ZTE SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

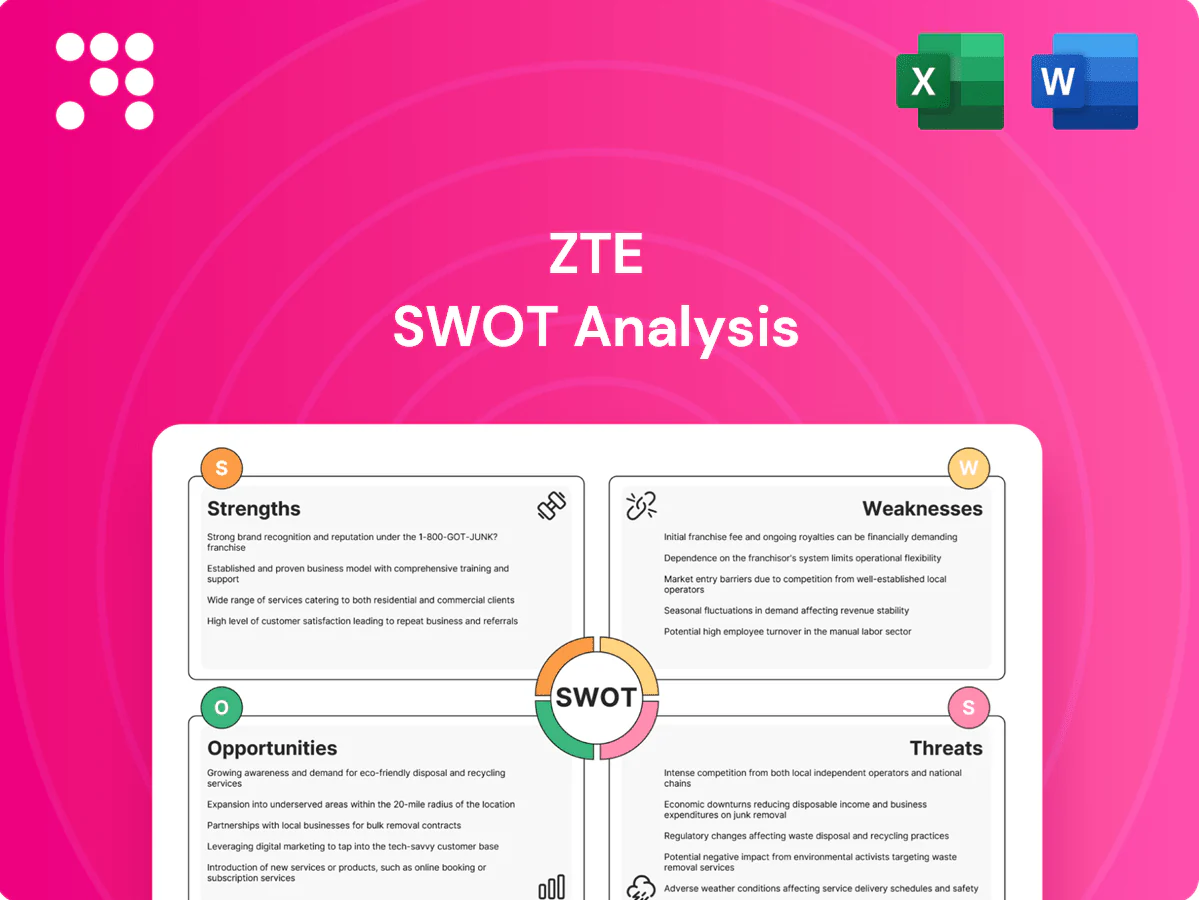

ZTE’s SWOT highlights strong 5G tech and global reach, balanced by geopolitical and supply-chain risks; opportunities include enterprise cloud and emerging markets while competition and sanctions are key threats. Want deeper strategic insight and editable tools? Purchase the full SWOT for a professional Word report and Excel matrix to plan, pitch, or invest with confidence.

Strengths

End-to-end telecom portfolio

ZTE's end-to-end portfolio spans six domains—wireless, wireline, optical, core, data communications and devices—enabling bundled offers across layers. This breadth supports single-vendor bids favored in carrier tenders and lifecycle support, helping win multi-year contracts with operators in over 160 countries. It reduces reliance on any single product line and raises customer switching costs, while cross-selling across domains improves revenue resilience.

Strong R&D and 5G expertise

Heavy R&D — ZTE invested about RMB 21 billion in R&D in 2023, building 5G/5G-Advanced radios, core, transport and AI-driven network automation. Active 3GPP participation and a patent portfolio of over 40,000 filings/grants boost technology leverage and licensing potential. Faster feature rollout improves bid competitiveness and KPIs, positioning ZTE for 6G evolution.

Cost-efficient manufacturing

ZTE leverages scale manufacturing and efficient supply chains to offer competitive pricing without sacrificing performance, supporting large-volume rollouts in price-sensitive emerging markets. Cost leadership is pivotal in winning aggressive tenders and preserves margin defensibility. Its lean cost base also enables flexible commercial models such as managed services; ZTE is listed as 000063.SZ and 0763.HK.

Diverse customer base

ZTE serves carriers, enterprises and consumers, spreading demand across segments and reducing reliance on single-market MNO capex; in 2023 ZTE reported roughly RMB 118 billion revenue, with growing enterprise contracts driving diversification. Enterprise private networks and government projects provided multi-year orders beyond public MNO cycles, while device and CPE lines complement infrastructure sales, smoothing revenue volatility.

- Carrier, enterprise, consumer mix

- Private networks/government diversification

- Device+CPE offsets infra cycles

Rapid deployment and integration

ZTE’s turnkey deployment experience—delivering projects to 320+ operators in 160+ countries—shortens time-to-market for operators and supports both greenfield and brownfield rollouts. Integrated RAN, transport and core with automation reduces rollout risk and accelerates commissioning cycles. Proven deployment playbooks and faster delivery can improve cash conversion by shortening project billing-to-cash timelines.

- 320+ operators served

- 160+ countries reach

- RAN+transport+core integration

- Automation-driven risk reduction

End-to-end portfolio, RMB 21bn R&D and 40,000+ patents drive global 5G/6G wins

ZTE’s end-to-end portfolio, scale manufacturing and RMB 21bn R&D (2023) create cost-competitive, fast-to-market bundled offers that win multi-year contracts with 320+ operators across 160+ countries. A 40,000+ patent portfolio and active 3GPP role accelerate 5G/6G readiness and licensing. Diversified revenues (RMB 118bn in 2023) reduce cycle risk.

| Metric | Value |

|---|---|

| Operators served | 320+ |

| Countries | 160+ |

| R&D 2023 | RMB 21bn |

| Revenue 2023 | RMB 118bn |

| Patents | 40,000+ |

What is included in the product

Delivers a strategic overview of ZTE’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats; examines competitive position, key growth drivers, operational gaps and market risks shaping ZTE’s future.

Provides a concise ZTE SWOT matrix for fast, visual strategy alignment, highlighting telecom-specific strengths, regulatory and supply-chain risks, and growth opportunities for quick stakeholder decisions.

Weaknesses

Geopolitical and compliance overhang

Historical sanctions—notably the 2018 US export ban and a subsequent roughly $1.4 billion remediation package—create lingering regulatory and reputational risk for ZTE. Heightened scrutiny increases compliance costs and can delay contracts, especially in Western markets where some tenders now exclude vendors from sensitive network roles. Governance assurances remain a recurring hurdle in major RFPs.

Brand gap in premium markets

Against incumbents like Ericsson and Nokia—which together accounted for over 50% of global RAN revenue in 2023—ZTE’s brand trust deficit in developed markets (global RAN share under 10% in 2024) raises perceived risk for core network and critical infrastructure awards, compressing attainable pricing or excluding bids; winning work increasingly requires extra certifications and local partnerships.

Dependence on carrier capex cycles

ZTE's large exposure to operator spending ties revenue to macro and spectrum cycles, with carrier networks historically representing roughly two-thirds of group revenue in recent years. Delays in 5G-Advanced rollouts or fiber builds can push project revenue right and make cash flows lumpy; projects are working-capital intensive, increasing receivable days. This makes regional forecasting more complex and sensitive to operator capex timing.

Supply chain sensitivity to export controls

Export controls since 2022–23 restricting access to sub-14nm semiconductors and advanced EDA/IP can tighten ZTE’s component availability, forcing design requalification to alternative suppliers that raises costs and time-to-market; higher buffer inventories increase working capital needs and elevate technology-roadmap risk if high-end chips remain constrained.

- Controls: sub-14nm and advanced EDA/IP restricted since 2022–23

- Requalification: higher NRE and delayed launches

- Working capital: larger inventories required

- Roadmap risk: innovation constrained by high-end chip limits

Margin pressure from pricing intensity

Carrier tenders force aggressive discounts versus low-cost rivals, compressing ASPs; ZTE’s heavy R&D commitment (over 10% of revenue in 2024) and warranty/service obligations further trim gross margins, while devices and CPE remain lower-margin product lines. Sustaining R&D to defend technology leadership while protecting price points strains profitability and EBITDA conversion.

- Carrier tender discounts: elevated vs low-cost peers

- R&D >10% of revenue (2024)

- Services/warranty depress gross margins

- Devices/CPE typically lower-margin

Lingering sanctions, export controls and <10% RAN share amplify carrier and margin risk

Lingering 2018 sanctions (≈$1.4bn remediation) and export controls since 2022–23 raise compliance and supply risks. ZTE’s global RAN share <10% (2024) vs Ericsson+Nokia >50% (2023), weakening trust in developed markets. Carrier exposure (~2/3 group revenue) plus R&D >10% (2024) and tender-driven discounts compress margins.

| Metric | Value |

|---|---|

| 2018 remediation | $1.4bn |

| RAN share (2024) | <10% |

| Top rivals RAN (2023) | >50% |

| Carrier revenue | ~66% |

| R&D (2024) | >10% rev |

Preview Before You Purchase

ZTE SWOT Analysis

This is the actual ZTE SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, with strengths, weaknesses, opportunities and threats clearly laid out. Buy to unlock the complete, editable version available immediately after payment.

Go Beyond the Preview—Access the Full Strategic Report

ZTE’s SWOT highlights strong 5G tech and global reach, balanced by geopolitical and supply-chain risks; opportunities include enterprise cloud and emerging markets while competition and sanctions are key threats. Want deeper strategic insight and editable tools? Purchase the full SWOT for a professional Word report and Excel matrix to plan, pitch, or invest with confidence.

Strengths

End-to-end telecom portfolio

ZTE's end-to-end portfolio spans six domains—wireless, wireline, optical, core, data communications and devices—enabling bundled offers across layers. This breadth supports single-vendor bids favored in carrier tenders and lifecycle support, helping win multi-year contracts with operators in over 160 countries. It reduces reliance on any single product line and raises customer switching costs, while cross-selling across domains improves revenue resilience.

Strong R&D and 5G expertise

Heavy R&D — ZTE invested about RMB 21 billion in R&D in 2023, building 5G/5G-Advanced radios, core, transport and AI-driven network automation. Active 3GPP participation and a patent portfolio of over 40,000 filings/grants boost technology leverage and licensing potential. Faster feature rollout improves bid competitiveness and KPIs, positioning ZTE for 6G evolution.

Cost-efficient manufacturing

ZTE leverages scale manufacturing and efficient supply chains to offer competitive pricing without sacrificing performance, supporting large-volume rollouts in price-sensitive emerging markets. Cost leadership is pivotal in winning aggressive tenders and preserves margin defensibility. Its lean cost base also enables flexible commercial models such as managed services; ZTE is listed as 000063.SZ and 0763.HK.

Diverse customer base

ZTE serves carriers, enterprises and consumers, spreading demand across segments and reducing reliance on single-market MNO capex; in 2023 ZTE reported roughly RMB 118 billion revenue, with growing enterprise contracts driving diversification. Enterprise private networks and government projects provided multi-year orders beyond public MNO cycles, while device and CPE lines complement infrastructure sales, smoothing revenue volatility.

- Carrier, enterprise, consumer mix

- Private networks/government diversification

- Device+CPE offsets infra cycles

Rapid deployment and integration

ZTE’s turnkey deployment experience—delivering projects to 320+ operators in 160+ countries—shortens time-to-market for operators and supports both greenfield and brownfield rollouts. Integrated RAN, transport and core with automation reduces rollout risk and accelerates commissioning cycles. Proven deployment playbooks and faster delivery can improve cash conversion by shortening project billing-to-cash timelines.

- 320+ operators served

- 160+ countries reach

- RAN+transport+core integration

- Automation-driven risk reduction

End-to-end portfolio, RMB 21bn R&D and 40,000+ patents drive global 5G/6G wins

ZTE’s end-to-end portfolio, scale manufacturing and RMB 21bn R&D (2023) create cost-competitive, fast-to-market bundled offers that win multi-year contracts with 320+ operators across 160+ countries. A 40,000+ patent portfolio and active 3GPP role accelerate 5G/6G readiness and licensing. Diversified revenues (RMB 118bn in 2023) reduce cycle risk.

| Metric | Value |

|---|---|

| Operators served | 320+ |

| Countries | 160+ |

| R&D 2023 | RMB 21bn |

| Revenue 2023 | RMB 118bn |

| Patents | 40,000+ |

What is included in the product

Delivers a strategic overview of ZTE’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats; examines competitive position, key growth drivers, operational gaps and market risks shaping ZTE’s future.

Provides a concise ZTE SWOT matrix for fast, visual strategy alignment, highlighting telecom-specific strengths, regulatory and supply-chain risks, and growth opportunities for quick stakeholder decisions.

Weaknesses

Geopolitical and compliance overhang

Historical sanctions—notably the 2018 US export ban and a subsequent roughly $1.4 billion remediation package—create lingering regulatory and reputational risk for ZTE. Heightened scrutiny increases compliance costs and can delay contracts, especially in Western markets where some tenders now exclude vendors from sensitive network roles. Governance assurances remain a recurring hurdle in major RFPs.

Brand gap in premium markets

Against incumbents like Ericsson and Nokia—which together accounted for over 50% of global RAN revenue in 2023—ZTE’s brand trust deficit in developed markets (global RAN share under 10% in 2024) raises perceived risk for core network and critical infrastructure awards, compressing attainable pricing or excluding bids; winning work increasingly requires extra certifications and local partnerships.

Dependence on carrier capex cycles

ZTE's large exposure to operator spending ties revenue to macro and spectrum cycles, with carrier networks historically representing roughly two-thirds of group revenue in recent years. Delays in 5G-Advanced rollouts or fiber builds can push project revenue right and make cash flows lumpy; projects are working-capital intensive, increasing receivable days. This makes regional forecasting more complex and sensitive to operator capex timing.

Supply chain sensitivity to export controls

Export controls since 2022–23 restricting access to sub-14nm semiconductors and advanced EDA/IP can tighten ZTE’s component availability, forcing design requalification to alternative suppliers that raises costs and time-to-market; higher buffer inventories increase working capital needs and elevate technology-roadmap risk if high-end chips remain constrained.

- Controls: sub-14nm and advanced EDA/IP restricted since 2022–23

- Requalification: higher NRE and delayed launches

- Working capital: larger inventories required

- Roadmap risk: innovation constrained by high-end chip limits

Margin pressure from pricing intensity

Carrier tenders force aggressive discounts versus low-cost rivals, compressing ASPs; ZTE’s heavy R&D commitment (over 10% of revenue in 2024) and warranty/service obligations further trim gross margins, while devices and CPE remain lower-margin product lines. Sustaining R&D to defend technology leadership while protecting price points strains profitability and EBITDA conversion.

- Carrier tender discounts: elevated vs low-cost peers

- R&D >10% of revenue (2024)

- Services/warranty depress gross margins

- Devices/CPE typically lower-margin

Lingering sanctions, export controls and <10% RAN share amplify carrier and margin risk

Lingering 2018 sanctions (≈$1.4bn remediation) and export controls since 2022–23 raise compliance and supply risks. ZTE’s global RAN share <10% (2024) vs Ericsson+Nokia >50% (2023), weakening trust in developed markets. Carrier exposure (~2/3 group revenue) plus R&D >10% (2024) and tender-driven discounts compress margins.

| Metric | Value |

|---|---|

| 2018 remediation | $1.4bn |

| RAN share (2024) | <10% |

| Top rivals RAN (2023) | >50% |

| Carrier revenue | ~66% |

| R&D (2024) | >10% rev |

Preview Before You Purchase

ZTE SWOT Analysis

This is the actual ZTE SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, with strengths, weaknesses, opportunities and threats clearly laid out. Buy to unlock the complete, editable version available immediately after payment.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

ZTE’s SWOT highlights strong 5G tech and global reach, balanced by geopolitical and supply-chain risks; opportunities include enterprise cloud and emerging markets while competition and sanctions are key threats. Want deeper strategic insight and editable tools? Purchase the full SWOT for a professional Word report and Excel matrix to plan, pitch, or invest with confidence.

Strengths

End-to-end telecom portfolio

ZTE's end-to-end portfolio spans six domains—wireless, wireline, optical, core, data communications and devices—enabling bundled offers across layers. This breadth supports single-vendor bids favored in carrier tenders and lifecycle support, helping win multi-year contracts with operators in over 160 countries. It reduces reliance on any single product line and raises customer switching costs, while cross-selling across domains improves revenue resilience.

Strong R&D and 5G expertise

Heavy R&D — ZTE invested about RMB 21 billion in R&D in 2023, building 5G/5G-Advanced radios, core, transport and AI-driven network automation. Active 3GPP participation and a patent portfolio of over 40,000 filings/grants boost technology leverage and licensing potential. Faster feature rollout improves bid competitiveness and KPIs, positioning ZTE for 6G evolution.

Cost-efficient manufacturing

ZTE leverages scale manufacturing and efficient supply chains to offer competitive pricing without sacrificing performance, supporting large-volume rollouts in price-sensitive emerging markets. Cost leadership is pivotal in winning aggressive tenders and preserves margin defensibility. Its lean cost base also enables flexible commercial models such as managed services; ZTE is listed as 000063.SZ and 0763.HK.

Diverse customer base

ZTE serves carriers, enterprises and consumers, spreading demand across segments and reducing reliance on single-market MNO capex; in 2023 ZTE reported roughly RMB 118 billion revenue, with growing enterprise contracts driving diversification. Enterprise private networks and government projects provided multi-year orders beyond public MNO cycles, while device and CPE lines complement infrastructure sales, smoothing revenue volatility.

- Carrier, enterprise, consumer mix

- Private networks/government diversification

- Device+CPE offsets infra cycles

Rapid deployment and integration

ZTE’s turnkey deployment experience—delivering projects to 320+ operators in 160+ countries—shortens time-to-market for operators and supports both greenfield and brownfield rollouts. Integrated RAN, transport and core with automation reduces rollout risk and accelerates commissioning cycles. Proven deployment playbooks and faster delivery can improve cash conversion by shortening project billing-to-cash timelines.

- 320+ operators served

- 160+ countries reach

- RAN+transport+core integration

- Automation-driven risk reduction

End-to-end portfolio, RMB 21bn R&D and 40,000+ patents drive global 5G/6G wins

ZTE’s end-to-end portfolio, scale manufacturing and RMB 21bn R&D (2023) create cost-competitive, fast-to-market bundled offers that win multi-year contracts with 320+ operators across 160+ countries. A 40,000+ patent portfolio and active 3GPP role accelerate 5G/6G readiness and licensing. Diversified revenues (RMB 118bn in 2023) reduce cycle risk.

| Metric | Value |

|---|---|

| Operators served | 320+ |

| Countries | 160+ |

| R&D 2023 | RMB 21bn |

| Revenue 2023 | RMB 118bn |

| Patents | 40,000+ |

What is included in the product

Delivers a strategic overview of ZTE’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats; examines competitive position, key growth drivers, operational gaps and market risks shaping ZTE’s future.

Provides a concise ZTE SWOT matrix for fast, visual strategy alignment, highlighting telecom-specific strengths, regulatory and supply-chain risks, and growth opportunities for quick stakeholder decisions.

Weaknesses

Geopolitical and compliance overhang

Historical sanctions—notably the 2018 US export ban and a subsequent roughly $1.4 billion remediation package—create lingering regulatory and reputational risk for ZTE. Heightened scrutiny increases compliance costs and can delay contracts, especially in Western markets where some tenders now exclude vendors from sensitive network roles. Governance assurances remain a recurring hurdle in major RFPs.

Brand gap in premium markets

Against incumbents like Ericsson and Nokia—which together accounted for over 50% of global RAN revenue in 2023—ZTE’s brand trust deficit in developed markets (global RAN share under 10% in 2024) raises perceived risk for core network and critical infrastructure awards, compressing attainable pricing or excluding bids; winning work increasingly requires extra certifications and local partnerships.

Dependence on carrier capex cycles

ZTE's large exposure to operator spending ties revenue to macro and spectrum cycles, with carrier networks historically representing roughly two-thirds of group revenue in recent years. Delays in 5G-Advanced rollouts or fiber builds can push project revenue right and make cash flows lumpy; projects are working-capital intensive, increasing receivable days. This makes regional forecasting more complex and sensitive to operator capex timing.

Supply chain sensitivity to export controls

Export controls since 2022–23 restricting access to sub-14nm semiconductors and advanced EDA/IP can tighten ZTE’s component availability, forcing design requalification to alternative suppliers that raises costs and time-to-market; higher buffer inventories increase working capital needs and elevate technology-roadmap risk if high-end chips remain constrained.

- Controls: sub-14nm and advanced EDA/IP restricted since 2022–23

- Requalification: higher NRE and delayed launches

- Working capital: larger inventories required

- Roadmap risk: innovation constrained by high-end chip limits

Margin pressure from pricing intensity

Carrier tenders force aggressive discounts versus low-cost rivals, compressing ASPs; ZTE’s heavy R&D commitment (over 10% of revenue in 2024) and warranty/service obligations further trim gross margins, while devices and CPE remain lower-margin product lines. Sustaining R&D to defend technology leadership while protecting price points strains profitability and EBITDA conversion.

- Carrier tender discounts: elevated vs low-cost peers

- R&D >10% of revenue (2024)

- Services/warranty depress gross margins

- Devices/CPE typically lower-margin

Lingering sanctions, export controls and <10% RAN share amplify carrier and margin risk

Lingering 2018 sanctions (≈$1.4bn remediation) and export controls since 2022–23 raise compliance and supply risks. ZTE’s global RAN share <10% (2024) vs Ericsson+Nokia >50% (2023), weakening trust in developed markets. Carrier exposure (~2/3 group revenue) plus R&D >10% (2024) and tender-driven discounts compress margins.

| Metric | Value |

|---|---|

| 2018 remediation | $1.4bn |

| RAN share (2024) | <10% |

| Top rivals RAN (2023) | >50% |

| Carrier revenue | ~66% |

| R&D (2024) | >10% rev |

Preview Before You Purchase

ZTE SWOT Analysis

This is the actual ZTE SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, with strengths, weaknesses, opportunities and threats clearly laid out. Buy to unlock the complete, editable version available immediately after payment.