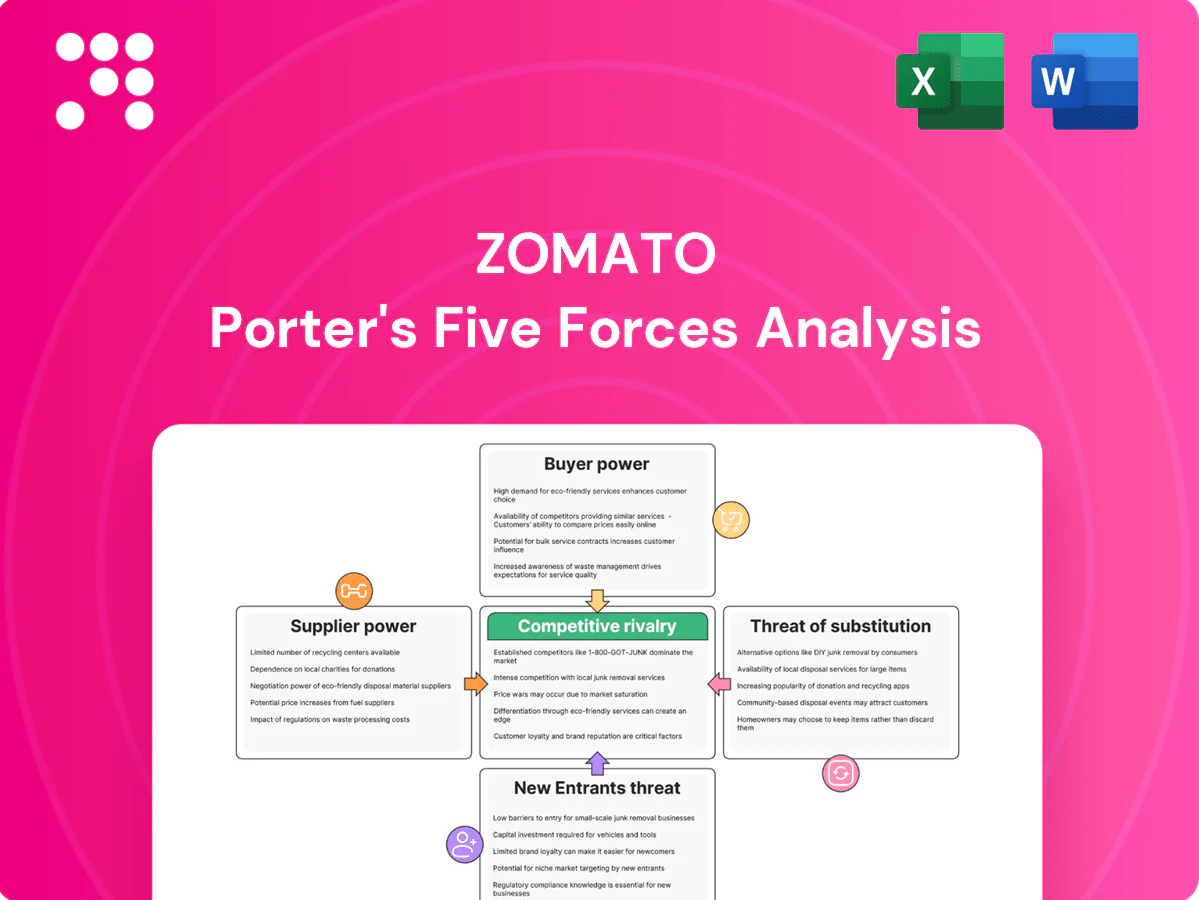

Zomato Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Zomato faces intense rivalry from local and global food delivery players, while buyer power and substitute threats rise with convenience apps and cloud kitchens. Supplier influence is moderate, but regulatory and margin pressures squeeze profitability. This snapshot highlights key competitive tensions. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Fragmented restaurant base

Zomato sources from a vast, fragmented base of over 400,000 restaurant partners, diluting any single supplier’s leverage. Many small and medium eateries rely on the platform for discovery and incremental orders, which enables Zomato to enforce standardized commission structures averaging around 20%. Local clusters of popular outlets, however, can still negotiate preferential terms in high-density urban pockets.

Power of marquee brands

In 2024 iconic chains and high-demand cloud kitchens exert elevated bargaining power on Zomato because strong customer pull concentrates order volume among few marquee partners. They secure lower commissions, premium placement, and richer data access, and losing them increases churn and weakens assortment. Zomato routinely counters with co-marketing spends and tailored SLAs to retain these suppliers.

Delivery partner dynamics

Delivery riders are the core supplier of capacity and service quality for Zomato; industry estimates in 2024 put India’s food-delivery gig workforce at roughly 2 million, so labor tightness or regulatory shifts (minimum pay, benefits) can materially raise payout costs and constrain flexibility. Small incentive tweaks have been shown to shift rider availability during peaks, and rider satisfaction and safety directly drive fulfillment reliability and on-time delivery rates.

Input cost pass-through

Rising food and fuel costs are squeezing restaurant margins, driving partners to push back on Zomato commissions and fees while seeking menu markups or reduced discounts, which can make platform prices appear higher to consumers; Zomato must balance take-rates with partner sustainability.

- Proactive analytics to identify margin pressure

- Cost-sharing programs with restaurants

- Flexible take-rates during inflationary periods

Tech and ecosystem vendors

Tech and ecosystem vendors — payment gateways, map/route APIs and ad-tech partners — create clear dependency points for Zomato; while substitutable, switching causes integration costs and operational risk, and as of 2024 outages or fee hikes have compressed margins across the food‑delivery sector. Zomato’s move to diversify partners and build in‑house payment/routing capabilities aims to reduce this exposure and lower supplier bargaining power over time. This shift improves unit‑economics resilience.

- Dependency: payment gateways, map/route APIs, ad‑tech partners

- Risk: switching costs, integration time, outage-driven margin compression (2024 industry impact)

- Mitigation: partner diversification and growing in‑house capabilities

Huge partner base keeps commissions near 20%; chains, riders and tech squeeze margins

Zomato’s supplier power is diluted by 400,000+ restaurant partners, enabling ~20% average commission discipline, but marquee chains and cloud kitchens concentrate volume and extract preferential terms. Delivery riders (~2 million in India, 2024) and rising food/fuel costs pose material wage and payout risk. Tech vendors create switching costs, prompting build‑inhouse moves to protect margins.

| Supplier | Metric | 2024 |

|---|---|---|

| Restaurants | Partner count / avg take-rate | 400,000+ / ~20% |

| Riders | Workforce | ~2,000,000 |

| Tech vendors | Impact | Integration/switching costs |

What is included in the product

Comprehensive Porter's Five Forces analysis of Zomato that evaluates competitive rivalry, buyer and supplier power, threat of new entrants, and substitutes, highlighting key drivers of pricing, profitability, and market structure. Identifies disruptive threats, regulatory and scale barriers, and strategic levers Zomato can use to defend and grow market share.

A concise one-sheet Porter's Five Forces for Zomato that visualizes competitive pressure with an editable radar chart, lets you customize force levels for scenario analysis (pre/post regulation, new entrants) and drops straight into pitch decks—no macros or advanced finance skills required.

Customers Bargaining Power

Low switching costs

Low switching costs mean consumers move between Zomato, Swiggy or direct ordering with minimal friction; 2024 estimates show Swiggy ~56% and Zomato ~36% market share in India, forcing competitive pricing and reliable delivery; app uninstalls/data portability are negligible for dining choice, so loyalty hinges on convenience, breadth of options and trust.

High price sensitivity

High price sensitivity: frequent deal-seeking elevates coupon and surge sensitivity; Zomato’s ~90 million monthly users in 2024 respond strongly to promotions, pushing heavy discounting. Subscriptions (Pro) moderate elasticity but require ongoing discounts and exclusive value to retain members. Visible fees and delivery charges amplify perceived cost, and even 5–10% price gaps can divert orders to rivals.

Information transparency

Ratings, reviews and visible ETAs give Zomato's over 100 million monthly users (2024) the power to demand quality, turning poor fulfillment or inflated menus into rapid churn within hours. Real-time comparison across listings raises relentless pressure on delivery times and service levels, while Zomato must curate credible content and counter review fraud to protect conversion and retention metrics.

Loyalty and habit formation

Zomato’s memberships, wallet credits, and saved preferences reduce churn by creating switching costs, while rival apps’ matched perks in 2024 keep net switching friction low; habit strengthens when ETAs stay within promised windows and quality is consistent, but service breaks quickly erode loyalty and spike cancellations.

- Memberships: retention lever

- Wallet credits: short-term stickiness

- Reliable ETA: habit driver

- Service breaks: rapid churn trigger

Multi-homing behavior

Many users keep multiple delivery apps — 2024 industry surveys indicate about 70% of urban food-delivery customers multi-home, boosting buyer leverage and switching frequency. Cross-app deal hunting compresses contribution margins as platforms run promotions to retain share. Exclusive offerings and a superior UX can reduce churn. Unique restaurant partnerships further anchor demand and raise switching costs.

- multi-homing ~70% (2024)

- promotion-driven margin pressure

- exclusive UX reduces churn

- unique partnerships anchor demand

High multi-homing (~70%) and 100M MAU fuel fierce price wars and rapid churn

Low switching costs and multi-homing (~70% urban, 2024) give customers high leverage; Swiggy ~56% vs Zomato ~36% market share and Zomato ~100M monthly users force aggressive pricing and promotions. Subscriptions and wallets add temporary stickiness but visible fees, ratings and ETAs drive rapid churn when service slips.

| Metric | 2024 |

|---|---|

| Zomato MAU | ~100M |

| Market share (India) | Zomato 36%, Swiggy 56% |

| Multi-homing | ~70% |

What You See Is What You Get

Zomato Porter's Five Forces Analysis

This preview shows the exact Zomato Porter's Five Forces Analysis you'll receive immediately after purchase—no samples, no placeholders. The document displayed here is the complete, professionally formatted analysis, ready for download and use the moment you buy. You're looking at the final file; once payment is complete you'll get instant access to this same document.

From Overview to Strategy Blueprint

Zomato faces intense rivalry from local and global food delivery players, while buyer power and substitute threats rise with convenience apps and cloud kitchens. Supplier influence is moderate, but regulatory and margin pressures squeeze profitability. This snapshot highlights key competitive tensions. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Fragmented restaurant base

Zomato sources from a vast, fragmented base of over 400,000 restaurant partners, diluting any single supplier’s leverage. Many small and medium eateries rely on the platform for discovery and incremental orders, which enables Zomato to enforce standardized commission structures averaging around 20%. Local clusters of popular outlets, however, can still negotiate preferential terms in high-density urban pockets.

Power of marquee brands

In 2024 iconic chains and high-demand cloud kitchens exert elevated bargaining power on Zomato because strong customer pull concentrates order volume among few marquee partners. They secure lower commissions, premium placement, and richer data access, and losing them increases churn and weakens assortment. Zomato routinely counters with co-marketing spends and tailored SLAs to retain these suppliers.

Delivery partner dynamics

Delivery riders are the core supplier of capacity and service quality for Zomato; industry estimates in 2024 put India’s food-delivery gig workforce at roughly 2 million, so labor tightness or regulatory shifts (minimum pay, benefits) can materially raise payout costs and constrain flexibility. Small incentive tweaks have been shown to shift rider availability during peaks, and rider satisfaction and safety directly drive fulfillment reliability and on-time delivery rates.

Input cost pass-through

Rising food and fuel costs are squeezing restaurant margins, driving partners to push back on Zomato commissions and fees while seeking menu markups or reduced discounts, which can make platform prices appear higher to consumers; Zomato must balance take-rates with partner sustainability.

- Proactive analytics to identify margin pressure

- Cost-sharing programs with restaurants

- Flexible take-rates during inflationary periods

Tech and ecosystem vendors

Tech and ecosystem vendors — payment gateways, map/route APIs and ad-tech partners — create clear dependency points for Zomato; while substitutable, switching causes integration costs and operational risk, and as of 2024 outages or fee hikes have compressed margins across the food‑delivery sector. Zomato’s move to diversify partners and build in‑house payment/routing capabilities aims to reduce this exposure and lower supplier bargaining power over time. This shift improves unit‑economics resilience.

- Dependency: payment gateways, map/route APIs, ad‑tech partners

- Risk: switching costs, integration time, outage-driven margin compression (2024 industry impact)

- Mitigation: partner diversification and growing in‑house capabilities

Huge partner base keeps commissions near 20%; chains, riders and tech squeeze margins

Zomato’s supplier power is diluted by 400,000+ restaurant partners, enabling ~20% average commission discipline, but marquee chains and cloud kitchens concentrate volume and extract preferential terms. Delivery riders (~2 million in India, 2024) and rising food/fuel costs pose material wage and payout risk. Tech vendors create switching costs, prompting build‑inhouse moves to protect margins.

| Supplier | Metric | 2024 |

|---|---|---|

| Restaurants | Partner count / avg take-rate | 400,000+ / ~20% |

| Riders | Workforce | ~2,000,000 |

| Tech vendors | Impact | Integration/switching costs |

What is included in the product

Comprehensive Porter's Five Forces analysis of Zomato that evaluates competitive rivalry, buyer and supplier power, threat of new entrants, and substitutes, highlighting key drivers of pricing, profitability, and market structure. Identifies disruptive threats, regulatory and scale barriers, and strategic levers Zomato can use to defend and grow market share.

A concise one-sheet Porter's Five Forces for Zomato that visualizes competitive pressure with an editable radar chart, lets you customize force levels for scenario analysis (pre/post regulation, new entrants) and drops straight into pitch decks—no macros or advanced finance skills required.

Customers Bargaining Power

Low switching costs

Low switching costs mean consumers move between Zomato, Swiggy or direct ordering with minimal friction; 2024 estimates show Swiggy ~56% and Zomato ~36% market share in India, forcing competitive pricing and reliable delivery; app uninstalls/data portability are negligible for dining choice, so loyalty hinges on convenience, breadth of options and trust.

High price sensitivity

High price sensitivity: frequent deal-seeking elevates coupon and surge sensitivity; Zomato’s ~90 million monthly users in 2024 respond strongly to promotions, pushing heavy discounting. Subscriptions (Pro) moderate elasticity but require ongoing discounts and exclusive value to retain members. Visible fees and delivery charges amplify perceived cost, and even 5–10% price gaps can divert orders to rivals.

Information transparency

Ratings, reviews and visible ETAs give Zomato's over 100 million monthly users (2024) the power to demand quality, turning poor fulfillment or inflated menus into rapid churn within hours. Real-time comparison across listings raises relentless pressure on delivery times and service levels, while Zomato must curate credible content and counter review fraud to protect conversion and retention metrics.

Loyalty and habit formation

Zomato’s memberships, wallet credits, and saved preferences reduce churn by creating switching costs, while rival apps’ matched perks in 2024 keep net switching friction low; habit strengthens when ETAs stay within promised windows and quality is consistent, but service breaks quickly erode loyalty and spike cancellations.

- Memberships: retention lever

- Wallet credits: short-term stickiness

- Reliable ETA: habit driver

- Service breaks: rapid churn trigger

Multi-homing behavior

Many users keep multiple delivery apps — 2024 industry surveys indicate about 70% of urban food-delivery customers multi-home, boosting buyer leverage and switching frequency. Cross-app deal hunting compresses contribution margins as platforms run promotions to retain share. Exclusive offerings and a superior UX can reduce churn. Unique restaurant partnerships further anchor demand and raise switching costs.

- multi-homing ~70% (2024)

- promotion-driven margin pressure

- exclusive UX reduces churn

- unique partnerships anchor demand

High multi-homing (~70%) and 100M MAU fuel fierce price wars and rapid churn

Low switching costs and multi-homing (~70% urban, 2024) give customers high leverage; Swiggy ~56% vs Zomato ~36% market share and Zomato ~100M monthly users force aggressive pricing and promotions. Subscriptions and wallets add temporary stickiness but visible fees, ratings and ETAs drive rapid churn when service slips.

| Metric | 2024 |

|---|---|

| Zomato MAU | ~100M |

| Market share (India) | Zomato 36%, Swiggy 56% |

| Multi-homing | ~70% |

What You See Is What You Get

Zomato Porter's Five Forces Analysis

This preview shows the exact Zomato Porter's Five Forces Analysis you'll receive immediately after purchase—no samples, no placeholders. The document displayed here is the complete, professionally formatted analysis, ready for download and use the moment you buy. You're looking at the final file; once payment is complete you'll get instant access to this same document.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Zomato faces intense rivalry from local and global food delivery players, while buyer power and substitute threats rise with convenience apps and cloud kitchens. Supplier influence is moderate, but regulatory and margin pressures squeeze profitability. This snapshot highlights key competitive tensions. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Fragmented restaurant base

Zomato sources from a vast, fragmented base of over 400,000 restaurant partners, diluting any single supplier’s leverage. Many small and medium eateries rely on the platform for discovery and incremental orders, which enables Zomato to enforce standardized commission structures averaging around 20%. Local clusters of popular outlets, however, can still negotiate preferential terms in high-density urban pockets.

Power of marquee brands

In 2024 iconic chains and high-demand cloud kitchens exert elevated bargaining power on Zomato because strong customer pull concentrates order volume among few marquee partners. They secure lower commissions, premium placement, and richer data access, and losing them increases churn and weakens assortment. Zomato routinely counters with co-marketing spends and tailored SLAs to retain these suppliers.

Delivery partner dynamics

Delivery riders are the core supplier of capacity and service quality for Zomato; industry estimates in 2024 put India’s food-delivery gig workforce at roughly 2 million, so labor tightness or regulatory shifts (minimum pay, benefits) can materially raise payout costs and constrain flexibility. Small incentive tweaks have been shown to shift rider availability during peaks, and rider satisfaction and safety directly drive fulfillment reliability and on-time delivery rates.

Input cost pass-through

Rising food and fuel costs are squeezing restaurant margins, driving partners to push back on Zomato commissions and fees while seeking menu markups or reduced discounts, which can make platform prices appear higher to consumers; Zomato must balance take-rates with partner sustainability.

- Proactive analytics to identify margin pressure

- Cost-sharing programs with restaurants

- Flexible take-rates during inflationary periods

Tech and ecosystem vendors

Tech and ecosystem vendors — payment gateways, map/route APIs and ad-tech partners — create clear dependency points for Zomato; while substitutable, switching causes integration costs and operational risk, and as of 2024 outages or fee hikes have compressed margins across the food‑delivery sector. Zomato’s move to diversify partners and build in‑house payment/routing capabilities aims to reduce this exposure and lower supplier bargaining power over time. This shift improves unit‑economics resilience.

- Dependency: payment gateways, map/route APIs, ad‑tech partners

- Risk: switching costs, integration time, outage-driven margin compression (2024 industry impact)

- Mitigation: partner diversification and growing in‑house capabilities

Huge partner base keeps commissions near 20%; chains, riders and tech squeeze margins

Zomato’s supplier power is diluted by 400,000+ restaurant partners, enabling ~20% average commission discipline, but marquee chains and cloud kitchens concentrate volume and extract preferential terms. Delivery riders (~2 million in India, 2024) and rising food/fuel costs pose material wage and payout risk. Tech vendors create switching costs, prompting build‑inhouse moves to protect margins.

| Supplier | Metric | 2024 |

|---|---|---|

| Restaurants | Partner count / avg take-rate | 400,000+ / ~20% |

| Riders | Workforce | ~2,000,000 |

| Tech vendors | Impact | Integration/switching costs |

What is included in the product

Comprehensive Porter's Five Forces analysis of Zomato that evaluates competitive rivalry, buyer and supplier power, threat of new entrants, and substitutes, highlighting key drivers of pricing, profitability, and market structure. Identifies disruptive threats, regulatory and scale barriers, and strategic levers Zomato can use to defend and grow market share.

A concise one-sheet Porter's Five Forces for Zomato that visualizes competitive pressure with an editable radar chart, lets you customize force levels for scenario analysis (pre/post regulation, new entrants) and drops straight into pitch decks—no macros or advanced finance skills required.

Customers Bargaining Power

Low switching costs

Low switching costs mean consumers move between Zomato, Swiggy or direct ordering with minimal friction; 2024 estimates show Swiggy ~56% and Zomato ~36% market share in India, forcing competitive pricing and reliable delivery; app uninstalls/data portability are negligible for dining choice, so loyalty hinges on convenience, breadth of options and trust.

High price sensitivity

High price sensitivity: frequent deal-seeking elevates coupon and surge sensitivity; Zomato’s ~90 million monthly users in 2024 respond strongly to promotions, pushing heavy discounting. Subscriptions (Pro) moderate elasticity but require ongoing discounts and exclusive value to retain members. Visible fees and delivery charges amplify perceived cost, and even 5–10% price gaps can divert orders to rivals.

Information transparency

Ratings, reviews and visible ETAs give Zomato's over 100 million monthly users (2024) the power to demand quality, turning poor fulfillment or inflated menus into rapid churn within hours. Real-time comparison across listings raises relentless pressure on delivery times and service levels, while Zomato must curate credible content and counter review fraud to protect conversion and retention metrics.

Loyalty and habit formation

Zomato’s memberships, wallet credits, and saved preferences reduce churn by creating switching costs, while rival apps’ matched perks in 2024 keep net switching friction low; habit strengthens when ETAs stay within promised windows and quality is consistent, but service breaks quickly erode loyalty and spike cancellations.

- Memberships: retention lever

- Wallet credits: short-term stickiness

- Reliable ETA: habit driver

- Service breaks: rapid churn trigger

Multi-homing behavior

Many users keep multiple delivery apps — 2024 industry surveys indicate about 70% of urban food-delivery customers multi-home, boosting buyer leverage and switching frequency. Cross-app deal hunting compresses contribution margins as platforms run promotions to retain share. Exclusive offerings and a superior UX can reduce churn. Unique restaurant partnerships further anchor demand and raise switching costs.

- multi-homing ~70% (2024)

- promotion-driven margin pressure

- exclusive UX reduces churn

- unique partnerships anchor demand

High multi-homing (~70%) and 100M MAU fuel fierce price wars and rapid churn

Low switching costs and multi-homing (~70% urban, 2024) give customers high leverage; Swiggy ~56% vs Zomato ~36% market share and Zomato ~100M monthly users force aggressive pricing and promotions. Subscriptions and wallets add temporary stickiness but visible fees, ratings and ETAs drive rapid churn when service slips.

| Metric | 2024 |

|---|---|

| Zomato MAU | ~100M |

| Market share (India) | Zomato 36%, Swiggy 56% |

| Multi-homing | ~70% |

What You See Is What You Get

Zomato Porter's Five Forces Analysis

This preview shows the exact Zomato Porter's Five Forces Analysis you'll receive immediately after purchase—no samples, no placeholders. The document displayed here is the complete, professionally formatted analysis, ready for download and use the moment you buy. You're looking at the final file; once payment is complete you'll get instant access to this same document.