Zydus Lifesciences Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

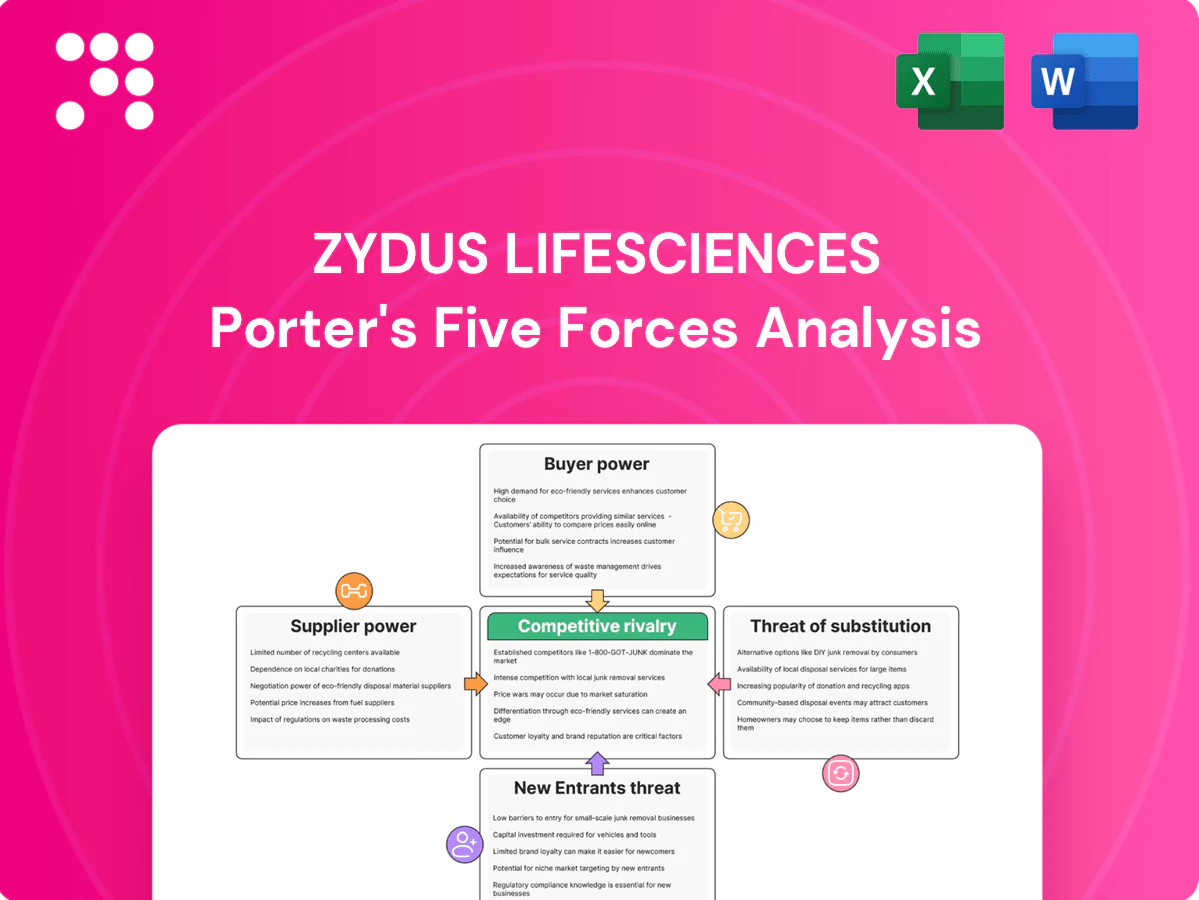

Zydus Lifesciences faces moderate supplier power, high buyer price sensitivity, and intense competition from generics and established branded players; regulatory barriers limit new entrants but biotech innovation raises substitute risk. This snapshot highlights strategic pressures and market levers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Zydus Lifesciences’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Backward-integrated APIs

Zydus's backward-integrated API network, anchored at sites such as Moraiya and Baddi, supplied over half of its small-molecule API needs in 2024, sharply cutting external procurement and improving cost control. This integration reduced exposure to global price volatility and supply disruptions during 2024 supply-chain shocks. In-house API manufacture also tightened quality assurance and regulatory compliance across the value chain. Collectively, these factors dampen supplier bargaining power for small-molecule generics.

Specialized biologics inputs

As of 2024 biosimilars and vaccines rely on cell lines, media, resins and single-use systems sourced from a handful of global vendors (Sartorius, Thermo Fisher, Cytiva, Merck), concentrating supply. Limited qualified suppliers and stringent specs raise switching costs, while validation and qualification often take 6–12 months. Long lead times of several months further enhance supplier leverage, concentrating power with niche biologics input providers.

Regulatory-compliant materials

US/EU GMP requirements, reliance on DMF-backed inputs, and serialization/track-and-trace regimes (EU FMD in force since 2019 and US DSCSA milestones culminating Nov 27, 2023) narrow Zydus’s qualified supplier pool. Failures in compliant materials trigger batch revalidation and regulatory filings, raising regulatory risk and dependence on approved vendors. Dual-sourcing mitigates but does not eliminate supplier leverage for critical inputs.

Logistics and cold-chain needs

Vaccines and biologics require reliable cold-chain and specialized packaging, and as of 2024 only a limited set of logistics providers consistently meet GDP standards across key markets, giving those providers incremental bargaining power. Zydus’ manufacturing and procurement scale improves negotiating leverage on pricing and capacity, but regional gaps in certified cold-chain coverage sustain supplier leverage in certain geographies.

- Cold-chain + GDP scarcity → higher supplier leverage

- Zydus scale mitigates price/capacity risk

- Geographic variability keeps localized supplier power

China/India API concentration

Global API supply remains concentrated in India and China, accounting for roughly 80% of production in 2024, exposing Zydus to geopolitical, regulatory and compliance shocks.

Backward-integrated API supply >50%; biologics reliant on ~4 vendors, 6–12 month lead times

Zydus’s backward-integrated API network supplied >50% of small-molecule API needs in 2024, reducing external procurement and supplier leverage. Critical biologics inputs (resins, single-use systems) are concentrated among ~4 global vendors with 6–12 month qualification lead times, increasing switching costs. c.80% of global APIs sourced from India/China in 2024 raises geopolitical and compliance exposure, while scale and dual-sourcing partially mitigate risks.

| Metric | 2024 Value |

|---|---|

| In-house API supply | >50% |

| APIs from India/China | ~80% |

| Key biologics vendors | ~4 |

| Qualification lead time | 6–12 months |

What is included in the product

Tailored exclusively for Zydus Lifesciences, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, and market entry risks affecting pricing and profitability. It identifies disruptive threats, substitutes, and protective dynamics that shape Zydus’s strategic position and growth prospects.

A concise one-sheet Porter's Five Forces for Zydus Lifesciences—visual spider chart with editable pressure levels, clean layout for pitch decks, no macros and easy integration into reports and dashboards to instantly relieve strategic analysis pain points.

Customers Bargaining Power

Tender-driven government buys

Institutional tenders in India and emerging markets aggregate demand and drive brutal price competition, with winner-take-most awards often allocating over 70% of volumes to the lowest bidder and sharply compressing margins for suppliers. Buyers can switch among therapeutically equivalent generics with minimal cost, increasing price sensitivity and forcing Zydus to trade lower prices for volume. Zydus must balance aggressive pricing with assured on-time supply and manufacturing quality to retain contract wins and protect market access.

US wholesalers and PBMs

Consolidated US channels—three PBMs (CVS Caremark, Express Scripts, OptumRx) covering roughly 80% of prescriptions and three wholesalers (McKesson, AmerisourceBergen, Cardinal) handling about 85–90% of distribution—exert heavy pricing pressure on Zydus’s US volumes. Steep generic price erosion and routine chargebacks amplify buyer leverage, compressing margins. Formulary access hinges on rebate levels and contracting strength with PBMs/GPOs. Zydus’s scale and differentiated ANDA filings partially mitigate this pressure.

Brand equity in wellness

Consumer wellness and branded formulations show notable loyalty and OTC stickiness, moderating buyer power through perceived differentiation and switching costs. Zydus leverages broad marketing and pan-India distribution to reinforce retention (2024). However, rising private-label penetration in value channels in 2024 reintroduces price pressure, capping bargaining power despite brand equity.

Biosimilars physician inertia

Physician trust and restrictive interchangeability rules slow switching to Zydus biosimilars, limiting buyer leverage despite labels supporting substitution; education, pharmacovigilance and accumulating real-world data have enabled uptake at typical biosimilar discounts of 20–40% versus originators in 2024. Hospital P&T committees continue aggressive tendering, producing a net balanced-to-moderate buyer power.

- Physician inertia reduces immediate switching

- RWD and pharmaco-vigilance support market entry

- Hospital tenders sustain price pressure

Animal health channels

Vet clinics, distributors and farms in animal health remain highly fragmented versus human pharma, reducing buyer leverage; India's animal health market was about USD 1.2 billion in 2024 with poultry roughly 50% of the mix. Large integrators and procurement alliances, which control an estimated 30–40% of poultry demand, can demand volume discounts. Product availability and on-field technical support remain decisive purchase drivers.

- Fragmentation softens bargaining power

- Large integrators can force discounts (30–40% poultry share)

- Product availability and field support are key

PBM and tender dominance squeeze generics margins; biosimilars, animal health offer limited relief

Institutional tenders (>70% winner-take-most) and three PBMs (~80% US scripts) give buyers strong pricing power, compressing margins despite Zydus scale and ANDA differentiation. Biosimilars trade at 20–40% discounts, moderating buyer leverage. Animal health fragmentation (market USD 1.2B; poultry ~50%) reduces customer bargaining.

| Metric | 2024 |

|---|---|

| PBM script share | ~80% |

| Winner-take-most tenders | >70% volumes |

| Animal health market | USD 1.2B |

Full Version Awaits

Zydus Lifesciences Porter's Five Forces Analysis

This preview shows the exact Zydus Lifesciences Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The report is fully formatted, ready to download and use upon payment. It comprehensively covers competitive rivalry, supplier and buyer power, and threats of new entrants and substitutes.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Zydus Lifesciences faces moderate supplier power, high buyer price sensitivity, and intense competition from generics and established branded players; regulatory barriers limit new entrants but biotech innovation raises substitute risk. This snapshot highlights strategic pressures and market levers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Zydus Lifesciences’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Backward-integrated APIs

Zydus's backward-integrated API network, anchored at sites such as Moraiya and Baddi, supplied over half of its small-molecule API needs in 2024, sharply cutting external procurement and improving cost control. This integration reduced exposure to global price volatility and supply disruptions during 2024 supply-chain shocks. In-house API manufacture also tightened quality assurance and regulatory compliance across the value chain. Collectively, these factors dampen supplier bargaining power for small-molecule generics.

Specialized biologics inputs

As of 2024 biosimilars and vaccines rely on cell lines, media, resins and single-use systems sourced from a handful of global vendors (Sartorius, Thermo Fisher, Cytiva, Merck), concentrating supply. Limited qualified suppliers and stringent specs raise switching costs, while validation and qualification often take 6–12 months. Long lead times of several months further enhance supplier leverage, concentrating power with niche biologics input providers.

Regulatory-compliant materials

US/EU GMP requirements, reliance on DMF-backed inputs, and serialization/track-and-trace regimes (EU FMD in force since 2019 and US DSCSA milestones culminating Nov 27, 2023) narrow Zydus’s qualified supplier pool. Failures in compliant materials trigger batch revalidation and regulatory filings, raising regulatory risk and dependence on approved vendors. Dual-sourcing mitigates but does not eliminate supplier leverage for critical inputs.

Logistics and cold-chain needs

Vaccines and biologics require reliable cold-chain and specialized packaging, and as of 2024 only a limited set of logistics providers consistently meet GDP standards across key markets, giving those providers incremental bargaining power. Zydus’ manufacturing and procurement scale improves negotiating leverage on pricing and capacity, but regional gaps in certified cold-chain coverage sustain supplier leverage in certain geographies.

- Cold-chain + GDP scarcity → higher supplier leverage

- Zydus scale mitigates price/capacity risk

- Geographic variability keeps localized supplier power

China/India API concentration

Global API supply remains concentrated in India and China, accounting for roughly 80% of production in 2024, exposing Zydus to geopolitical, regulatory and compliance shocks.

Backward-integrated API supply >50%; biologics reliant on ~4 vendors, 6–12 month lead times

Zydus’s backward-integrated API network supplied >50% of small-molecule API needs in 2024, reducing external procurement and supplier leverage. Critical biologics inputs (resins, single-use systems) are concentrated among ~4 global vendors with 6–12 month qualification lead times, increasing switching costs. c.80% of global APIs sourced from India/China in 2024 raises geopolitical and compliance exposure, while scale and dual-sourcing partially mitigate risks.

| Metric | 2024 Value |

|---|---|

| In-house API supply | >50% |

| APIs from India/China | ~80% |

| Key biologics vendors | ~4 |

| Qualification lead time | 6–12 months |

What is included in the product

Tailored exclusively for Zydus Lifesciences, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, and market entry risks affecting pricing and profitability. It identifies disruptive threats, substitutes, and protective dynamics that shape Zydus’s strategic position and growth prospects.

A concise one-sheet Porter's Five Forces for Zydus Lifesciences—visual spider chart with editable pressure levels, clean layout for pitch decks, no macros and easy integration into reports and dashboards to instantly relieve strategic analysis pain points.

Customers Bargaining Power

Tender-driven government buys

Institutional tenders in India and emerging markets aggregate demand and drive brutal price competition, with winner-take-most awards often allocating over 70% of volumes to the lowest bidder and sharply compressing margins for suppliers. Buyers can switch among therapeutically equivalent generics with minimal cost, increasing price sensitivity and forcing Zydus to trade lower prices for volume. Zydus must balance aggressive pricing with assured on-time supply and manufacturing quality to retain contract wins and protect market access.

US wholesalers and PBMs

Consolidated US channels—three PBMs (CVS Caremark, Express Scripts, OptumRx) covering roughly 80% of prescriptions and three wholesalers (McKesson, AmerisourceBergen, Cardinal) handling about 85–90% of distribution—exert heavy pricing pressure on Zydus’s US volumes. Steep generic price erosion and routine chargebacks amplify buyer leverage, compressing margins. Formulary access hinges on rebate levels and contracting strength with PBMs/GPOs. Zydus’s scale and differentiated ANDA filings partially mitigate this pressure.

Brand equity in wellness

Consumer wellness and branded formulations show notable loyalty and OTC stickiness, moderating buyer power through perceived differentiation and switching costs. Zydus leverages broad marketing and pan-India distribution to reinforce retention (2024). However, rising private-label penetration in value channels in 2024 reintroduces price pressure, capping bargaining power despite brand equity.

Biosimilars physician inertia

Physician trust and restrictive interchangeability rules slow switching to Zydus biosimilars, limiting buyer leverage despite labels supporting substitution; education, pharmacovigilance and accumulating real-world data have enabled uptake at typical biosimilar discounts of 20–40% versus originators in 2024. Hospital P&T committees continue aggressive tendering, producing a net balanced-to-moderate buyer power.

- Physician inertia reduces immediate switching

- RWD and pharmaco-vigilance support market entry

- Hospital tenders sustain price pressure

Animal health channels

Vet clinics, distributors and farms in animal health remain highly fragmented versus human pharma, reducing buyer leverage; India's animal health market was about USD 1.2 billion in 2024 with poultry roughly 50% of the mix. Large integrators and procurement alliances, which control an estimated 30–40% of poultry demand, can demand volume discounts. Product availability and on-field technical support remain decisive purchase drivers.

- Fragmentation softens bargaining power

- Large integrators can force discounts (30–40% poultry share)

- Product availability and field support are key

PBM and tender dominance squeeze generics margins; biosimilars, animal health offer limited relief

Institutional tenders (>70% winner-take-most) and three PBMs (~80% US scripts) give buyers strong pricing power, compressing margins despite Zydus scale and ANDA differentiation. Biosimilars trade at 20–40% discounts, moderating buyer leverage. Animal health fragmentation (market USD 1.2B; poultry ~50%) reduces customer bargaining.

| Metric | 2024 |

|---|---|

| PBM script share | ~80% |

| Winner-take-most tenders | >70% volumes |

| Animal health market | USD 1.2B |

Full Version Awaits

Zydus Lifesciences Porter's Five Forces Analysis

This preview shows the exact Zydus Lifesciences Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The report is fully formatted, ready to download and use upon payment. It comprehensively covers competitive rivalry, supplier and buyer power, and threats of new entrants and substitutes.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Zydus Lifesciences faces moderate supplier power, high buyer price sensitivity, and intense competition from generics and established branded players; regulatory barriers limit new entrants but biotech innovation raises substitute risk. This snapshot highlights strategic pressures and market levers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Zydus Lifesciences’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Backward-integrated APIs

Zydus's backward-integrated API network, anchored at sites such as Moraiya and Baddi, supplied over half of its small-molecule API needs in 2024, sharply cutting external procurement and improving cost control. This integration reduced exposure to global price volatility and supply disruptions during 2024 supply-chain shocks. In-house API manufacture also tightened quality assurance and regulatory compliance across the value chain. Collectively, these factors dampen supplier bargaining power for small-molecule generics.

Specialized biologics inputs

As of 2024 biosimilars and vaccines rely on cell lines, media, resins and single-use systems sourced from a handful of global vendors (Sartorius, Thermo Fisher, Cytiva, Merck), concentrating supply. Limited qualified suppliers and stringent specs raise switching costs, while validation and qualification often take 6–12 months. Long lead times of several months further enhance supplier leverage, concentrating power with niche biologics input providers.

Regulatory-compliant materials

US/EU GMP requirements, reliance on DMF-backed inputs, and serialization/track-and-trace regimes (EU FMD in force since 2019 and US DSCSA milestones culminating Nov 27, 2023) narrow Zydus’s qualified supplier pool. Failures in compliant materials trigger batch revalidation and regulatory filings, raising regulatory risk and dependence on approved vendors. Dual-sourcing mitigates but does not eliminate supplier leverage for critical inputs.

Logistics and cold-chain needs

Vaccines and biologics require reliable cold-chain and specialized packaging, and as of 2024 only a limited set of logistics providers consistently meet GDP standards across key markets, giving those providers incremental bargaining power. Zydus’ manufacturing and procurement scale improves negotiating leverage on pricing and capacity, but regional gaps in certified cold-chain coverage sustain supplier leverage in certain geographies.

- Cold-chain + GDP scarcity → higher supplier leverage

- Zydus scale mitigates price/capacity risk

- Geographic variability keeps localized supplier power

China/India API concentration

Global API supply remains concentrated in India and China, accounting for roughly 80% of production in 2024, exposing Zydus to geopolitical, regulatory and compliance shocks.

Backward-integrated API supply >50%; biologics reliant on ~4 vendors, 6–12 month lead times

Zydus’s backward-integrated API network supplied >50% of small-molecule API needs in 2024, reducing external procurement and supplier leverage. Critical biologics inputs (resins, single-use systems) are concentrated among ~4 global vendors with 6–12 month qualification lead times, increasing switching costs. c.80% of global APIs sourced from India/China in 2024 raises geopolitical and compliance exposure, while scale and dual-sourcing partially mitigate risks.

| Metric | 2024 Value |

|---|---|

| In-house API supply | >50% |

| APIs from India/China | ~80% |

| Key biologics vendors | ~4 |

| Qualification lead time | 6–12 months |

What is included in the product

Tailored exclusively for Zydus Lifesciences, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, and market entry risks affecting pricing and profitability. It identifies disruptive threats, substitutes, and protective dynamics that shape Zydus’s strategic position and growth prospects.

A concise one-sheet Porter's Five Forces for Zydus Lifesciences—visual spider chart with editable pressure levels, clean layout for pitch decks, no macros and easy integration into reports and dashboards to instantly relieve strategic analysis pain points.

Customers Bargaining Power

Tender-driven government buys

Institutional tenders in India and emerging markets aggregate demand and drive brutal price competition, with winner-take-most awards often allocating over 70% of volumes to the lowest bidder and sharply compressing margins for suppliers. Buyers can switch among therapeutically equivalent generics with minimal cost, increasing price sensitivity and forcing Zydus to trade lower prices for volume. Zydus must balance aggressive pricing with assured on-time supply and manufacturing quality to retain contract wins and protect market access.

US wholesalers and PBMs

Consolidated US channels—three PBMs (CVS Caremark, Express Scripts, OptumRx) covering roughly 80% of prescriptions and three wholesalers (McKesson, AmerisourceBergen, Cardinal) handling about 85–90% of distribution—exert heavy pricing pressure on Zydus’s US volumes. Steep generic price erosion and routine chargebacks amplify buyer leverage, compressing margins. Formulary access hinges on rebate levels and contracting strength with PBMs/GPOs. Zydus’s scale and differentiated ANDA filings partially mitigate this pressure.

Brand equity in wellness

Consumer wellness and branded formulations show notable loyalty and OTC stickiness, moderating buyer power through perceived differentiation and switching costs. Zydus leverages broad marketing and pan-India distribution to reinforce retention (2024). However, rising private-label penetration in value channels in 2024 reintroduces price pressure, capping bargaining power despite brand equity.

Biosimilars physician inertia

Physician trust and restrictive interchangeability rules slow switching to Zydus biosimilars, limiting buyer leverage despite labels supporting substitution; education, pharmacovigilance and accumulating real-world data have enabled uptake at typical biosimilar discounts of 20–40% versus originators in 2024. Hospital P&T committees continue aggressive tendering, producing a net balanced-to-moderate buyer power.

- Physician inertia reduces immediate switching

- RWD and pharmaco-vigilance support market entry

- Hospital tenders sustain price pressure

Animal health channels

Vet clinics, distributors and farms in animal health remain highly fragmented versus human pharma, reducing buyer leverage; India's animal health market was about USD 1.2 billion in 2024 with poultry roughly 50% of the mix. Large integrators and procurement alliances, which control an estimated 30–40% of poultry demand, can demand volume discounts. Product availability and on-field technical support remain decisive purchase drivers.

- Fragmentation softens bargaining power

- Large integrators can force discounts (30–40% poultry share)

- Product availability and field support are key

PBM and tender dominance squeeze generics margins; biosimilars, animal health offer limited relief

Institutional tenders (>70% winner-take-most) and three PBMs (~80% US scripts) give buyers strong pricing power, compressing margins despite Zydus scale and ANDA differentiation. Biosimilars trade at 20–40% discounts, moderating buyer leverage. Animal health fragmentation (market USD 1.2B; poultry ~50%) reduces customer bargaining.

| Metric | 2024 |

|---|---|

| PBM script share | ~80% |

| Winner-take-most tenders | >70% volumes |

| Animal health market | USD 1.2B |

Full Version Awaits

Zydus Lifesciences Porter's Five Forces Analysis

This preview shows the exact Zydus Lifesciences Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The report is fully formatted, ready to download and use upon payment. It comprehensively covers competitive rivalry, supplier and buyer power, and threats of new entrants and substitutes.