95%; open rate ~20–25%

- SMS deliverability: >95%

- volume discounts: up to ~30%

- outages/policy shifts = workflow risk

Platform dominance (~92% search, ~50% job traffic) squeezes margins

Supplier power is high: distribution partners (Indeed ~50% US job search) and Google (search ~92% global, 2024) can extract fees or change policies, raising CAC and reducing fills. Cloud hyperscalers (AWS 32%, Azure 23%, GCP 11% 2024) and AI providers drive cost volatility via usage pricing and lock-in. Niche data/verification vendors (Checkr, Sterling) and payment processors (card fees ~1.5–3.5%) further constrain margins; contracts and internal datasets mitigate risk.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Indeed | ~50% US job traffic | High pricing leverage |

| ~92% global search | Lead risk from algo changes | |

| AWS/Azure/GCP | 32%/23%/11% | Cost sensitivity, lock-in |

| Checkr/Sterling | Market leaders | Data/feature constraints |

| Payments | 1.5–3.5% + $0.10–0.30 | Conversion cost |

What is included in the product

Tailored Porter's Five Forces analysis for ZipRecruiter that uncovers competitive drivers, buyer and supplier power, substitution risks, and entry barriers, highlighting disruptive threats, market dynamics protecting incumbents, and strategic implications for pricing, profitability, and growth.

Clear, one-sheet Porter's Five Forces for ZipRecruiter that pinpoints hiring-market pressures and strategic pain points, with customizable pressure levels and an instant spider chart—ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Low switching costs for employers

Employers can post across platforms with minimal friction—LinkedIn reports 930 million members and Indeed exceeds 250 million monthly visitors—so many buyers list broadly, increasing bargaining power. Price and feature comparisons are transparent and programmatic buying, which accounts for over 80% of display ad spend, lets buyers optimize spend across channels. ZipRecruiter must therefore compete on performance guarantees, measurable ROI, and deep integrations to retain employer spend.

Demand cyclicality

Hiring volumes fluctuate with macro conditions—U.S. unemployment averaged about 3.9% in 2024 (BLS), giving buyers budget leverage in downturns when vacancies fall. During slowdowns customers consolidate vendors and push discounts, while tight labor markets force demands for faster time-to-fill and higher-quality matches. Flexible pricing and outcome-based models align ZipRecruiter with these shifting buyer expectations.

Enterprise negotiation leverage

Larger employers extract custom pricing, SLAs and data-rights from ZipRecruiter, often via multi-year contracts that compress unit economics in exchange for volume; large-account deals can represent a disproportionate share of revenue and renewal risk. Buyers routinely demand ATS and HRIS integrations, shifting implementation and maintenance costs to the vendor. Robust case studies and measured hiring outcomes help ZipRecruiter counteract procurement pressure and preserve margin.

Multi-homing behavior

Employers frequently multi-home across job boards and networks (LinkedIn exceeds 930 million members), reducing dependence on any single platform and increasing price sensitivity; performance-attribution tools let buyers reallocate spend rapidly, pressuring ROI. To defend share, ZipRecruiter must prove incremental, not duplicative, candidate delivery.

- Multi-homing: common

- Price sensitivity: higher

- Attribution: faster reallocations

- Defense: incremental candidates

Outcome expectations

Buyers increasingly prioritize qualified applicants and time-to-hire over clicks or views; a 2024 HR survey found roughly 68% of employers rank applicant quality as top purchase criterion, and marketing spend shifts rapidly when quality dips. Guarantees, refunds or performance pricing raise buyer power but can build trust and lower churn. Robust analytics and AI matching must consistently deliver measurable hiring outcomes to justify spend.

- Buyer priority: applicant quality > views (2024: ~68%)

- Spend sensitivity: rapid reallocation if quality falls

- Pricing levers: guarantees/refunds increase buyer leverage

- Outcome demand: analytics/AI must show measurable hires

Networks 930M, portals 250M, programmatic > 80%, unemployment 3.9%

Employers list broadly across LinkedIn (930M members) and Indeed (~250M monthly visitors), raising buyer leverage. Programmatic buying (>80% display ad spend) and attribution enable rapid reallocation, increasing price sensitivity. 2024 U.S. unemployment ~3.9% (BLS) shifts bargaining power with cycles; 68% of employers prioritize applicant quality, pressing performance guarantees.

| Metric | 2024 |

|---|---|

| LinkedIn users | 930M |

| Indeed monthly visitors | ~250M |

| Programmatic display spend | >80% |

| US unemployment | 3.9% |

| Employers prioritizing quality | 68% |

What You See Is What You Get

ZipRecruiter Porter's Five Forces Analysis

This preview shows the exact ZipRecruiter Porter’s Five Forces analysis you'll receive upon purchase—fully formatted, professionally written, and ready to download. No placeholders or samples: the file available immediately after payment is identical to this preview. Use it right away for strategic insights, competitive assessment, and decision-making without any further setup.

Don't Miss the Bigger Picture

ZipRecruiter faces intense buyer power, moderate supplier leverage, notable threats from substitutes and new entrants, and competitive rivalry shaped by network effects and pricing pressure. This snapshot highlights key dynamics but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications tailored to ZipRecruiter.

Suppliers Bargaining Power

Concentrated traffic partners

ZipRecruiter depends on major job boards and aggregators for distribution, creating pockets of supplier leverage over candidate reach. Dominant partners such as Indeed and Google—Indeed commands roughly 50% of US job-search traffic—can press for favorable rev-share, placement, or data terms. Renegotiations or delistings can spike acquisition costs and lower fill rates; diversifying channels and building proprietary audiences reduce but do not eliminate this risk.

Search engine dependence

ZipRecruiter depends heavily on search, with Google holding roughly 92% of global search market share in 2024 (StatCounter); Google for Jobs and SEM/SEO controls core lead channels, so algorithm or policy shifts can sharply reduce lead flow and worsen unit economics. Intense bidding on job keywords pushes CPCs among classifieds highest in search, and brand/direct traffic mitigates but cannot fully replace this dependency.

Cloud and AI infrastructure

Hosting, compute and AI tooling vendors (hyperscalers and model providers) materially affect ZipRecruiter’s cost and performance; AWS, Azure and GCP held about 32%, 23% and 11% cloud market share in 2024, concentrating leverage. Usage-based pricing makes margins sensitive to volume spikes. Switching is costly due to architecture lock-in and tuning, while long-term contracts and multi-vendor strategies can reduce supplier power.

Data and identity providers

Data and identity providers for background checks, enrichment, and verification are specialized and not easily substitutable; as of 2024 Checkr and Sterling remain dominant in the US market. Quality and coverage directly affect match accuracy and employer satisfaction, and vendors can raise prices or restrict data rights, limiting feature rollouts. Contractual data rights and building internal datasets reduce dependency and preserve product control.

- Dependency: high

- Key vendors: Checkr, Sterling (2024)

- Risk: price/data restrictions

- Mitigation: contracts + internal data

Payment and communication rails

Payment processors and messaging/email providers set fees (card rates ~1.5–3.5% plus $0.10–$0.30 per tx) and compliance rules that shape ZipRecruiter conversion; email deliverability runs ~85–95% with open rates ~20–25% and SMS deliverability >95%, while fraud controls directly reduce engagement and hires. Vendor outages or policy shifts can halt workflows; negotiated volume discounts can cut costs up to ~30% but do not eliminate supplier leverage.

- fees: card 1.5–3.5% + $0.10–$0.30 per tx

- email deliverability: 85–95%; open rate ~20–25%

- SMS deliverability: >95%

- volume discounts: up to ~30%

- outages/policy shifts = workflow risk

Platform dominance (~92% search, ~50% job traffic) squeezes margins

Supplier power is high: distribution partners (Indeed ~50% US job search) and Google (search ~92% global, 2024) can extract fees or change policies, raising CAC and reducing fills. Cloud hyperscalers (AWS 32%, Azure 23%, GCP 11% 2024) and AI providers drive cost volatility via usage pricing and lock-in. Niche data/verification vendors (Checkr, Sterling) and payment processors (card fees ~1.5–3.5%) further constrain margins; contracts and internal datasets mitigate risk.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Indeed | ~50% US job traffic | High pricing leverage |

| ~92% global search | Lead risk from algo changes | |

| AWS/Azure/GCP | 32%/23%/11% | Cost sensitivity, lock-in |

| Checkr/Sterling | Market leaders | Data/feature constraints |

| Payments | 1.5–3.5% + $0.10–0.30 | Conversion cost |

What is included in the product

Tailored Porter's Five Forces analysis for ZipRecruiter that uncovers competitive drivers, buyer and supplier power, substitution risks, and entry barriers, highlighting disruptive threats, market dynamics protecting incumbents, and strategic implications for pricing, profitability, and growth.

Clear, one-sheet Porter's Five Forces for ZipRecruiter that pinpoints hiring-market pressures and strategic pain points, with customizable pressure levels and an instant spider chart—ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Low switching costs for employers

Employers can post across platforms with minimal friction—LinkedIn reports 930 million members and Indeed exceeds 250 million monthly visitors—so many buyers list broadly, increasing bargaining power. Price and feature comparisons are transparent and programmatic buying, which accounts for over 80% of display ad spend, lets buyers optimize spend across channels. ZipRecruiter must therefore compete on performance guarantees, measurable ROI, and deep integrations to retain employer spend.

Demand cyclicality

Hiring volumes fluctuate with macro conditions—U.S. unemployment averaged about 3.9% in 2024 (BLS), giving buyers budget leverage in downturns when vacancies fall. During slowdowns customers consolidate vendors and push discounts, while tight labor markets force demands for faster time-to-fill and higher-quality matches. Flexible pricing and outcome-based models align ZipRecruiter with these shifting buyer expectations.

Enterprise negotiation leverage

Larger employers extract custom pricing, SLAs and data-rights from ZipRecruiter, often via multi-year contracts that compress unit economics in exchange for volume; large-account deals can represent a disproportionate share of revenue and renewal risk. Buyers routinely demand ATS and HRIS integrations, shifting implementation and maintenance costs to the vendor. Robust case studies and measured hiring outcomes help ZipRecruiter counteract procurement pressure and preserve margin.

Multi-homing behavior

Employers frequently multi-home across job boards and networks (LinkedIn exceeds 930 million members), reducing dependence on any single platform and increasing price sensitivity; performance-attribution tools let buyers reallocate spend rapidly, pressuring ROI. To defend share, ZipRecruiter must prove incremental, not duplicative, candidate delivery.

- Multi-homing: common

- Price sensitivity: higher

- Attribution: faster reallocations

- Defense: incremental candidates

Outcome expectations

Buyers increasingly prioritize qualified applicants and time-to-hire over clicks or views; a 2024 HR survey found roughly 68% of employers rank applicant quality as top purchase criterion, and marketing spend shifts rapidly when quality dips. Guarantees, refunds or performance pricing raise buyer power but can build trust and lower churn. Robust analytics and AI matching must consistently deliver measurable hiring outcomes to justify spend.

- Buyer priority: applicant quality > views (2024: ~68%)

- Spend sensitivity: rapid reallocation if quality falls

- Pricing levers: guarantees/refunds increase buyer leverage

- Outcome demand: analytics/AI must show measurable hires

Networks 930M, portals 250M, programmatic > 80%, unemployment 3.9%

Employers list broadly across LinkedIn (930M members) and Indeed (~250M monthly visitors), raising buyer leverage. Programmatic buying (>80% display ad spend) and attribution enable rapid reallocation, increasing price sensitivity. 2024 U.S. unemployment ~3.9% (BLS) shifts bargaining power with cycles; 68% of employers prioritize applicant quality, pressing performance guarantees.

| Metric | 2024 |

|---|---|

| LinkedIn users | 930M |

| Indeed monthly visitors | ~250M |

| Programmatic display spend | >80% |

| US unemployment | 3.9% |

| Employers prioritizing quality | 68% |

What You See Is What You Get

ZipRecruiter Porter's Five Forces Analysis

This preview shows the exact ZipRecruiter Porter’s Five Forces analysis you'll receive upon purchase—fully formatted, professionally written, and ready to download. No placeholders or samples: the file available immediately after payment is identical to this preview. Use it right away for strategic insights, competitive assessment, and decision-making without any further setup.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

ZipRecruiter faces intense buyer power, moderate supplier leverage, notable threats from substitutes and new entrants, and competitive rivalry shaped by network effects and pricing pressure. This snapshot highlights key dynamics but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications tailored to ZipRecruiter.

Suppliers Bargaining Power

Concentrated traffic partners

ZipRecruiter depends on major job boards and aggregators for distribution, creating pockets of supplier leverage over candidate reach. Dominant partners such as Indeed and Google—Indeed commands roughly 50% of US job-search traffic—can press for favorable rev-share, placement, or data terms. Renegotiations or delistings can spike acquisition costs and lower fill rates; diversifying channels and building proprietary audiences reduce but do not eliminate this risk.

Search engine dependence

ZipRecruiter depends heavily on search, with Google holding roughly 92% of global search market share in 2024 (StatCounter); Google for Jobs and SEM/SEO controls core lead channels, so algorithm or policy shifts can sharply reduce lead flow and worsen unit economics. Intense bidding on job keywords pushes CPCs among classifieds highest in search, and brand/direct traffic mitigates but cannot fully replace this dependency.

Cloud and AI infrastructure

Hosting, compute and AI tooling vendors (hyperscalers and model providers) materially affect ZipRecruiter’s cost and performance; AWS, Azure and GCP held about 32%, 23% and 11% cloud market share in 2024, concentrating leverage. Usage-based pricing makes margins sensitive to volume spikes. Switching is costly due to architecture lock-in and tuning, while long-term contracts and multi-vendor strategies can reduce supplier power.

Data and identity providers

Data and identity providers for background checks, enrichment, and verification are specialized and not easily substitutable; as of 2024 Checkr and Sterling remain dominant in the US market. Quality and coverage directly affect match accuracy and employer satisfaction, and vendors can raise prices or restrict data rights, limiting feature rollouts. Contractual data rights and building internal datasets reduce dependency and preserve product control.

- Dependency: high

- Key vendors: Checkr, Sterling (2024)

- Risk: price/data restrictions

- Mitigation: contracts + internal data

Payment and communication rails

Payment processors and messaging/email providers set fees (card rates ~1.5–3.5% plus $0.10–$0.30 per tx) and compliance rules that shape ZipRecruiter conversion; email deliverability runs ~85–95% with open rates ~20–25% and SMS deliverability >95%, while fraud controls directly reduce engagement and hires. Vendor outages or policy shifts can halt workflows; negotiated volume discounts can cut costs up to ~30% but do not eliminate supplier leverage.

- fees: card 1.5–3.5% + $0.10–$0.30 per tx

- email deliverability: 85–95%; open rate ~20–25%

- SMS deliverability: >95%

- volume discounts: up to ~30%

- outages/policy shifts = workflow risk

Platform dominance (~92% search, ~50% job traffic) squeezes margins

Supplier power is high: distribution partners (Indeed ~50% US job search) and Google (search ~92% global, 2024) can extract fees or change policies, raising CAC and reducing fills. Cloud hyperscalers (AWS 32%, Azure 23%, GCP 11% 2024) and AI providers drive cost volatility via usage pricing and lock-in. Niche data/verification vendors (Checkr, Sterling) and payment processors (card fees ~1.5–3.5%) further constrain margins; contracts and internal datasets mitigate risk.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Indeed | ~50% US job traffic | High pricing leverage |

| ~92% global search | Lead risk from algo changes | |

| AWS/Azure/GCP | 32%/23%/11% | Cost sensitivity, lock-in |

| Checkr/Sterling | Market leaders | Data/feature constraints |

| Payments | 1.5–3.5% + $0.10–0.30 | Conversion cost |

What is included in the product

Tailored Porter's Five Forces analysis for ZipRecruiter that uncovers competitive drivers, buyer and supplier power, substitution risks, and entry barriers, highlighting disruptive threats, market dynamics protecting incumbents, and strategic implications for pricing, profitability, and growth.

Clear, one-sheet Porter's Five Forces for ZipRecruiter that pinpoints hiring-market pressures and strategic pain points, with customizable pressure levels and an instant spider chart—ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Low switching costs for employers

Employers can post across platforms with minimal friction—LinkedIn reports 930 million members and Indeed exceeds 250 million monthly visitors—so many buyers list broadly, increasing bargaining power. Price and feature comparisons are transparent and programmatic buying, which accounts for over 80% of display ad spend, lets buyers optimize spend across channels. ZipRecruiter must therefore compete on performance guarantees, measurable ROI, and deep integrations to retain employer spend.

Demand cyclicality

Hiring volumes fluctuate with macro conditions—U.S. unemployment averaged about 3.9% in 2024 (BLS), giving buyers budget leverage in downturns when vacancies fall. During slowdowns customers consolidate vendors and push discounts, while tight labor markets force demands for faster time-to-fill and higher-quality matches. Flexible pricing and outcome-based models align ZipRecruiter with these shifting buyer expectations.

Enterprise negotiation leverage

Larger employers extract custom pricing, SLAs and data-rights from ZipRecruiter, often via multi-year contracts that compress unit economics in exchange for volume; large-account deals can represent a disproportionate share of revenue and renewal risk. Buyers routinely demand ATS and HRIS integrations, shifting implementation and maintenance costs to the vendor. Robust case studies and measured hiring outcomes help ZipRecruiter counteract procurement pressure and preserve margin.

Multi-homing behavior

Employers frequently multi-home across job boards and networks (LinkedIn exceeds 930 million members), reducing dependence on any single platform and increasing price sensitivity; performance-attribution tools let buyers reallocate spend rapidly, pressuring ROI. To defend share, ZipRecruiter must prove incremental, not duplicative, candidate delivery.

- Multi-homing: common

- Price sensitivity: higher

- Attribution: faster reallocations

- Defense: incremental candidates

Outcome expectations

Buyers increasingly prioritize qualified applicants and time-to-hire over clicks or views; a 2024 HR survey found roughly 68% of employers rank applicant quality as top purchase criterion, and marketing spend shifts rapidly when quality dips. Guarantees, refunds or performance pricing raise buyer power but can build trust and lower churn. Robust analytics and AI matching must consistently deliver measurable hiring outcomes to justify spend.

- Buyer priority: applicant quality > views (2024: ~68%)

- Spend sensitivity: rapid reallocation if quality falls

- Pricing levers: guarantees/refunds increase buyer leverage

- Outcome demand: analytics/AI must show measurable hires

Networks 930M, portals 250M, programmatic > 80%, unemployment 3.9%

Employers list broadly across LinkedIn (930M members) and Indeed (~250M monthly visitors), raising buyer leverage. Programmatic buying (>80% display ad spend) and attribution enable rapid reallocation, increasing price sensitivity. 2024 U.S. unemployment ~3.9% (BLS) shifts bargaining power with cycles; 68% of employers prioritize applicant quality, pressing performance guarantees.

| Metric | 2024 |

|---|---|

| LinkedIn users | 930M |

| Indeed monthly visitors | ~250M |

| Programmatic display spend | >80% |

| US unemployment | 3.9% |

| Employers prioritizing quality | 68% |

What You See Is What You Get

ZipRecruiter Porter's Five Forces Analysis

This preview shows the exact ZipRecruiter Porter’s Five Forces analysis you'll receive upon purchase—fully formatted, professionally written, and ready to download. No placeholders or samples: the file available immediately after payment is identical to this preview. Use it right away for strategic insights, competitive assessment, and decision-making without any further setup.