Zhongliang Holdings Porter's Five Forces Analysis

Don't Miss the Bigger Picture

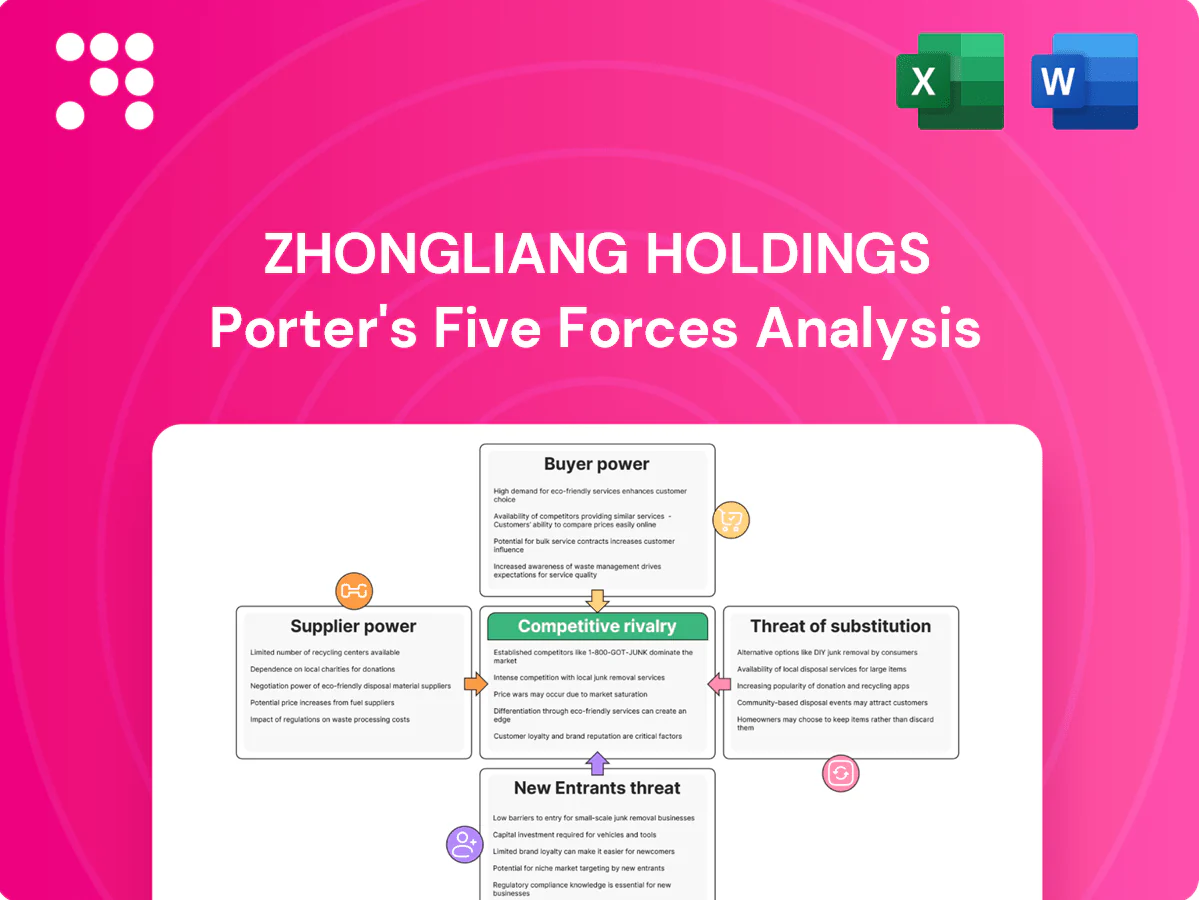

Zhongliang Holdings faces moderate buyer power, high rivalry from established developers, and meaningful regulatory and financing pressures that squeeze margins and strategic flexibility; supplier and substitute threats are currently muted but evolving. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights for investment or strategy decisions.

Suppliers Bargaining Power

Land supply concentrated

Urban land in China is auctioned almost exclusively by local governments, concentrating supply in a few powerful sellers who set timing and price; this near-100% public supply elevates supplier leverage. Policy cycles in 2023–24 tightened quotas and delayed auctions, compressing developer pipelines and raising financing risk. Zhongliang’s focus in the Yangtze River Delta — roughly a quarter of national GDP — increases exposure to fierce bidding and pricier parcels, so supplier power remains high despite occasional policy-driven discounts.

Materials commoditized

Materials such as cement, steel, glass and fittings are largely standardized with many suppliers, enabling Zhongliang to multi-source and extract volume and payment-term discounts. China produced roughly 2.2bn t of cement and 1.05bn t of steel in 2024, supporting broad vendor availability. Still, steel/cement price swings and 2024 environmental curbs tightened supply, compressing margins. West China logistics bottlenecks raise localized supplier leverage.

Contractor capacity cycles

EPC/general contractors’ bargaining power softens in the current sector slowdown, giving developers some rate leverage, though top-tier firms remain scarce for high-quality projects and command premiums. Post-2021 payment defaults have pushed contractors to insist on tighter cash safeguards, often retaining up to 10% on contracts. In core cities reputable contractors still retain pricing power due to delivery assurance.

Financing as a “supplier”

Banks, trusts and bond investors function as capital suppliers to Zhongliang, and after the 2020 three red lines regime lenders increased leverage via higher pricing, tighter covenants and allocation controls; market commentary in 2024 showed financing remained concentrated toward lower-risk SOEs while private developers faced steeper spreads and conditional access. Zhongliang’s funding terms thus hinge on its credit profile, pledged collateral and prevailing policy windows.

- Banks: core senior funding;

- Trusts/bonds: mezzanine and market access;

- Post-three red lines: higher spreads, tighter covenants;

- SOE vs private: clear access gap;

- Zhongliang: credit, collateral, policy-dependent.

Property services partners

Designers, MEP consultants and property managers supply differentiated expertise, with brand-name partners commanding premium fees in upscale segments; Zhongliang’s in-house property management (covering its core residential portfolio) reduces supplier dependence. Specialized green-building and smart-home vendors retain niche leverage as adoption rose in China (market >RMB2.2tn in 2024).

- Designers: differentiated expertise

- Brand partners: premium pricing in luxury

- In-house PM: lowers supplier risk

- Green/smart vendors: niche bargaining power

Land auctions & tighter financing lift bidding costs and squeeze margins, YRD exposure intensifies

Urban land auctions concentrated with local governments and 2023–24 quota cuts kept supplier power high; Yangtze River Delta exposure raises parcel bidding and costs. Commodity materials abundant nationally (2024: cement 2.2bn t, steel 1.05bn t) limiting supplier hold but price swings and curbs squeezed margins. Financing remains a key supplier leverage: post-three red lines banks favor SOEs, raising spreads for private developers like Zhongliang.

| Supplier | 2024 metric | Impact on Zhongliang |

|---|---|---|

| Land (local govts) | Auction-controlled; quota cuts 2023–24 | High bargaining power |

| Cement/Steel | 2.2bn t / 1.05bn t | Low supplier concentration but price volatility |

| Contractors | Retain 10% retention | Moderate power in core cities |

| Finance | Higher spreads vs SOEs (2024) | High leverage over Zhongliang |

What is included in the product

Tailored Porter's Five Forces for Zhongliang Holdings: examines competitive rivalry, buyer/supplier power, entry barriers, and substitute threats to assess pricing leverage, margin risks, and strategic defenses.

A concise, one-sheet Porter's Five Forces for Zhongliang Holdings that maps competitive pressures and buyer/supplier dynamics to relieve strategic uncertainty; customize pressure levels with current market data for instant, slide-ready insights.

Customers Bargaining Power

High price sensitivity

Homebuyers in China remain highly price-aware amid weak income growth and housing deflation, with many cities seeing mid-single-digit price declines into 2024; discounting and promotions by developers quickly shift bookings. Zhongliang faces a trade-off between aggressive discounts to sustain sales and margin erosion that hurts cash collection and debt servicing. Mortgage relief—notably a 5-year LPR near 4.3% in 2024—eases pressure but does not remove entrenched price sensitivity.

Abundant alternatives

Zhongliang Holdings (HKEX: 2772) faces abundant alternatives as competing new builds and large second-hand inventories give buyers many choices. Buyers in 2024 switch readily by location, school district, brand and delivery record, especially in YRD cities such as Shanghai, Suzhou and Hangzhou where dense competition amplifies comparison shopping. This breadth strengthens buyer bargaining power on features and price.

Delivery and trust concerns

With presales funding construction and industry debt near $1.3 trillion in 2024, on-time delivery is paramount to buyers who face project completion risk. Sector distress has made purchasers risk-averse, favoring SOEs or developers with proven track records. Zhongliang must use escrow transparency, clear construction milestones and robust warranties to reassure buyers. Heightened scrutiny empowers purchasers to demand discounts or stronger safeguards.

Regulatory protections

Regulatory protections—stricter escrow of presale proceeds and mandatory completion guarantees—shift cash flows from sales to construction, making compliance a marketable attribute for Zhongliang and other developers.

As guaranteed-delivery rules become enforcement benchmarks, buyers gain indirect bargaining power: projects that meet escrow and guarantee requirements command stronger buyer confidence, while noncompliance forces pricing concessions and dampens demand.

- escrow protections: increase buyer security, raise developer compliance costs

- guaranteed delivery: shifts cash use toward construction, strengthens buyer leverage

- noncompliance risk: reduces demand and drives discounts

Segmented demand

Segmented demand at Zhongliang means first-time buyers, upgraders and investors prioritize price, layout and yield differently; tailored product-mix and amenities are required to win each segment. Missed fit can slow absorption by months and force discounts—2024 market reports saw project-specific discounts exceed 10% in weak launches. Data-driven pricing and layout optimization reduce buyer leverage and speed sell-through.

- First-time buyers: affordability, compact layouts

- Upgraders: space, school/amenity access

- Investors: yield, rental demand

- 2024 risk: >10% discounts in under‑fit projects

Buyers cut prices as mid-single-digit housing declines force developers to trade margin for cash

Buyers in 2024 are highly price-sensitive amid mid-single-digit housing deflation, forcing Zhongliang to balance deep discounts against margin and cash risks. Abundant alternatives and large resales pools raise buyer leverage; on-time delivery and escrow/guarantee compliance materially reduce purchase risk. Data-driven product fit cuts absorption time and limits >10% project‑level discounts.

| Metric | 2024 Value |

|---|---|

| Housing price change | Mid-single-digit decline |

| 5yr LPR | ≈4.3% |

| Industry debt | ≈RMB 1.3T |

| Weak-launch discounts | >10% |

Preview the Actual Deliverable

Zhongliang Holdings Porter's Five Forces Analysis

This Zhongliang Holdings Porter’s Five Forces Analysis evaluates competitive rivalry, threat of new entrants, bargaining power of suppliers and customers, and substitutes, translating findings into strategic implications and risk-adjusted recommendations. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

Don't Miss the Bigger Picture

Zhongliang Holdings faces moderate buyer power, high rivalry from established developers, and meaningful regulatory and financing pressures that squeeze margins and strategic flexibility; supplier and substitute threats are currently muted but evolving. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights for investment or strategy decisions.

Suppliers Bargaining Power

Land supply concentrated

Urban land in China is auctioned almost exclusively by local governments, concentrating supply in a few powerful sellers who set timing and price; this near-100% public supply elevates supplier leverage. Policy cycles in 2023–24 tightened quotas and delayed auctions, compressing developer pipelines and raising financing risk. Zhongliang’s focus in the Yangtze River Delta — roughly a quarter of national GDP — increases exposure to fierce bidding and pricier parcels, so supplier power remains high despite occasional policy-driven discounts.

Materials commoditized

Materials such as cement, steel, glass and fittings are largely standardized with many suppliers, enabling Zhongliang to multi-source and extract volume and payment-term discounts. China produced roughly 2.2bn t of cement and 1.05bn t of steel in 2024, supporting broad vendor availability. Still, steel/cement price swings and 2024 environmental curbs tightened supply, compressing margins. West China logistics bottlenecks raise localized supplier leverage.

Contractor capacity cycles

EPC/general contractors’ bargaining power softens in the current sector slowdown, giving developers some rate leverage, though top-tier firms remain scarce for high-quality projects and command premiums. Post-2021 payment defaults have pushed contractors to insist on tighter cash safeguards, often retaining up to 10% on contracts. In core cities reputable contractors still retain pricing power due to delivery assurance.

Financing as a “supplier”

Banks, trusts and bond investors function as capital suppliers to Zhongliang, and after the 2020 three red lines regime lenders increased leverage via higher pricing, tighter covenants and allocation controls; market commentary in 2024 showed financing remained concentrated toward lower-risk SOEs while private developers faced steeper spreads and conditional access. Zhongliang’s funding terms thus hinge on its credit profile, pledged collateral and prevailing policy windows.

- Banks: core senior funding;

- Trusts/bonds: mezzanine and market access;

- Post-three red lines: higher spreads, tighter covenants;

- SOE vs private: clear access gap;

- Zhongliang: credit, collateral, policy-dependent.

Property services partners

Designers, MEP consultants and property managers supply differentiated expertise, with brand-name partners commanding premium fees in upscale segments; Zhongliang’s in-house property management (covering its core residential portfolio) reduces supplier dependence. Specialized green-building and smart-home vendors retain niche leverage as adoption rose in China (market >RMB2.2tn in 2024).

- Designers: differentiated expertise

- Brand partners: premium pricing in luxury

- In-house PM: lowers supplier risk

- Green/smart vendors: niche bargaining power

Land auctions & tighter financing lift bidding costs and squeeze margins, YRD exposure intensifies

Urban land auctions concentrated with local governments and 2023–24 quota cuts kept supplier power high; Yangtze River Delta exposure raises parcel bidding and costs. Commodity materials abundant nationally (2024: cement 2.2bn t, steel 1.05bn t) limiting supplier hold but price swings and curbs squeezed margins. Financing remains a key supplier leverage: post-three red lines banks favor SOEs, raising spreads for private developers like Zhongliang.

| Supplier | 2024 metric | Impact on Zhongliang |

|---|---|---|

| Land (local govts) | Auction-controlled; quota cuts 2023–24 | High bargaining power |

| Cement/Steel | 2.2bn t / 1.05bn t | Low supplier concentration but price volatility |

| Contractors | Retain 10% retention | Moderate power in core cities |

| Finance | Higher spreads vs SOEs (2024) | High leverage over Zhongliang |

What is included in the product

Tailored Porter's Five Forces for Zhongliang Holdings: examines competitive rivalry, buyer/supplier power, entry barriers, and substitute threats to assess pricing leverage, margin risks, and strategic defenses.

A concise, one-sheet Porter's Five Forces for Zhongliang Holdings that maps competitive pressures and buyer/supplier dynamics to relieve strategic uncertainty; customize pressure levels with current market data for instant, slide-ready insights.

Customers Bargaining Power

High price sensitivity

Homebuyers in China remain highly price-aware amid weak income growth and housing deflation, with many cities seeing mid-single-digit price declines into 2024; discounting and promotions by developers quickly shift bookings. Zhongliang faces a trade-off between aggressive discounts to sustain sales and margin erosion that hurts cash collection and debt servicing. Mortgage relief—notably a 5-year LPR near 4.3% in 2024—eases pressure but does not remove entrenched price sensitivity.

Abundant alternatives

Zhongliang Holdings (HKEX: 2772) faces abundant alternatives as competing new builds and large second-hand inventories give buyers many choices. Buyers in 2024 switch readily by location, school district, brand and delivery record, especially in YRD cities such as Shanghai, Suzhou and Hangzhou where dense competition amplifies comparison shopping. This breadth strengthens buyer bargaining power on features and price.

Delivery and trust concerns

With presales funding construction and industry debt near $1.3 trillion in 2024, on-time delivery is paramount to buyers who face project completion risk. Sector distress has made purchasers risk-averse, favoring SOEs or developers with proven track records. Zhongliang must use escrow transparency, clear construction milestones and robust warranties to reassure buyers. Heightened scrutiny empowers purchasers to demand discounts or stronger safeguards.

Regulatory protections

Regulatory protections—stricter escrow of presale proceeds and mandatory completion guarantees—shift cash flows from sales to construction, making compliance a marketable attribute for Zhongliang and other developers.

As guaranteed-delivery rules become enforcement benchmarks, buyers gain indirect bargaining power: projects that meet escrow and guarantee requirements command stronger buyer confidence, while noncompliance forces pricing concessions and dampens demand.

- escrow protections: increase buyer security, raise developer compliance costs

- guaranteed delivery: shifts cash use toward construction, strengthens buyer leverage

- noncompliance risk: reduces demand and drives discounts

Segmented demand

Segmented demand at Zhongliang means first-time buyers, upgraders and investors prioritize price, layout and yield differently; tailored product-mix and amenities are required to win each segment. Missed fit can slow absorption by months and force discounts—2024 market reports saw project-specific discounts exceed 10% in weak launches. Data-driven pricing and layout optimization reduce buyer leverage and speed sell-through.

- First-time buyers: affordability, compact layouts

- Upgraders: space, school/amenity access

- Investors: yield, rental demand

- 2024 risk: >10% discounts in under‑fit projects

Buyers cut prices as mid-single-digit housing declines force developers to trade margin for cash

Buyers in 2024 are highly price-sensitive amid mid-single-digit housing deflation, forcing Zhongliang to balance deep discounts against margin and cash risks. Abundant alternatives and large resales pools raise buyer leverage; on-time delivery and escrow/guarantee compliance materially reduce purchase risk. Data-driven product fit cuts absorption time and limits >10% project‑level discounts.

| Metric | 2024 Value |

|---|---|

| Housing price change | Mid-single-digit decline |

| 5yr LPR | ≈4.3% |

| Industry debt | ≈RMB 1.3T |

| Weak-launch discounts | >10% |

Preview the Actual Deliverable

Zhongliang Holdings Porter's Five Forces Analysis

This Zhongliang Holdings Porter’s Five Forces Analysis evaluates competitive rivalry, threat of new entrants, bargaining power of suppliers and customers, and substitutes, translating findings into strategic implications and risk-adjusted recommendations. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

Description

Don't Miss the Bigger Picture

Zhongliang Holdings faces moderate buyer power, high rivalry from established developers, and meaningful regulatory and financing pressures that squeeze margins and strategic flexibility; supplier and substitute threats are currently muted but evolving. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights for investment or strategy decisions.

Suppliers Bargaining Power

Land supply concentrated

Urban land in China is auctioned almost exclusively by local governments, concentrating supply in a few powerful sellers who set timing and price; this near-100% public supply elevates supplier leverage. Policy cycles in 2023–24 tightened quotas and delayed auctions, compressing developer pipelines and raising financing risk. Zhongliang’s focus in the Yangtze River Delta — roughly a quarter of national GDP — increases exposure to fierce bidding and pricier parcels, so supplier power remains high despite occasional policy-driven discounts.

Materials commoditized

Materials such as cement, steel, glass and fittings are largely standardized with many suppliers, enabling Zhongliang to multi-source and extract volume and payment-term discounts. China produced roughly 2.2bn t of cement and 1.05bn t of steel in 2024, supporting broad vendor availability. Still, steel/cement price swings and 2024 environmental curbs tightened supply, compressing margins. West China logistics bottlenecks raise localized supplier leverage.

Contractor capacity cycles

EPC/general contractors’ bargaining power softens in the current sector slowdown, giving developers some rate leverage, though top-tier firms remain scarce for high-quality projects and command premiums. Post-2021 payment defaults have pushed contractors to insist on tighter cash safeguards, often retaining up to 10% on contracts. In core cities reputable contractors still retain pricing power due to delivery assurance.

Financing as a “supplier”

Banks, trusts and bond investors function as capital suppliers to Zhongliang, and after the 2020 three red lines regime lenders increased leverage via higher pricing, tighter covenants and allocation controls; market commentary in 2024 showed financing remained concentrated toward lower-risk SOEs while private developers faced steeper spreads and conditional access. Zhongliang’s funding terms thus hinge on its credit profile, pledged collateral and prevailing policy windows.

- Banks: core senior funding;

- Trusts/bonds: mezzanine and market access;

- Post-three red lines: higher spreads, tighter covenants;

- SOE vs private: clear access gap;

- Zhongliang: credit, collateral, policy-dependent.

Property services partners

Designers, MEP consultants and property managers supply differentiated expertise, with brand-name partners commanding premium fees in upscale segments; Zhongliang’s in-house property management (covering its core residential portfolio) reduces supplier dependence. Specialized green-building and smart-home vendors retain niche leverage as adoption rose in China (market >RMB2.2tn in 2024).

- Designers: differentiated expertise

- Brand partners: premium pricing in luxury

- In-house PM: lowers supplier risk

- Green/smart vendors: niche bargaining power

Land auctions & tighter financing lift bidding costs and squeeze margins, YRD exposure intensifies

Urban land auctions concentrated with local governments and 2023–24 quota cuts kept supplier power high; Yangtze River Delta exposure raises parcel bidding and costs. Commodity materials abundant nationally (2024: cement 2.2bn t, steel 1.05bn t) limiting supplier hold but price swings and curbs squeezed margins. Financing remains a key supplier leverage: post-three red lines banks favor SOEs, raising spreads for private developers like Zhongliang.

| Supplier | 2024 metric | Impact on Zhongliang |

|---|---|---|

| Land (local govts) | Auction-controlled; quota cuts 2023–24 | High bargaining power |

| Cement/Steel | 2.2bn t / 1.05bn t | Low supplier concentration but price volatility |

| Contractors | Retain 10% retention | Moderate power in core cities |

| Finance | Higher spreads vs SOEs (2024) | High leverage over Zhongliang |

What is included in the product

Tailored Porter's Five Forces for Zhongliang Holdings: examines competitive rivalry, buyer/supplier power, entry barriers, and substitute threats to assess pricing leverage, margin risks, and strategic defenses.

A concise, one-sheet Porter's Five Forces for Zhongliang Holdings that maps competitive pressures and buyer/supplier dynamics to relieve strategic uncertainty; customize pressure levels with current market data for instant, slide-ready insights.

Customers Bargaining Power

High price sensitivity

Homebuyers in China remain highly price-aware amid weak income growth and housing deflation, with many cities seeing mid-single-digit price declines into 2024; discounting and promotions by developers quickly shift bookings. Zhongliang faces a trade-off between aggressive discounts to sustain sales and margin erosion that hurts cash collection and debt servicing. Mortgage relief—notably a 5-year LPR near 4.3% in 2024—eases pressure but does not remove entrenched price sensitivity.

Abundant alternatives

Zhongliang Holdings (HKEX: 2772) faces abundant alternatives as competing new builds and large second-hand inventories give buyers many choices. Buyers in 2024 switch readily by location, school district, brand and delivery record, especially in YRD cities such as Shanghai, Suzhou and Hangzhou where dense competition amplifies comparison shopping. This breadth strengthens buyer bargaining power on features and price.

Delivery and trust concerns

With presales funding construction and industry debt near $1.3 trillion in 2024, on-time delivery is paramount to buyers who face project completion risk. Sector distress has made purchasers risk-averse, favoring SOEs or developers with proven track records. Zhongliang must use escrow transparency, clear construction milestones and robust warranties to reassure buyers. Heightened scrutiny empowers purchasers to demand discounts or stronger safeguards.

Regulatory protections

Regulatory protections—stricter escrow of presale proceeds and mandatory completion guarantees—shift cash flows from sales to construction, making compliance a marketable attribute for Zhongliang and other developers.

As guaranteed-delivery rules become enforcement benchmarks, buyers gain indirect bargaining power: projects that meet escrow and guarantee requirements command stronger buyer confidence, while noncompliance forces pricing concessions and dampens demand.

- escrow protections: increase buyer security, raise developer compliance costs

- guaranteed delivery: shifts cash use toward construction, strengthens buyer leverage

- noncompliance risk: reduces demand and drives discounts

Segmented demand

Segmented demand at Zhongliang means first-time buyers, upgraders and investors prioritize price, layout and yield differently; tailored product-mix and amenities are required to win each segment. Missed fit can slow absorption by months and force discounts—2024 market reports saw project-specific discounts exceed 10% in weak launches. Data-driven pricing and layout optimization reduce buyer leverage and speed sell-through.

- First-time buyers: affordability, compact layouts

- Upgraders: space, school/amenity access

- Investors: yield, rental demand

- 2024 risk: >10% discounts in under‑fit projects

Buyers cut prices as mid-single-digit housing declines force developers to trade margin for cash

Buyers in 2024 are highly price-sensitive amid mid-single-digit housing deflation, forcing Zhongliang to balance deep discounts against margin and cash risks. Abundant alternatives and large resales pools raise buyer leverage; on-time delivery and escrow/guarantee compliance materially reduce purchase risk. Data-driven product fit cuts absorption time and limits >10% project‑level discounts.

| Metric | 2024 Value |

|---|---|

| Housing price change | Mid-single-digit decline |

| 5yr LPR | ≈4.3% |

| Industry debt | ≈RMB 1.3T |

| Weak-launch discounts | >10% |

Preview the Actual Deliverable

Zhongliang Holdings Porter's Five Forces Analysis

This Zhongliang Holdings Porter’s Five Forces Analysis evaluates competitive rivalry, threat of new entrants, bargaining power of suppliers and customers, and substitutes, translating findings into strategic implications and risk-adjusted recommendations. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.