Zhongyuan Bank Boston Consulting Group Matrix

Download Your Competitive Advantage

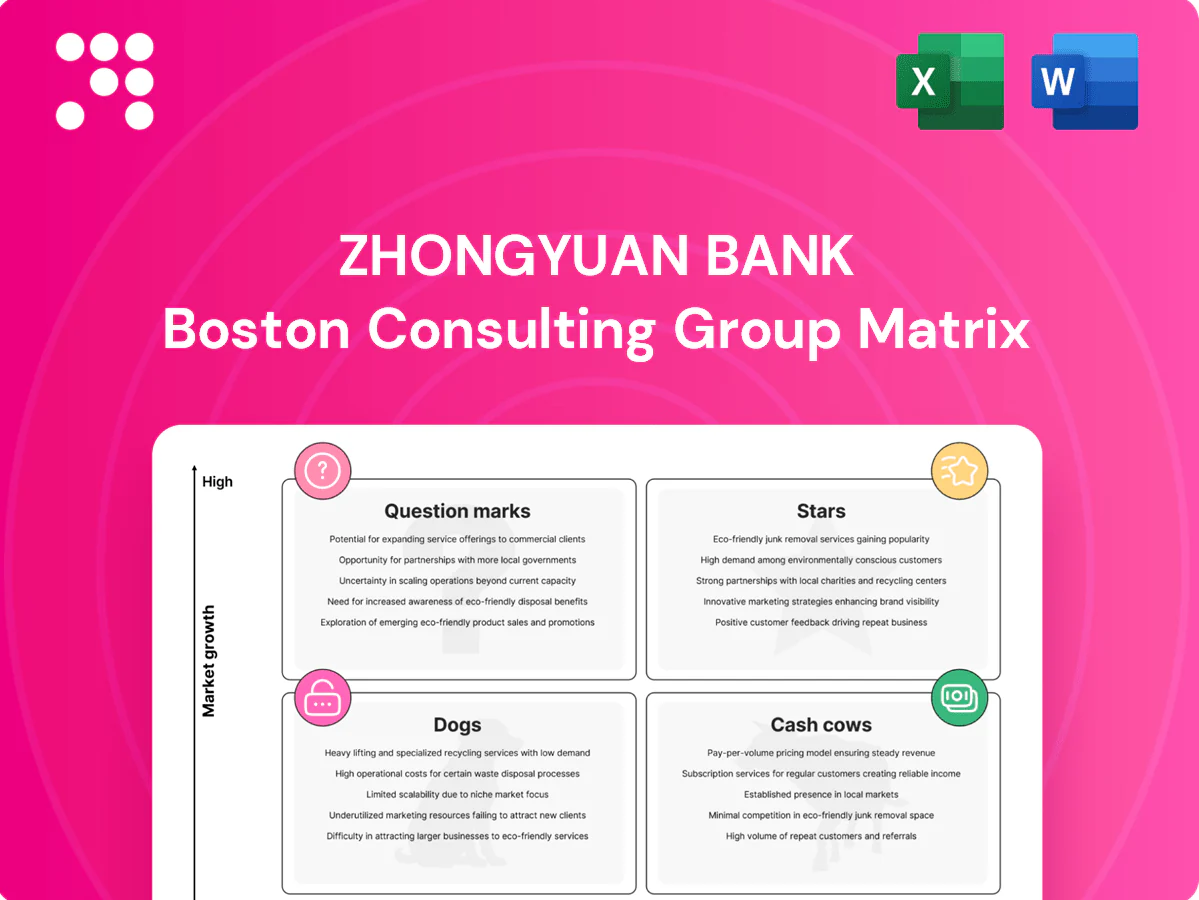

Curious where Zhongyuan Bank’s products land—Stars, Cash Cows, Dogs, or Question Marks? This snapshot teases positioning and trends, but the full BCG Matrix gives quadrant-by-quadrant data, strategic recommendations, and ready-to-use Word + Excel files to act on. Purchase the complete report for the clarity you need to allocate capital and move fast.

Stars

Digital payments & mobile app growth

Mobile usage is surging: Henan hosts about 99 million residents and China had roughly 1.04 billion mobile payment users in 2024, so Zhongyuan’s app can ride that wave hard locally. High transaction velocity, daily engagement and sticky behavior show classic Star dynamics. Keep pouring into UX, QR rails and merchant acceptance to hold share now and let it graduate into a cash-printing platform later.

SME lending with supply‑chain finance

Manufacturing and trading SMEs in Henan (province population ~99 million) are expanding and, with Chinese SMEs contributing roughly 60% of GDP and 80% of urban employment, they demand fast, data‑driven credit. Bundling receivables financing with collections creates scale and switching costs for Zhongyuan Bank. Growth is hot and cash needs heavy—this Star needs more limits, analytics, and risk tech to win share today and harvest tomorrow.

Retail deposits via ecosystem partnerships

Payroll tie‑ups and integration into digital ecosystems are rapidly capturing low‑cost retail deposits for Zhongyuan Bank, driving balance growth that can outpace peers. Low funding cost combined with rising balances creates clear leadership potential if APIs, mini‑programs and sticky features are expanded. Defend acquired share vigorously to convert scale into sustained margin power.

Wealth management for mass affluent

Household investable assets in the province rose 11% YoY to CNY 1.2 trillion in 2024, making advisory‑led wealth management for the mass affluent a clear Star: simple, transparent products are scaling rapidly, with advisory AUA up ~35% YoY. It consumes marketing and talent cash now, but client lifetime value yields ROE above 18%, justifying the investment. Focus on strict suitability and digital onboarding (conversion ~68%, retention ~82%) to cement leadership.

- 2024: investable assets +11% to CNY 1.2T

- Advisory AUA +35% YoY

- Digital onboarding conversion ~68%

- Client retention ~82%

- Target ROE >18%—invest in marketing & talent now

Green credit & ESG‑linked lending

Policy tailwinds and corporate transition plans drove rapid demand for Green credit & ESG‑linked lending at Zhongyuan Bank in 2024, with China’s green loan origination reported up ~15% year‑on‑year and ESG‑linked deal volume rising globally; first‑mover structures (equipment upgrades, clean energy, efficiency retrofits) create a durable moat despite higher underwriting and verification costs.

- growth: 2024 market expansion ~15%

- moat: first‑mover tech & retrofit financing

- cost: higher underwriting/verification spend

- action: build frameworks to lock marquee clients & volume

Henan surge: mobile pay, mass-affluent assets & green loans - invest in UX, risk tech

Zhongyuan’s Stars—mobile payments, SME receivables, payroll deposits and mass‑affluent wealth—show high growth and stickiness in 2024: Henan pop ~99M, China mobile pay users ~1.04B, investable assets CNY1.2T (+11%), advisory AUA +35%, onboarding conv ~68%, retention ~82%, green lending growth ~15%; invest in UX, risk tech, APIs and talent to convert share into durable margins.

| Metric | 2024 |

|---|---|

| Henan population | ~99M |

| China mobile pay users | ~1.04B |

| Investable assets | CNY1.2T (+11%) |

| Advisory AUA | +35% YoY |

| Onboarding conv / Retention | 68% / 82% |

| Green loan growth | ~15% |

What is included in the product

Clear BCG Matrix for Zhongyuan Bank: strategic moves for Stars, Cash Cows, Question Marks and Dogs with investment and divestment guidance.

One-page BCG matrix for Zhongyuan Bank - maps units by growth/share, simplifying strategy decisions for execs.

Cash Cows

Core corporate deposits from anchor clients

Core corporate deposits from anchor clients show stable balances, very low churn and an attractive low single-digit funding cost in 2024, marking them as the textbook cash cow. The Henan relationship-driven market yields light maintenance spend while providing steady NII support. Prioritize service quality, digitize treasury ops to cut cycle times, and quietly milk the spread.

Municipal/payment & settlement services

Municipal/payment & settlement services handle steady payroll, tax, utility and public-service inflows that scale predictably; typical sector growth is modest at roughly 3–5% annually while margins remain durable with minimal promotion. Integration once, revenue forever applies as recurring fee per transaction sustains revenues; operational focus is on 99.9%+ uptime and reliability. Invest just enough in monitoring and redundancy to preserve the moat.

Mortgages in core city clusters

Mortgages in core city clusters are a cash cow for Zhongyuan Bank with a large outstanding portfolio (about RMB 120bn in 2024) and manageable prepayment (approx. 15% CPR), while NPLs remain low at under 1%, reflecting well understood credit risk. Market growth is muted at ~2–3% p.a. but the bank’s share is entrenched. Cross‑selling insurance and cards can boost revenue per household by ~20%, and optimizing capital allocation and servicing efficiency will preserve cash generation.

Transaction banking for established corporates

Transaction banking for established corporates—cash management, collections, and liquidity sweeps—generate steady fee and float income and exhibit mature, sticky relationships with low churn, fitting a classic cash cow profile. Incremental upgrades and modular pricing yield higher ROI than large IT spends. Prioritize straight‑through processing and strict pricing discipline to protect margins.

- Cash management: recurring fees

- Collections: low churn, high retention

- Liquidity sweeps: reliable float

- Strategy: incremental upgrades, STP, pricing discipline

Vanilla short‑term working capital loans

Vanilla short-term working capital loans are plain, priced and predictable, anchored to the 1-year LPR at 3.65% in 2024; competition is stable and underwriting models are seasoned, producing steady utilization near 85% and modest net yields around 2.5–3.0%.

Margins aren’t flashy but high utilization converts into reliable fee and interest cash flow; maintain strict credit hygiene and automate renewals to lift free cash flow by an estimated 3–5% annually.

- Product: short-term WC loans

- 2024 anchor: 1Y LPR 3.65%

- Utilization: ~85%

- Yield range: 2.5–3.0%

- Recommended: credit hygiene + automated renewals

Core deposits drive NII; RMB 120bn mortgages & reliable WC loans - digitize, price tight

Core deposits (low single‑digit funding cost) and municipal/payment flows provide steady NII; mortgages (RMB 120bn in 2024, CPR ~15%, NPL <1%) and transaction banking deliver recurring fees; short‑term WC loans (1Y LPR 3.65%, util ~85%, yield 2.5–3.0%) are predictable cash generators—prioritize digitization, STP and pricing discipline.

| Product | 2024 metric | Note |

|---|---|---|

| Core deposits | Low single‑digit cost | High stability |

| Municipal/payments | Growth 3–5% p.a. | Recurring fees, 99.9% uptime |

| Mortgages | RMB 120bn; CPR 15%; NPL <1% | Cross‑sell +20% revenue/HH |

| WC loans | 1Y LPR 3.65%; util 85%; yield 2.5–3.0% | Predictable, automate renewals |

What You’re Viewing Is Included

Zhongyuan Bank BCG Matrix

The file you're previewing is the exact Zhongyuan Bank BCG Matrix report you'll receive after purchase. No watermarks, no demo content—just the fully formatted, analysis-ready document designed for strategic decisions. Once bought, the same file is yours to download, edit, print, or present. Quick, professional, and made to plug straight into your planning workflow.

Download Your Competitive Advantage

Curious where Zhongyuan Bank’s products land—Stars, Cash Cows, Dogs, or Question Marks? This snapshot teases positioning and trends, but the full BCG Matrix gives quadrant-by-quadrant data, strategic recommendations, and ready-to-use Word + Excel files to act on. Purchase the complete report for the clarity you need to allocate capital and move fast.

Stars

Digital payments & mobile app growth

Mobile usage is surging: Henan hosts about 99 million residents and China had roughly 1.04 billion mobile payment users in 2024, so Zhongyuan’s app can ride that wave hard locally. High transaction velocity, daily engagement and sticky behavior show classic Star dynamics. Keep pouring into UX, QR rails and merchant acceptance to hold share now and let it graduate into a cash-printing platform later.

SME lending with supply‑chain finance

Manufacturing and trading SMEs in Henan (province population ~99 million) are expanding and, with Chinese SMEs contributing roughly 60% of GDP and 80% of urban employment, they demand fast, data‑driven credit. Bundling receivables financing with collections creates scale and switching costs for Zhongyuan Bank. Growth is hot and cash needs heavy—this Star needs more limits, analytics, and risk tech to win share today and harvest tomorrow.

Retail deposits via ecosystem partnerships

Payroll tie‑ups and integration into digital ecosystems are rapidly capturing low‑cost retail deposits for Zhongyuan Bank, driving balance growth that can outpace peers. Low funding cost combined with rising balances creates clear leadership potential if APIs, mini‑programs and sticky features are expanded. Defend acquired share vigorously to convert scale into sustained margin power.

Wealth management for mass affluent

Household investable assets in the province rose 11% YoY to CNY 1.2 trillion in 2024, making advisory‑led wealth management for the mass affluent a clear Star: simple, transparent products are scaling rapidly, with advisory AUA up ~35% YoY. It consumes marketing and talent cash now, but client lifetime value yields ROE above 18%, justifying the investment. Focus on strict suitability and digital onboarding (conversion ~68%, retention ~82%) to cement leadership.

- 2024: investable assets +11% to CNY 1.2T

- Advisory AUA +35% YoY

- Digital onboarding conversion ~68%

- Client retention ~82%

- Target ROE >18%—invest in marketing & talent now

Green credit & ESG‑linked lending

Policy tailwinds and corporate transition plans drove rapid demand for Green credit & ESG‑linked lending at Zhongyuan Bank in 2024, with China’s green loan origination reported up ~15% year‑on‑year and ESG‑linked deal volume rising globally; first‑mover structures (equipment upgrades, clean energy, efficiency retrofits) create a durable moat despite higher underwriting and verification costs.

- growth: 2024 market expansion ~15%

- moat: first‑mover tech & retrofit financing

- cost: higher underwriting/verification spend

- action: build frameworks to lock marquee clients & volume

Henan surge: mobile pay, mass-affluent assets & green loans - invest in UX, risk tech

Zhongyuan’s Stars—mobile payments, SME receivables, payroll deposits and mass‑affluent wealth—show high growth and stickiness in 2024: Henan pop ~99M, China mobile pay users ~1.04B, investable assets CNY1.2T (+11%), advisory AUA +35%, onboarding conv ~68%, retention ~82%, green lending growth ~15%; invest in UX, risk tech, APIs and talent to convert share into durable margins.

| Metric | 2024 |

|---|---|

| Henan population | ~99M |

| China mobile pay users | ~1.04B |

| Investable assets | CNY1.2T (+11%) |

| Advisory AUA | +35% YoY |

| Onboarding conv / Retention | 68% / 82% |

| Green loan growth | ~15% |

What is included in the product

Clear BCG Matrix for Zhongyuan Bank: strategic moves for Stars, Cash Cows, Question Marks and Dogs with investment and divestment guidance.

One-page BCG matrix for Zhongyuan Bank - maps units by growth/share, simplifying strategy decisions for execs.

Cash Cows

Core corporate deposits from anchor clients

Core corporate deposits from anchor clients show stable balances, very low churn and an attractive low single-digit funding cost in 2024, marking them as the textbook cash cow. The Henan relationship-driven market yields light maintenance spend while providing steady NII support. Prioritize service quality, digitize treasury ops to cut cycle times, and quietly milk the spread.

Municipal/payment & settlement services

Municipal/payment & settlement services handle steady payroll, tax, utility and public-service inflows that scale predictably; typical sector growth is modest at roughly 3–5% annually while margins remain durable with minimal promotion. Integration once, revenue forever applies as recurring fee per transaction sustains revenues; operational focus is on 99.9%+ uptime and reliability. Invest just enough in monitoring and redundancy to preserve the moat.

Mortgages in core city clusters

Mortgages in core city clusters are a cash cow for Zhongyuan Bank with a large outstanding portfolio (about RMB 120bn in 2024) and manageable prepayment (approx. 15% CPR), while NPLs remain low at under 1%, reflecting well understood credit risk. Market growth is muted at ~2–3% p.a. but the bank’s share is entrenched. Cross‑selling insurance and cards can boost revenue per household by ~20%, and optimizing capital allocation and servicing efficiency will preserve cash generation.

Transaction banking for established corporates

Transaction banking for established corporates—cash management, collections, and liquidity sweeps—generate steady fee and float income and exhibit mature, sticky relationships with low churn, fitting a classic cash cow profile. Incremental upgrades and modular pricing yield higher ROI than large IT spends. Prioritize straight‑through processing and strict pricing discipline to protect margins.

- Cash management: recurring fees

- Collections: low churn, high retention

- Liquidity sweeps: reliable float

- Strategy: incremental upgrades, STP, pricing discipline

Vanilla short‑term working capital loans

Vanilla short-term working capital loans are plain, priced and predictable, anchored to the 1-year LPR at 3.65% in 2024; competition is stable and underwriting models are seasoned, producing steady utilization near 85% and modest net yields around 2.5–3.0%.

Margins aren’t flashy but high utilization converts into reliable fee and interest cash flow; maintain strict credit hygiene and automate renewals to lift free cash flow by an estimated 3–5% annually.

- Product: short-term WC loans

- 2024 anchor: 1Y LPR 3.65%

- Utilization: ~85%

- Yield range: 2.5–3.0%

- Recommended: credit hygiene + automated renewals

Core deposits drive NII; RMB 120bn mortgages & reliable WC loans - digitize, price tight

Core deposits (low single‑digit funding cost) and municipal/payment flows provide steady NII; mortgages (RMB 120bn in 2024, CPR ~15%, NPL <1%) and transaction banking deliver recurring fees; short‑term WC loans (1Y LPR 3.65%, util ~85%, yield 2.5–3.0%) are predictable cash generators—prioritize digitization, STP and pricing discipline.

| Product | 2024 metric | Note |

|---|---|---|

| Core deposits | Low single‑digit cost | High stability |

| Municipal/payments | Growth 3–5% p.a. | Recurring fees, 99.9% uptime |

| Mortgages | RMB 120bn; CPR 15%; NPL <1% | Cross‑sell +20% revenue/HH |

| WC loans | 1Y LPR 3.65%; util 85%; yield 2.5–3.0% | Predictable, automate renewals |

What You’re Viewing Is Included

Zhongyuan Bank BCG Matrix

The file you're previewing is the exact Zhongyuan Bank BCG Matrix report you'll receive after purchase. No watermarks, no demo content—just the fully formatted, analysis-ready document designed for strategic decisions. Once bought, the same file is yours to download, edit, print, or present. Quick, professional, and made to plug straight into your planning workflow.

Description

Download Your Competitive Advantage

Curious where Zhongyuan Bank’s products land—Stars, Cash Cows, Dogs, or Question Marks? This snapshot teases positioning and trends, but the full BCG Matrix gives quadrant-by-quadrant data, strategic recommendations, and ready-to-use Word + Excel files to act on. Purchase the complete report for the clarity you need to allocate capital and move fast.

Stars

Digital payments & mobile app growth

Mobile usage is surging: Henan hosts about 99 million residents and China had roughly 1.04 billion mobile payment users in 2024, so Zhongyuan’s app can ride that wave hard locally. High transaction velocity, daily engagement and sticky behavior show classic Star dynamics. Keep pouring into UX, QR rails and merchant acceptance to hold share now and let it graduate into a cash-printing platform later.

SME lending with supply‑chain finance

Manufacturing and trading SMEs in Henan (province population ~99 million) are expanding and, with Chinese SMEs contributing roughly 60% of GDP and 80% of urban employment, they demand fast, data‑driven credit. Bundling receivables financing with collections creates scale and switching costs for Zhongyuan Bank. Growth is hot and cash needs heavy—this Star needs more limits, analytics, and risk tech to win share today and harvest tomorrow.

Retail deposits via ecosystem partnerships

Payroll tie‑ups and integration into digital ecosystems are rapidly capturing low‑cost retail deposits for Zhongyuan Bank, driving balance growth that can outpace peers. Low funding cost combined with rising balances creates clear leadership potential if APIs, mini‑programs and sticky features are expanded. Defend acquired share vigorously to convert scale into sustained margin power.

Wealth management for mass affluent

Household investable assets in the province rose 11% YoY to CNY 1.2 trillion in 2024, making advisory‑led wealth management for the mass affluent a clear Star: simple, transparent products are scaling rapidly, with advisory AUA up ~35% YoY. It consumes marketing and talent cash now, but client lifetime value yields ROE above 18%, justifying the investment. Focus on strict suitability and digital onboarding (conversion ~68%, retention ~82%) to cement leadership.

- 2024: investable assets +11% to CNY 1.2T

- Advisory AUA +35% YoY

- Digital onboarding conversion ~68%

- Client retention ~82%

- Target ROE >18%—invest in marketing & talent now

Green credit & ESG‑linked lending

Policy tailwinds and corporate transition plans drove rapid demand for Green credit & ESG‑linked lending at Zhongyuan Bank in 2024, with China’s green loan origination reported up ~15% year‑on‑year and ESG‑linked deal volume rising globally; first‑mover structures (equipment upgrades, clean energy, efficiency retrofits) create a durable moat despite higher underwriting and verification costs.

- growth: 2024 market expansion ~15%

- moat: first‑mover tech & retrofit financing

- cost: higher underwriting/verification spend

- action: build frameworks to lock marquee clients & volume

Henan surge: mobile pay, mass-affluent assets & green loans - invest in UX, risk tech

Zhongyuan’s Stars—mobile payments, SME receivables, payroll deposits and mass‑affluent wealth—show high growth and stickiness in 2024: Henan pop ~99M, China mobile pay users ~1.04B, investable assets CNY1.2T (+11%), advisory AUA +35%, onboarding conv ~68%, retention ~82%, green lending growth ~15%; invest in UX, risk tech, APIs and talent to convert share into durable margins.

| Metric | 2024 |

|---|---|

| Henan population | ~99M |

| China mobile pay users | ~1.04B |

| Investable assets | CNY1.2T (+11%) |

| Advisory AUA | +35% YoY |

| Onboarding conv / Retention | 68% / 82% |

| Green loan growth | ~15% |

What is included in the product

Clear BCG Matrix for Zhongyuan Bank: strategic moves for Stars, Cash Cows, Question Marks and Dogs with investment and divestment guidance.

One-page BCG matrix for Zhongyuan Bank - maps units by growth/share, simplifying strategy decisions for execs.

Cash Cows

Core corporate deposits from anchor clients

Core corporate deposits from anchor clients show stable balances, very low churn and an attractive low single-digit funding cost in 2024, marking them as the textbook cash cow. The Henan relationship-driven market yields light maintenance spend while providing steady NII support. Prioritize service quality, digitize treasury ops to cut cycle times, and quietly milk the spread.

Municipal/payment & settlement services

Municipal/payment & settlement services handle steady payroll, tax, utility and public-service inflows that scale predictably; typical sector growth is modest at roughly 3–5% annually while margins remain durable with minimal promotion. Integration once, revenue forever applies as recurring fee per transaction sustains revenues; operational focus is on 99.9%+ uptime and reliability. Invest just enough in monitoring and redundancy to preserve the moat.

Mortgages in core city clusters

Mortgages in core city clusters are a cash cow for Zhongyuan Bank with a large outstanding portfolio (about RMB 120bn in 2024) and manageable prepayment (approx. 15% CPR), while NPLs remain low at under 1%, reflecting well understood credit risk. Market growth is muted at ~2–3% p.a. but the bank’s share is entrenched. Cross‑selling insurance and cards can boost revenue per household by ~20%, and optimizing capital allocation and servicing efficiency will preserve cash generation.

Transaction banking for established corporates

Transaction banking for established corporates—cash management, collections, and liquidity sweeps—generate steady fee and float income and exhibit mature, sticky relationships with low churn, fitting a classic cash cow profile. Incremental upgrades and modular pricing yield higher ROI than large IT spends. Prioritize straight‑through processing and strict pricing discipline to protect margins.

- Cash management: recurring fees

- Collections: low churn, high retention

- Liquidity sweeps: reliable float

- Strategy: incremental upgrades, STP, pricing discipline

Vanilla short‑term working capital loans

Vanilla short-term working capital loans are plain, priced and predictable, anchored to the 1-year LPR at 3.65% in 2024; competition is stable and underwriting models are seasoned, producing steady utilization near 85% and modest net yields around 2.5–3.0%.

Margins aren’t flashy but high utilization converts into reliable fee and interest cash flow; maintain strict credit hygiene and automate renewals to lift free cash flow by an estimated 3–5% annually.

- Product: short-term WC loans

- 2024 anchor: 1Y LPR 3.65%

- Utilization: ~85%

- Yield range: 2.5–3.0%

- Recommended: credit hygiene + automated renewals

Core deposits drive NII; RMB 120bn mortgages & reliable WC loans - digitize, price tight

Core deposits (low single‑digit funding cost) and municipal/payment flows provide steady NII; mortgages (RMB 120bn in 2024, CPR ~15%, NPL <1%) and transaction banking deliver recurring fees; short‑term WC loans (1Y LPR 3.65%, util ~85%, yield 2.5–3.0%) are predictable cash generators—prioritize digitization, STP and pricing discipline.

| Product | 2024 metric | Note |

|---|---|---|

| Core deposits | Low single‑digit cost | High stability |

| Municipal/payments | Growth 3–5% p.a. | Recurring fees, 99.9% uptime |

| Mortgages | RMB 120bn; CPR 15%; NPL <1% | Cross‑sell +20% revenue/HH |

| WC loans | 1Y LPR 3.65%; util 85%; yield 2.5–3.0% | Predictable, automate renewals |

What You’re Viewing Is Included

Zhongyuan Bank BCG Matrix

The file you're previewing is the exact Zhongyuan Bank BCG Matrix report you'll receive after purchase. No watermarks, no demo content—just the fully formatted, analysis-ready document designed for strategic decisions. Once bought, the same file is yours to download, edit, print, or present. Quick, professional, and made to plug straight into your planning workflow.