Zurel Group B.V SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Zurel Group B.V. combines niche market expertise with scalable tech capabilities, yet faces regulatory and competitive pressures that could constrain growth; our concise preview highlights key signals and tactical implications. Want the full picture with actionable strategies and editable deliverables? Purchase the complete SWOT analysis for a professional Word report and Excel matrix to plan, pitch, or invest with confidence.

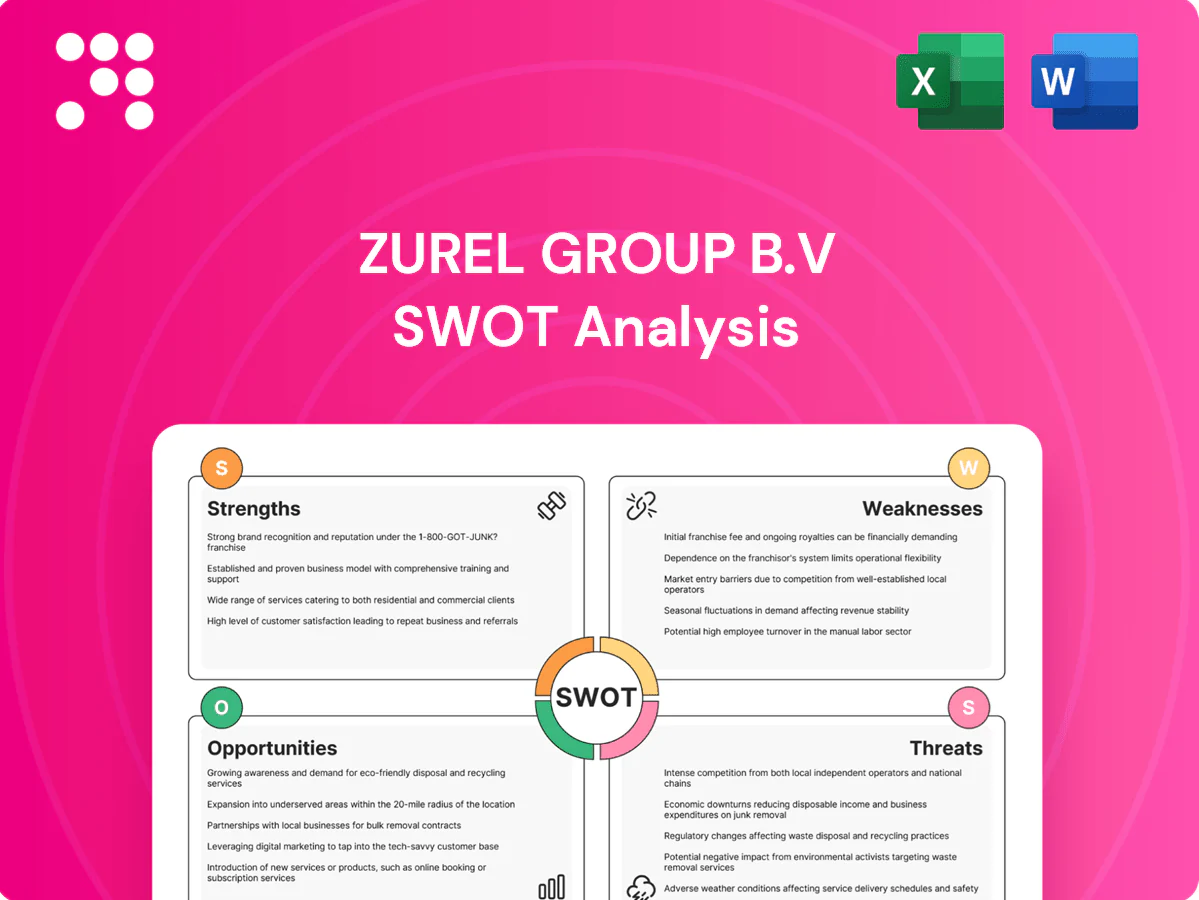

Strengths

Diverse lodging portfolio

Offering holiday homes, apartments, and villas widens appeal across families, couples, and groups, enabling tiered pricing and targeted packages; diversified portfolios typically reduce seasonality volatility (peak vs off-peak occupancy swings often reach 20–30%) and help smooth price sensitivity. This mix supports occupancy optimization across seasons and improves revenue resilience.

End-to-end park management

End-to-end park management—development, operations, rentals and maintenance—lets Zurel Group B.V. control quality and cut handoff frictions that drive cost leakage, improving operating margins. Integrated data loops from operations guide targeted asset upgrades and maintenance scheduling, supporting uptime targets and guest experience. Industry attendance rebounded to ~1.66 billion (TEA/AECOM 2024), amplifying value of consistent brand delivery and higher guest satisfaction.

Quality-focused guest experience

Positioning around high-quality leisure drives premium ADR potential, supported by global RevPAR growth of about 11% YoY in 2023 (STR) as leisure demand shifts to upscale stays. Consistent service and well-maintained facilities boost reviews and repeat stays; repeat guests typically cost 5x less to acquire than new ones. Strong NPS lowers distribution spend over time and underpins pricing power during peak periods.

Recurring revenue streams

Recurring rental income and management fees deliver predictable cash flows for Zurel Group B.V., while portfolio effects spread exposure and reduce single-asset risk.

Long booking windows in holiday parks improve revenue visibility, strengthening financing terms and investor appeal.

- reliable cash flows

- diversification benefits

- booking-led forecasting

- better financing & investor interest

Attractive investment platform

Holiday parks are tangible, income-producing assets attractive to yield-seeking capital, often achieving peak-season occupancy of 75-85% and stable year-round cashflows. Professional asset management can unlock value via targeted capex and revenue management, driving RevPAR uplifts commonly in the 8-12% range. The platform can scale through bolt-on acquisitions, enabling portfolio growth and multiple return pathways.

- Income stability: high occupancy (75-85%)

- Value creation: RevPAR uplift 8-12% via capex/rev mgmt

- Scalability: bolt-ons enable rapid portfolio expansion

Diversified holiday parks boost occupancy, lift RevPAR 8-12% amid STR +11% growth

Diversified holiday homes, apartments and villas drive occupancy resilience (peak 75–85%) and smooth seasonality (occupancy swings 20–30%). End-to-end park management cuts costs and boosts RevPAR (+8–12% via capex/rev‑mgmt). Leisure premium positioning supports ADR/RevPAR growth (STR RevPAR +11% YoY 2023); TEA/AECOM attendance ~1.66bn (2024).

| Metric | Value |

|---|---|

| Peak occupancy | 75–85% |

| RevPAR uplift | 8–12% |

| RevPAR growth 2023 | +11% (STR) |

| Global attendance 2024 | ~1.66bn (TEA/AECOM) |

What is included in the product

Provides a clear SWOT framework analyzing Zurel Group B.V’s internal capabilities, market strengths, growth opportunities, and external threats shaping its strategic trajectory.

Provides a concise SWOT matrix tailored to Zurel Group B.V, quickly surfacing strategic risks and growth levers to enable fast stakeholder alignment and actionable planning.

Weaknesses

Capital-intensive assets

Development and refurbishment demand high upfront capex, with payback often stretched and sensitive to occupancy rates; prolonged vacancies amplify returns volatility. Heavy balance-sheet leverage limits strategic flexibility and borrowing capacity. Recurring maintenance capex is non-deferrable and continuously drains operating cash flow.

Seasonality and demand swings

Leisure travel concentrates in holidays and summer, driving summer occupancy often 65–85% versus 30–50% in shoulder months (STR: US 2023 avg occupancy ~65%). Fixed operating costs (rent, utilities, debt service) keep margins compressed off-peak, forcing promotions that can cut ADR 10–20% to defend occupancy, while rigid staffing models struggle to flex efficiently.

Geographic concentration risk

Clustered park locations expose Zurel Group B.V to concentrated local shocks where a single regional downturn or disaster can disproportionately dent revenue; climate-driven weather variability has increased extreme events, amplifying demand swings for outdoor leisure. Regulatory change in one market can force portfolio-wide re-pricing or closures, and management bandwidth may constrain geographic diversification, limiting the firm's ability to reallocate capital swiftly.

Operational complexity

Running multiple properties with diverse unit types raises coordination needs across reservations, pricing and guest services, making SOP standardization while preserving local flair difficult; IT, housekeeping and maintenance synchronization are execution-heavy and small failures can rapidly harm reviews and bookings.

- High coordination overhead

- Hard to standardize vs local identity

- IT/housekeeping/maintenance sync risk

- Small failures quickly hit revenue

Distribution dependence

Zurel Group B.V. depends heavily on OTAs, which typically charge 15–25% commissions (industry reports, 2024), compressing room-level margins; sudden algorithm changes can sharply reduce OTA visibility and bookings; building direct channels requires sustained marketing spend and higher customer acquisition costs; optimizing channel mix to hit industry direct-booking targets of ~30–40% remains an ongoing operational challenge.

- OTA-commissions: 15–25% (2024)

- Visibility-risk: algorithm-driven traffic drops

- Direct-CAC: sustained marketing required

- Channel-mix: target ~30–40% direct

Seasonality, heavy capex and 15–25% OTA commissions squeeze margins

High upfront capex with stretched payback and vacancy-sensitive returns; recurring maintenance capex continuously drains cash. Strong seasonality: summer occupancy 65–85% vs shoulder 30–50% (STR; US 2023 avg ~65%), compressing off-peak margins. Heavy balance-sheet leverage and concentrated park clusters raise exposure to regional shocks and regulatory shifts. OTA dependence (commissions 15–25% in 2024) limits margins; direct-booking target ~30–40% remains unmet.

| Weakness | Metric / 2023–24 |

|---|---|

| Seasonality | Summer 65–85% vs shoulder 30–50% (STR) |

| OTA commissions | 15–25% (2024) |

| Direct bookings | Target ~30–40% |

Same Document Delivered

Zurel Group B.V SWOT Analysis

This is the actual SWOT analysis document you'll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report for Zurel Group B.V., covering strengths, weaknesses, opportunities and threats with actionable insights. Purchase unlocks the complete, editable version available for immediate download.

Dive Deeper Into the Company’s Strategic Blueprint

Zurel Group B.V. combines niche market expertise with scalable tech capabilities, yet faces regulatory and competitive pressures that could constrain growth; our concise preview highlights key signals and tactical implications. Want the full picture with actionable strategies and editable deliverables? Purchase the complete SWOT analysis for a professional Word report and Excel matrix to plan, pitch, or invest with confidence.

Strengths

Diverse lodging portfolio

Offering holiday homes, apartments, and villas widens appeal across families, couples, and groups, enabling tiered pricing and targeted packages; diversified portfolios typically reduce seasonality volatility (peak vs off-peak occupancy swings often reach 20–30%) and help smooth price sensitivity. This mix supports occupancy optimization across seasons and improves revenue resilience.

End-to-end park management

End-to-end park management—development, operations, rentals and maintenance—lets Zurel Group B.V. control quality and cut handoff frictions that drive cost leakage, improving operating margins. Integrated data loops from operations guide targeted asset upgrades and maintenance scheduling, supporting uptime targets and guest experience. Industry attendance rebounded to ~1.66 billion (TEA/AECOM 2024), amplifying value of consistent brand delivery and higher guest satisfaction.

Quality-focused guest experience

Positioning around high-quality leisure drives premium ADR potential, supported by global RevPAR growth of about 11% YoY in 2023 (STR) as leisure demand shifts to upscale stays. Consistent service and well-maintained facilities boost reviews and repeat stays; repeat guests typically cost 5x less to acquire than new ones. Strong NPS lowers distribution spend over time and underpins pricing power during peak periods.

Recurring revenue streams

Recurring rental income and management fees deliver predictable cash flows for Zurel Group B.V., while portfolio effects spread exposure and reduce single-asset risk.

Long booking windows in holiday parks improve revenue visibility, strengthening financing terms and investor appeal.

- reliable cash flows

- diversification benefits

- booking-led forecasting

- better financing & investor interest

Attractive investment platform

Holiday parks are tangible, income-producing assets attractive to yield-seeking capital, often achieving peak-season occupancy of 75-85% and stable year-round cashflows. Professional asset management can unlock value via targeted capex and revenue management, driving RevPAR uplifts commonly in the 8-12% range. The platform can scale through bolt-on acquisitions, enabling portfolio growth and multiple return pathways.

- Income stability: high occupancy (75-85%)

- Value creation: RevPAR uplift 8-12% via capex/rev mgmt

- Scalability: bolt-ons enable rapid portfolio expansion

Diversified holiday parks boost occupancy, lift RevPAR 8-12% amid STR +11% growth

Diversified holiday homes, apartments and villas drive occupancy resilience (peak 75–85%) and smooth seasonality (occupancy swings 20–30%). End-to-end park management cuts costs and boosts RevPAR (+8–12% via capex/rev‑mgmt). Leisure premium positioning supports ADR/RevPAR growth (STR RevPAR +11% YoY 2023); TEA/AECOM attendance ~1.66bn (2024).

| Metric | Value |

|---|---|

| Peak occupancy | 75–85% |

| RevPAR uplift | 8–12% |

| RevPAR growth 2023 | +11% (STR) |

| Global attendance 2024 | ~1.66bn (TEA/AECOM) |

What is included in the product

Provides a clear SWOT framework analyzing Zurel Group B.V’s internal capabilities, market strengths, growth opportunities, and external threats shaping its strategic trajectory.

Provides a concise SWOT matrix tailored to Zurel Group B.V, quickly surfacing strategic risks and growth levers to enable fast stakeholder alignment and actionable planning.

Weaknesses

Capital-intensive assets

Development and refurbishment demand high upfront capex, with payback often stretched and sensitive to occupancy rates; prolonged vacancies amplify returns volatility. Heavy balance-sheet leverage limits strategic flexibility and borrowing capacity. Recurring maintenance capex is non-deferrable and continuously drains operating cash flow.

Seasonality and demand swings

Leisure travel concentrates in holidays and summer, driving summer occupancy often 65–85% versus 30–50% in shoulder months (STR: US 2023 avg occupancy ~65%). Fixed operating costs (rent, utilities, debt service) keep margins compressed off-peak, forcing promotions that can cut ADR 10–20% to defend occupancy, while rigid staffing models struggle to flex efficiently.

Geographic concentration risk

Clustered park locations expose Zurel Group B.V to concentrated local shocks where a single regional downturn or disaster can disproportionately dent revenue; climate-driven weather variability has increased extreme events, amplifying demand swings for outdoor leisure. Regulatory change in one market can force portfolio-wide re-pricing or closures, and management bandwidth may constrain geographic diversification, limiting the firm's ability to reallocate capital swiftly.

Operational complexity

Running multiple properties with diverse unit types raises coordination needs across reservations, pricing and guest services, making SOP standardization while preserving local flair difficult; IT, housekeeping and maintenance synchronization are execution-heavy and small failures can rapidly harm reviews and bookings.

- High coordination overhead

- Hard to standardize vs local identity

- IT/housekeeping/maintenance sync risk

- Small failures quickly hit revenue

Distribution dependence

Zurel Group B.V. depends heavily on OTAs, which typically charge 15–25% commissions (industry reports, 2024), compressing room-level margins; sudden algorithm changes can sharply reduce OTA visibility and bookings; building direct channels requires sustained marketing spend and higher customer acquisition costs; optimizing channel mix to hit industry direct-booking targets of ~30–40% remains an ongoing operational challenge.

- OTA-commissions: 15–25% (2024)

- Visibility-risk: algorithm-driven traffic drops

- Direct-CAC: sustained marketing required

- Channel-mix: target ~30–40% direct

Seasonality, heavy capex and 15–25% OTA commissions squeeze margins

High upfront capex with stretched payback and vacancy-sensitive returns; recurring maintenance capex continuously drains cash. Strong seasonality: summer occupancy 65–85% vs shoulder 30–50% (STR; US 2023 avg ~65%), compressing off-peak margins. Heavy balance-sheet leverage and concentrated park clusters raise exposure to regional shocks and regulatory shifts. OTA dependence (commissions 15–25% in 2024) limits margins; direct-booking target ~30–40% remains unmet.

| Weakness | Metric / 2023–24 |

|---|---|

| Seasonality | Summer 65–85% vs shoulder 30–50% (STR) |

| OTA commissions | 15–25% (2024) |

| Direct bookings | Target ~30–40% |

Same Document Delivered

Zurel Group B.V SWOT Analysis

This is the actual SWOT analysis document you'll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report for Zurel Group B.V., covering strengths, weaknesses, opportunities and threats with actionable insights. Purchase unlocks the complete, editable version available for immediate download.

Original: $10.00

-65%$10.00

$3.50Description

Dive Deeper Into the Company’s Strategic Blueprint

Zurel Group B.V. combines niche market expertise with scalable tech capabilities, yet faces regulatory and competitive pressures that could constrain growth; our concise preview highlights key signals and tactical implications. Want the full picture with actionable strategies and editable deliverables? Purchase the complete SWOT analysis for a professional Word report and Excel matrix to plan, pitch, or invest with confidence.

Strengths

Diverse lodging portfolio

Offering holiday homes, apartments, and villas widens appeal across families, couples, and groups, enabling tiered pricing and targeted packages; diversified portfolios typically reduce seasonality volatility (peak vs off-peak occupancy swings often reach 20–30%) and help smooth price sensitivity. This mix supports occupancy optimization across seasons and improves revenue resilience.

End-to-end park management

End-to-end park management—development, operations, rentals and maintenance—lets Zurel Group B.V. control quality and cut handoff frictions that drive cost leakage, improving operating margins. Integrated data loops from operations guide targeted asset upgrades and maintenance scheduling, supporting uptime targets and guest experience. Industry attendance rebounded to ~1.66 billion (TEA/AECOM 2024), amplifying value of consistent brand delivery and higher guest satisfaction.

Quality-focused guest experience

Positioning around high-quality leisure drives premium ADR potential, supported by global RevPAR growth of about 11% YoY in 2023 (STR) as leisure demand shifts to upscale stays. Consistent service and well-maintained facilities boost reviews and repeat stays; repeat guests typically cost 5x less to acquire than new ones. Strong NPS lowers distribution spend over time and underpins pricing power during peak periods.

Recurring revenue streams

Recurring rental income and management fees deliver predictable cash flows for Zurel Group B.V., while portfolio effects spread exposure and reduce single-asset risk.

Long booking windows in holiday parks improve revenue visibility, strengthening financing terms and investor appeal.

- reliable cash flows

- diversification benefits

- booking-led forecasting

- better financing & investor interest

Attractive investment platform

Holiday parks are tangible, income-producing assets attractive to yield-seeking capital, often achieving peak-season occupancy of 75-85% and stable year-round cashflows. Professional asset management can unlock value via targeted capex and revenue management, driving RevPAR uplifts commonly in the 8-12% range. The platform can scale through bolt-on acquisitions, enabling portfolio growth and multiple return pathways.

- Income stability: high occupancy (75-85%)

- Value creation: RevPAR uplift 8-12% via capex/rev mgmt

- Scalability: bolt-ons enable rapid portfolio expansion

Diversified holiday parks boost occupancy, lift RevPAR 8-12% amid STR +11% growth

Diversified holiday homes, apartments and villas drive occupancy resilience (peak 75–85%) and smooth seasonality (occupancy swings 20–30%). End-to-end park management cuts costs and boosts RevPAR (+8–12% via capex/rev‑mgmt). Leisure premium positioning supports ADR/RevPAR growth (STR RevPAR +11% YoY 2023); TEA/AECOM attendance ~1.66bn (2024).

| Metric | Value |

|---|---|

| Peak occupancy | 75–85% |

| RevPAR uplift | 8–12% |

| RevPAR growth 2023 | +11% (STR) |

| Global attendance 2024 | ~1.66bn (TEA/AECOM) |

What is included in the product

Provides a clear SWOT framework analyzing Zurel Group B.V’s internal capabilities, market strengths, growth opportunities, and external threats shaping its strategic trajectory.

Provides a concise SWOT matrix tailored to Zurel Group B.V, quickly surfacing strategic risks and growth levers to enable fast stakeholder alignment and actionable planning.

Weaknesses

Capital-intensive assets

Development and refurbishment demand high upfront capex, with payback often stretched and sensitive to occupancy rates; prolonged vacancies amplify returns volatility. Heavy balance-sheet leverage limits strategic flexibility and borrowing capacity. Recurring maintenance capex is non-deferrable and continuously drains operating cash flow.

Seasonality and demand swings

Leisure travel concentrates in holidays and summer, driving summer occupancy often 65–85% versus 30–50% in shoulder months (STR: US 2023 avg occupancy ~65%). Fixed operating costs (rent, utilities, debt service) keep margins compressed off-peak, forcing promotions that can cut ADR 10–20% to defend occupancy, while rigid staffing models struggle to flex efficiently.

Geographic concentration risk

Clustered park locations expose Zurel Group B.V to concentrated local shocks where a single regional downturn or disaster can disproportionately dent revenue; climate-driven weather variability has increased extreme events, amplifying demand swings for outdoor leisure. Regulatory change in one market can force portfolio-wide re-pricing or closures, and management bandwidth may constrain geographic diversification, limiting the firm's ability to reallocate capital swiftly.

Operational complexity

Running multiple properties with diverse unit types raises coordination needs across reservations, pricing and guest services, making SOP standardization while preserving local flair difficult; IT, housekeeping and maintenance synchronization are execution-heavy and small failures can rapidly harm reviews and bookings.

- High coordination overhead

- Hard to standardize vs local identity

- IT/housekeeping/maintenance sync risk

- Small failures quickly hit revenue

Distribution dependence

Zurel Group B.V. depends heavily on OTAs, which typically charge 15–25% commissions (industry reports, 2024), compressing room-level margins; sudden algorithm changes can sharply reduce OTA visibility and bookings; building direct channels requires sustained marketing spend and higher customer acquisition costs; optimizing channel mix to hit industry direct-booking targets of ~30–40% remains an ongoing operational challenge.

- OTA-commissions: 15–25% (2024)

- Visibility-risk: algorithm-driven traffic drops

- Direct-CAC: sustained marketing required

- Channel-mix: target ~30–40% direct

Seasonality, heavy capex and 15–25% OTA commissions squeeze margins

High upfront capex with stretched payback and vacancy-sensitive returns; recurring maintenance capex continuously drains cash. Strong seasonality: summer occupancy 65–85% vs shoulder 30–50% (STR; US 2023 avg ~65%), compressing off-peak margins. Heavy balance-sheet leverage and concentrated park clusters raise exposure to regional shocks and regulatory shifts. OTA dependence (commissions 15–25% in 2024) limits margins; direct-booking target ~30–40% remains unmet.

| Weakness | Metric / 2023–24 |

|---|---|

| Seasonality | Summer 65–85% vs shoulder 30–50% (STR) |

| OTA commissions | 15–25% (2024) |

| Direct bookings | Target ~30–40% |

Same Document Delivered

Zurel Group B.V SWOT Analysis

This is the actual SWOT analysis document you'll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report for Zurel Group B.V., covering strengths, weaknesses, opportunities and threats with actionable insights. Purchase unlocks the complete, editable version available for immediate download.