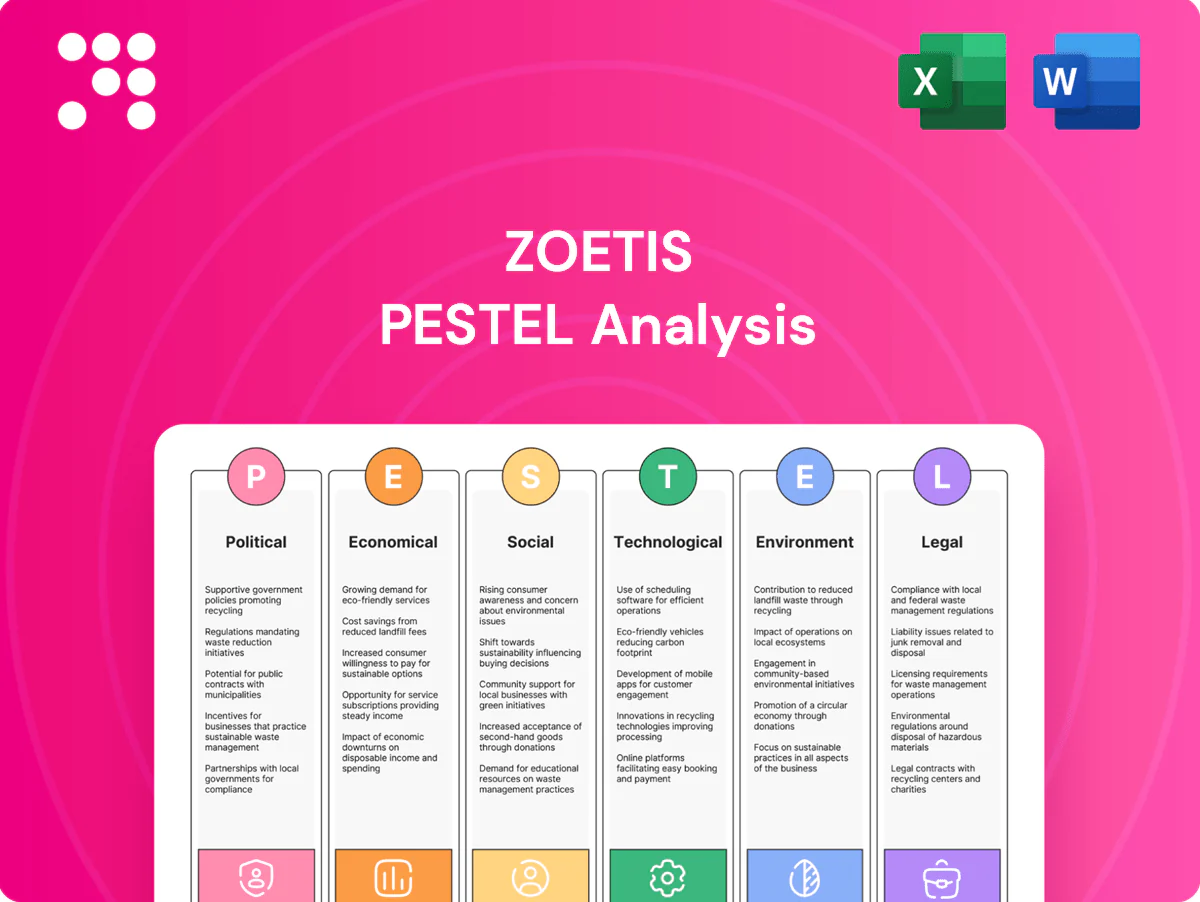

Zoetis PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock how political shifts, economic cycles, and technological advances are reshaping Zoetis’s growth prospects with our concise PESTLE snapshot—ideal for investors and strategists. This expert analysis highlights regulatory risks, market opportunities, and sustainability trends that matter now. Purchase the full PESTLE report to get the complete, actionable breakdown and ready-to-use slides and data.

Political factors

Regulatory stability & trade policy

Animal health products face shifting policies across the US, EU, China and emerging markets, affecting Zoetis which sells in more than 100 countries and competes in a global animal health market estimated at about $55 billion in 2024. Tariffs, sanctions and veterinary import rules can accelerate or delay market access and add to time-to-revenue. Political alignment on food security has unlocked subsidies in regions such as the EU and parts of Asia, boosting livestock health spending. Geopolitical instability raises supply risk and compliance costs for Zoetis.

Public health & biosecurity priorities

Governments fund surveillance and emergency stockpiles for zoonotic threats as 60% of human infectious diseases are zoonotic and 75% of emerging pathogens originate in animals, driving sustained public spending on preparedness. Priority disease lists and national vaccination programs raise demand for targeted veterinary vaccines and diagnostics, while FDA Emergency Use Authorizations and EMA conditional approvals can fast-track procurement after outbreaks. Reduced attention post-crisis often compresses volumes and pressures pricing, creating revenue volatility for firms like Zoetis.

Agricultural subsidies & rural policy

Agricultural subsidies shape herd sizes, productivity targets and access to veterinary services, influencing demand for Zoetis products; Zoetis reported roughly $8.9B revenue in 2024 so shifts in farm support can materially reweight species and regional sales. Incentives for herd health programs foster preventive adoption over treatment, expanding markets for vaccines and diagnostics. Rural veterinary workforce policies and shortages constrain product utilization and uptake rates in key livestock markets.

Geopolitical supply chain resiliency

Export controls on biologics, adjuvants and critical inputs can disrupt Zoetis production; governments increasingly mandate local manufacturing or stockpiling, and Zoetis sells in more than 100 countries. Political risk forces multi-region sourcing and larger inventory buffers, raising COGS, lengthening lead times and squeezing service levels.

- Export controls disrupt supply

- Local manufacturing/stockpiles rising

- Multi-region sourcing increases costs

- Higher inventory → longer lead times, lower margins

Government procurement & price negotiations

Government tenders for livestock vaccines and companion-animal programs constrain Zoetis pricing power while increasing order visibility. Centralized buying frequently compresses margins but improves volume predictability. Health-agency partnerships shape clinical priorities and data requirements, and policy-driven purchasing cycles add seasonality to demand.

- Zoetis FY2024 revenue reported at $8.66 billion

- Operates in 100+ countries

- Public tenders boost predictability; centralized buying can compress margins

Tariffs, mandates and tenders reshape animal-health market; vaccines buoyed by zoonotic risk

Political shifts in US, EU, China and emerging markets affect Zoetis (FY2024 revenue $8.66B; 100+ countries) via tariffs, export controls, local-manufacturing mandates and centralized tenders that compress margins while boosting volume predictability. Government zoonotic preparedness (60% human infections zoonotic; 75% emerging pathogens animal-origin) sustains vaccine and diagnostic demand.

| Metric | Value |

|---|---|

| Zoetis FY2024 | $8.66B |

| Global market (2024) | $55B |

| Countries | 100+ |

What is included in the product

Explores how macro-environmental forces uniquely affect Zoetis across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and regional regulatory context; designed to help executives, investors and strategists identify threats, opportunities and forward-looking scenarios for decision-making.

A concise, visually segmented PESTLE summary of Zoetis that clarifies regulatory, market and technological risks for quick meeting use, editable for region-specific notes and easily dropped into slides or reports.

Economic factors

Livestock cycles & commodity prices

Producer profitability depends on feed, milk, meat and egg prices; volatile corn and soybean markets pushed feed costs up 18% in 2023–24, squeezing margins and driving cautious herd expansion. Strong margins in 2021–22 enabled investment in vaccines, parasiticides and diagnostics, while downturns prompt trade-down and fewer herd treatments. Zoetis reported ~9.3 billion in 2024 sales with ~36% livestock exposure, requiring agile pricing and bundled offerings by region and species.

Pet humanization & premiumization

Rising pet ownership—about 70% of US households per APPA—sustains resilient demand for preventive care, underpinning steady volume for vaccines and parasiticides. Willingness to pay for chronic therapies and in-clinic diagnostics supports premium pricing and higher ASPs. Macroeconomic slowdowns can push price-sensitive owners toward generics while veterinary services and procedures remain sticky; growing pet insurance (around 3–4% penetration in the US with double-digit annual policy growth) further stabilizes companion-animal health spend.

Inflation, FX, and input costs

Biologics inputs, energy and logistics inflation pressured Zoetis margins in 2024; Brent averaged roughly $85–90/barrel that year, raising production and distribution costs. Currency swings—USD strength versus major currencies in 2024—compressed reported revenue and local affordability in markets like Latin America and Europe. Zoetis used pricing actions, productivity programs, hedging and a regional manufacturing footprint to offset cost creep and FX volatility.

Veterinary capacity & clinic economics

Emerging market growth

Urbanization is accelerating—UN projects urban share rising from about 56% in 2020 to 68% by 2050—driving protein demand and lifting livestock‑health investment in emerging markets; low baseline penetration leaves significant runway for vaccines and diagnostics, though credit access and cold‑chain infrastructure remain bottlenecks, so tailored pricing and local partnerships are critical to scale.

- Urbanization: UN 56% (2020) → 68% (2050)

- Opportunity: low veterinary penetration = growth runway

- Constraints: limited credit, cold‑chain gaps

- Strategy: tailored pricing + local partnerships

Tariffs, mandates and tenders reshape animal-health market; vaccines buoyed by zoonotic risk

Producer margins squeezed by 18% feed cost rise (2023–24) and volatile corn/soy markets; Zoetis reported ~9.3B sales in 2024 with ~36% livestock exposure, requiring agile pricing. Pet demand resilient (US pet ownership ~70%); pet insurance penetration ~3–4% stabilizes spend but slowdowns favor generics. Input, energy and FX pressure (Brent ~$85–90/bbl, USD strength) led to pricing, productivity and hedging actions; clinic staffing gaps ~60% and DSO share ~20% affect pull‑through.

| Metric | 2024 |

|---|---|

| Zoetis sales | ~$9.3B |

| Livestock exposure | 36% |

| Feed cost rise | +18% |

| Clinic staffing gaps | ~60% |

| DSO share | ~20% |

| Brent | $85–90/bbl |

What You See Is What You Get

Zoetis PESTLE Analysis

The Zoetis PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment as presented. No placeholders or teasers—this is the final, downloadable file.

Plan Smarter. Present Sharper. Compete Stronger.

Unlock how political shifts, economic cycles, and technological advances are reshaping Zoetis’s growth prospects with our concise PESTLE snapshot—ideal for investors and strategists. This expert analysis highlights regulatory risks, market opportunities, and sustainability trends that matter now. Purchase the full PESTLE report to get the complete, actionable breakdown and ready-to-use slides and data.

Political factors

Regulatory stability & trade policy

Animal health products face shifting policies across the US, EU, China and emerging markets, affecting Zoetis which sells in more than 100 countries and competes in a global animal health market estimated at about $55 billion in 2024. Tariffs, sanctions and veterinary import rules can accelerate or delay market access and add to time-to-revenue. Political alignment on food security has unlocked subsidies in regions such as the EU and parts of Asia, boosting livestock health spending. Geopolitical instability raises supply risk and compliance costs for Zoetis.

Public health & biosecurity priorities

Governments fund surveillance and emergency stockpiles for zoonotic threats as 60% of human infectious diseases are zoonotic and 75% of emerging pathogens originate in animals, driving sustained public spending on preparedness. Priority disease lists and national vaccination programs raise demand for targeted veterinary vaccines and diagnostics, while FDA Emergency Use Authorizations and EMA conditional approvals can fast-track procurement after outbreaks. Reduced attention post-crisis often compresses volumes and pressures pricing, creating revenue volatility for firms like Zoetis.

Agricultural subsidies & rural policy

Agricultural subsidies shape herd sizes, productivity targets and access to veterinary services, influencing demand for Zoetis products; Zoetis reported roughly $8.9B revenue in 2024 so shifts in farm support can materially reweight species and regional sales. Incentives for herd health programs foster preventive adoption over treatment, expanding markets for vaccines and diagnostics. Rural veterinary workforce policies and shortages constrain product utilization and uptake rates in key livestock markets.

Geopolitical supply chain resiliency

Export controls on biologics, adjuvants and critical inputs can disrupt Zoetis production; governments increasingly mandate local manufacturing or stockpiling, and Zoetis sells in more than 100 countries. Political risk forces multi-region sourcing and larger inventory buffers, raising COGS, lengthening lead times and squeezing service levels.

- Export controls disrupt supply

- Local manufacturing/stockpiles rising

- Multi-region sourcing increases costs

- Higher inventory → longer lead times, lower margins

Government procurement & price negotiations

Government tenders for livestock vaccines and companion-animal programs constrain Zoetis pricing power while increasing order visibility. Centralized buying frequently compresses margins but improves volume predictability. Health-agency partnerships shape clinical priorities and data requirements, and policy-driven purchasing cycles add seasonality to demand.

- Zoetis FY2024 revenue reported at $8.66 billion

- Operates in 100+ countries

- Public tenders boost predictability; centralized buying can compress margins

Tariffs, mandates and tenders reshape animal-health market; vaccines buoyed by zoonotic risk

Political shifts in US, EU, China and emerging markets affect Zoetis (FY2024 revenue $8.66B; 100+ countries) via tariffs, export controls, local-manufacturing mandates and centralized tenders that compress margins while boosting volume predictability. Government zoonotic preparedness (60% human infections zoonotic; 75% emerging pathogens animal-origin) sustains vaccine and diagnostic demand.

| Metric | Value |

|---|---|

| Zoetis FY2024 | $8.66B |

| Global market (2024) | $55B |

| Countries | 100+ |

What is included in the product

Explores how macro-environmental forces uniquely affect Zoetis across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and regional regulatory context; designed to help executives, investors and strategists identify threats, opportunities and forward-looking scenarios for decision-making.

A concise, visually segmented PESTLE summary of Zoetis that clarifies regulatory, market and technological risks for quick meeting use, editable for region-specific notes and easily dropped into slides or reports.

Economic factors

Livestock cycles & commodity prices

Producer profitability depends on feed, milk, meat and egg prices; volatile corn and soybean markets pushed feed costs up 18% in 2023–24, squeezing margins and driving cautious herd expansion. Strong margins in 2021–22 enabled investment in vaccines, parasiticides and diagnostics, while downturns prompt trade-down and fewer herd treatments. Zoetis reported ~9.3 billion in 2024 sales with ~36% livestock exposure, requiring agile pricing and bundled offerings by region and species.

Pet humanization & premiumization

Rising pet ownership—about 70% of US households per APPA—sustains resilient demand for preventive care, underpinning steady volume for vaccines and parasiticides. Willingness to pay for chronic therapies and in-clinic diagnostics supports premium pricing and higher ASPs. Macroeconomic slowdowns can push price-sensitive owners toward generics while veterinary services and procedures remain sticky; growing pet insurance (around 3–4% penetration in the US with double-digit annual policy growth) further stabilizes companion-animal health spend.

Inflation, FX, and input costs

Biologics inputs, energy and logistics inflation pressured Zoetis margins in 2024; Brent averaged roughly $85–90/barrel that year, raising production and distribution costs. Currency swings—USD strength versus major currencies in 2024—compressed reported revenue and local affordability in markets like Latin America and Europe. Zoetis used pricing actions, productivity programs, hedging and a regional manufacturing footprint to offset cost creep and FX volatility.

Veterinary capacity & clinic economics

Emerging market growth

Urbanization is accelerating—UN projects urban share rising from about 56% in 2020 to 68% by 2050—driving protein demand and lifting livestock‑health investment in emerging markets; low baseline penetration leaves significant runway for vaccines and diagnostics, though credit access and cold‑chain infrastructure remain bottlenecks, so tailored pricing and local partnerships are critical to scale.

- Urbanization: UN 56% (2020) → 68% (2050)

- Opportunity: low veterinary penetration = growth runway

- Constraints: limited credit, cold‑chain gaps

- Strategy: tailored pricing + local partnerships

Tariffs, mandates and tenders reshape animal-health market; vaccines buoyed by zoonotic risk

Producer margins squeezed by 18% feed cost rise (2023–24) and volatile corn/soy markets; Zoetis reported ~9.3B sales in 2024 with ~36% livestock exposure, requiring agile pricing. Pet demand resilient (US pet ownership ~70%); pet insurance penetration ~3–4% stabilizes spend but slowdowns favor generics. Input, energy and FX pressure (Brent ~$85–90/bbl, USD strength) led to pricing, productivity and hedging actions; clinic staffing gaps ~60% and DSO share ~20% affect pull‑through.

| Metric | 2024 |

|---|---|

| Zoetis sales | ~$9.3B |

| Livestock exposure | 36% |

| Feed cost rise | +18% |

| Clinic staffing gaps | ~60% |

| DSO share | ~20% |

| Brent | $85–90/bbl |

What You See Is What You Get

Zoetis PESTLE Analysis

The Zoetis PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment as presented. No placeholders or teasers—this is the final, downloadable file.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock how political shifts, economic cycles, and technological advances are reshaping Zoetis’s growth prospects with our concise PESTLE snapshot—ideal for investors and strategists. This expert analysis highlights regulatory risks, market opportunities, and sustainability trends that matter now. Purchase the full PESTLE report to get the complete, actionable breakdown and ready-to-use slides and data.

Political factors

Regulatory stability & trade policy

Animal health products face shifting policies across the US, EU, China and emerging markets, affecting Zoetis which sells in more than 100 countries and competes in a global animal health market estimated at about $55 billion in 2024. Tariffs, sanctions and veterinary import rules can accelerate or delay market access and add to time-to-revenue. Political alignment on food security has unlocked subsidies in regions such as the EU and parts of Asia, boosting livestock health spending. Geopolitical instability raises supply risk and compliance costs for Zoetis.

Public health & biosecurity priorities

Governments fund surveillance and emergency stockpiles for zoonotic threats as 60% of human infectious diseases are zoonotic and 75% of emerging pathogens originate in animals, driving sustained public spending on preparedness. Priority disease lists and national vaccination programs raise demand for targeted veterinary vaccines and diagnostics, while FDA Emergency Use Authorizations and EMA conditional approvals can fast-track procurement after outbreaks. Reduced attention post-crisis often compresses volumes and pressures pricing, creating revenue volatility for firms like Zoetis.

Agricultural subsidies & rural policy

Agricultural subsidies shape herd sizes, productivity targets and access to veterinary services, influencing demand for Zoetis products; Zoetis reported roughly $8.9B revenue in 2024 so shifts in farm support can materially reweight species and regional sales. Incentives for herd health programs foster preventive adoption over treatment, expanding markets for vaccines and diagnostics. Rural veterinary workforce policies and shortages constrain product utilization and uptake rates in key livestock markets.

Geopolitical supply chain resiliency

Export controls on biologics, adjuvants and critical inputs can disrupt Zoetis production; governments increasingly mandate local manufacturing or stockpiling, and Zoetis sells in more than 100 countries. Political risk forces multi-region sourcing and larger inventory buffers, raising COGS, lengthening lead times and squeezing service levels.

- Export controls disrupt supply

- Local manufacturing/stockpiles rising

- Multi-region sourcing increases costs

- Higher inventory → longer lead times, lower margins

Government procurement & price negotiations

Government tenders for livestock vaccines and companion-animal programs constrain Zoetis pricing power while increasing order visibility. Centralized buying frequently compresses margins but improves volume predictability. Health-agency partnerships shape clinical priorities and data requirements, and policy-driven purchasing cycles add seasonality to demand.

- Zoetis FY2024 revenue reported at $8.66 billion

- Operates in 100+ countries

- Public tenders boost predictability; centralized buying can compress margins

Tariffs, mandates and tenders reshape animal-health market; vaccines buoyed by zoonotic risk

Political shifts in US, EU, China and emerging markets affect Zoetis (FY2024 revenue $8.66B; 100+ countries) via tariffs, export controls, local-manufacturing mandates and centralized tenders that compress margins while boosting volume predictability. Government zoonotic preparedness (60% human infections zoonotic; 75% emerging pathogens animal-origin) sustains vaccine and diagnostic demand.

| Metric | Value |

|---|---|

| Zoetis FY2024 | $8.66B |

| Global market (2024) | $55B |

| Countries | 100+ |

What is included in the product

Explores how macro-environmental forces uniquely affect Zoetis across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and regional regulatory context; designed to help executives, investors and strategists identify threats, opportunities and forward-looking scenarios for decision-making.

A concise, visually segmented PESTLE summary of Zoetis that clarifies regulatory, market and technological risks for quick meeting use, editable for region-specific notes and easily dropped into slides or reports.

Economic factors

Livestock cycles & commodity prices

Producer profitability depends on feed, milk, meat and egg prices; volatile corn and soybean markets pushed feed costs up 18% in 2023–24, squeezing margins and driving cautious herd expansion. Strong margins in 2021–22 enabled investment in vaccines, parasiticides and diagnostics, while downturns prompt trade-down and fewer herd treatments. Zoetis reported ~9.3 billion in 2024 sales with ~36% livestock exposure, requiring agile pricing and bundled offerings by region and species.

Pet humanization & premiumization

Rising pet ownership—about 70% of US households per APPA—sustains resilient demand for preventive care, underpinning steady volume for vaccines and parasiticides. Willingness to pay for chronic therapies and in-clinic diagnostics supports premium pricing and higher ASPs. Macroeconomic slowdowns can push price-sensitive owners toward generics while veterinary services and procedures remain sticky; growing pet insurance (around 3–4% penetration in the US with double-digit annual policy growth) further stabilizes companion-animal health spend.

Inflation, FX, and input costs

Biologics inputs, energy and logistics inflation pressured Zoetis margins in 2024; Brent averaged roughly $85–90/barrel that year, raising production and distribution costs. Currency swings—USD strength versus major currencies in 2024—compressed reported revenue and local affordability in markets like Latin America and Europe. Zoetis used pricing actions, productivity programs, hedging and a regional manufacturing footprint to offset cost creep and FX volatility.

Veterinary capacity & clinic economics

Emerging market growth

Urbanization is accelerating—UN projects urban share rising from about 56% in 2020 to 68% by 2050—driving protein demand and lifting livestock‑health investment in emerging markets; low baseline penetration leaves significant runway for vaccines and diagnostics, though credit access and cold‑chain infrastructure remain bottlenecks, so tailored pricing and local partnerships are critical to scale.

- Urbanization: UN 56% (2020) → 68% (2050)

- Opportunity: low veterinary penetration = growth runway

- Constraints: limited credit, cold‑chain gaps

- Strategy: tailored pricing + local partnerships

Tariffs, mandates and tenders reshape animal-health market; vaccines buoyed by zoonotic risk

Producer margins squeezed by 18% feed cost rise (2023–24) and volatile corn/soy markets; Zoetis reported ~9.3B sales in 2024 with ~36% livestock exposure, requiring agile pricing. Pet demand resilient (US pet ownership ~70%); pet insurance penetration ~3–4% stabilizes spend but slowdowns favor generics. Input, energy and FX pressure (Brent ~$85–90/bbl, USD strength) led to pricing, productivity and hedging actions; clinic staffing gaps ~60% and DSO share ~20% affect pull‑through.

| Metric | 2024 |

|---|---|

| Zoetis sales | ~$9.3B |

| Livestock exposure | 36% |

| Feed cost rise | +18% |

| Clinic staffing gaps | ~60% |

| DSO share | ~20% |

| Brent | $85–90/bbl |

What You See Is What You Get

Zoetis PESTLE Analysis

The Zoetis PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment as presented. No placeholders or teasers—this is the final, downloadable file.